If you run a business in a UAE free zone, you have probably heard that free zone companies pay 0% corporate tax. That statement is not wrong, but it is dangerously incomplete. The 0% rate is not automatic. It is not guaranteed by your free zone license. And getting it wrong does not just mean paying 9% for one year it means losing your eligibility for the next five years, a penalty that can run into millions of dirhams.

Since the UAE introduced corporate tax under Federal Decree-Law No. 47 of 2022 on 1 June 2023, every free zone entity is a taxable person under the law. You must register with the Federal Tax Authority (FTA), file an annual corporate tax return, prepare audited financial statements, and comply with transfer pricing rules. The only benefit of being a Qualifying Free Zone Person (QFZP) is that your qualifying income is taxed at 0% instead of 9%. Everything else registration, filing, record keeping, VAT compliance, audit obligations applies regardless of your tax rate.

The 2026 tax changes have made QFZP compliance more complex. Ministerial Decision No. 229 of 2025 expanded qualifying commodity trading but tightened substance requirements. Federal Decree-Law No. 17 of 2025 extended the FTA’s audit reach to 15 years in evasion cases. The FTA completed 93,000 inspection visits in 2024 a 135% year-on-year increase and is now cross-referencing corporate tax returns against VAT filings to identify revenue discrepancies. Free zone businesses that file as QFZPs without genuinely meeting every condition are operating on borrowed time.

This guide explains exactly what it takes to qualify for and maintain the 0% rate in 2026. Whether your business is in DMCC, IFZA, JAFZA, SAIF Zone, RAK ICC, Meydan, DIFC, or any of the UAE’s 40+ free zones, the rules are the same. We walk you through each qualifying condition, the complete list of qualifying and excluded activities, the de minimis calculation with worked examples, substance requirements, the IP nexus formula, the five-year disqualification trap, and a head-to-head comparison of when the 0% rate is actually less advantageous than the standard 9% mainland regime.

If you already hold a free zone license and want to know where you stand, or you are evaluating a new free zone setup and want to model the real tax outcome, this is the reference you need before your next corporate tax filing.

✅ Book Your Free QFZP Assessment

1. What Is a Qualifying Free Zone Person?

A Qualifying Free Zone Person is defined under Article 18 of the Corporate Tax Law. It is a juridical person a company, branch, or other legal entity that is incorporated, established, or registered in a UAE free zone and meets a specific set of conditions. If all conditions are met, the entity’s qualifying income is subject to a 0% corporate tax rate. Any non-qualifying income is taxed at the standard 9% rate. The detailed rules are set out in Cabinet Decision No. 100 of 2023 and Ministerial Decision No. 229 of 2025 (which replaced the earlier MD 265 of 2023).

The term “free zone person” refers to the juridical person as a whole. This means a free zone company that also has a mainland branch (a Domestic Permanent Establishment) is treated as one entity. The 0% rate applies only to the free zone business the portion registered in the free zone. The mainland branch’s income is taxed at 9% regardless. Similarly, a foreign company with a branch registered in a UAE free zone can claim QFZP status only on the income of that free zone branch.

It is critical to understand that QFZP status is not something you apply for or receive approval for. There is no FTA certificate confirming you are a QFZP. You self-assess when you file your corporate tax return. If the FTA later determines during an audit that you did not meet the conditions, you lose QFZP status retroactively from the beginning of that tax period, and the consequences are severe: 9% on all income for that year plus a five-year lockout.

The FTA’s official guidance on this regime is the Free Zone Persons Corporate Tax Guide (CTGFZP1), published in May 2024. It runs to over 100 pages and contains detailed examples for each qualifying condition. If you are managing your QFZP status in-house, this guide is essential reading. If you are working with a tax consultant, ensure they have reviewed it thoroughly.

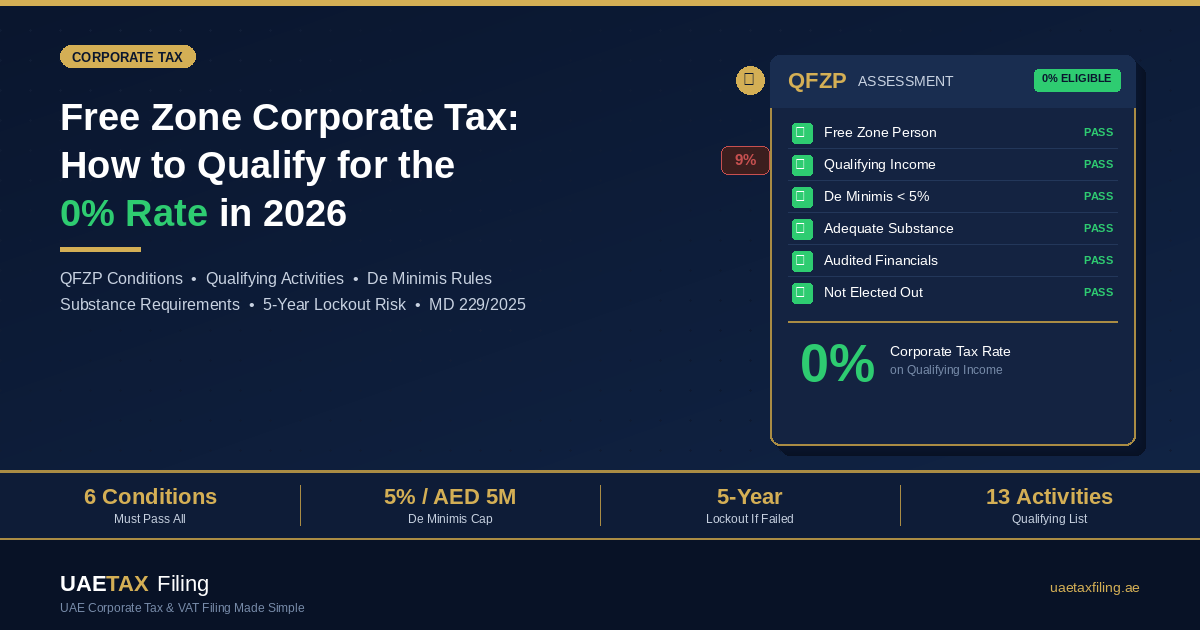

2. The Six Conditions You Must Meet (Every Single Year)

To qualify as a QFZP, your free zone entity must satisfy all six of the following conditions simultaneously, for every single tax period. Failing any one of them at any point during the tax period is enough to disqualify you. There is no partial compliance and no grace period.

Condition 1: Be a Free Zone Person

You must be a juridical person incorporated, established, or otherwise registered in a UAE free zone. This includes branches of foreign companies and branches of UAE mainland companies that are separately registered in a free zone. Natural persons (individuals) cannot be QFZPs, even if they hold a free zone license. Freelancers operating as natural persons fall under different corporate tax rules and should refer to the relevant thresholds for natural persons conducting business.

Condition 2: Derive Qualifying Income

Your income must fall into categories defined as “qualifying income” under Cabinet Decision No. 100 of 2023 and Ministerial Decision No. 229 of 2025. This is the most complex condition and the one where most businesses get caught. We break it down fully in Section 3 and the complete activity lists in Section 4.

Condition 3: Meet the De Minimis Threshold

Your non-qualifying revenue must not exceed 5% of your total revenue or AED 5 million, whichever is lower. If you earn even one dirham of non-qualifying income beyond this threshold, you lose QFZP status entirely not just on the excess amount, but on your entire income for the period. We cover this rule with worked examples in Section 5.

Condition 4: Maintain Adequate Substance in the Free Zone

You must conduct your core income-generating activities (CIGAs) within the free zone. This means maintaining adequate assets, qualified full-time employees, and operating expenditure in the free zone. Cabinet Decision No. 100 of 2023 clarified that CIGAs must be significant functions that drive business value, not merely support activities. You can outsource CIGAs, but only to related parties or third parties within a UAE free zone, and you must maintain adequate supervision. This is increasingly important as the FTA ramps up substance audits. See Section 6 for what “adequate” means in practice.

Condition 5: Prepare Audited Financial Statements

Every QFZP must prepare audited financial statements following Ministerial Decision No. 84 of 2025, regardless of revenue. This is a significant compliance cost that many small free zone businesses overlook. Mainland companies only require audited statements if revenue exceeds AED 50 million, but for QFZPs, there is no revenue threshold the audit is mandatory at every size. A DMCC company with AED 500,000 in revenue and a JAFZA company with AED 50 million in revenue both need a full audit to claim the 0% rate. The audit must follow International Standards on Auditing (ISA) and the financial statements must comply with IFRS or IFRS for SMEs as applicable.

Condition 6: Do Not Elect Out of the QFZP Regime

You must not have made an irrevocable election to be subject to the standard 9% corporate tax regime. Some businesses choose to opt out deliberately for example, to access group relief, business restructuring relief, or tax loss transfers, none of which are available to QFZPs. If your free zone company is part of a larger group that needs to reorganise or transfer losses, the 0% rate may actually be a structural impediment. This is a strategic decision that should be made with professional corporate tax advice.

3. What Counts as Qualifying Income (and What Does Not)

Qualifying income is determined by a combination of what activity you perform and who you perform it for. The rules come from Cabinet Decision No. 100 of 2023, supplemented by Ministerial Decision No. 229 of 2025. There are three main categories.

Category A: Income from Transactions with Other Free Zone Persons

Revenue earned from transactions with other free zone entities qualifies, provided the activity is a qualifying activity (see Section 4) and the other free zone person is the beneficial recipient. The beneficial recipient test is critical: if you sell to a free zone company that immediately passes the goods or services through to a mainland customer, the FTA may look through the arrangement and treat the mainland entity as the real recipient. The FTA’s Free Zone Guide (CTGFZP1) states that you can rely on a written statement from the buyer confirming they are the beneficial recipient, but only if you have no reason to believe the statement is incorrect.

Practical tip: Insert a contractual clause in every free zone-to-free zone agreement confirming the buyer is the beneficial recipient. This creates an audit trail that demonstrates you performed due diligence. If the FTA challenges the transaction during an audit, this clause is your first line of defence.

Category B: Income from Qualifying Activities with Non-Free Zone Persons

Certain qualifying activities generate qualifying income even when the customer is a mainland UAE company or a foreign entity. However, the list of activities that qualify regardless of customer status is narrower than most businesses expect. Manufacturing, processing, commodity trading, ship and aircraft operations, and distribution from Designated Zones can qualify even with mainland counterparties. Consulting, IT services, and general trading with mainland companies are more restricted they may qualify only if the specific activity is listed and not an excluded activity. Each revenue stream must be individually assessed.

Category C: Ancillary and Passive Income

Dividends, capital gains, interest, royalties from qualifying intellectual property, and other passive income can be qualifying income, but only if your total non-qualifying revenue stays within the de minimis threshold (Section 5). If you are a holding company deriving dividend income from UAE subsidiaries, this income is typically exempt under the participation exemption in Article 23 of the Corporate Tax Law. However, proper structuring is essential to ensure the exemption applies, particularly where the subsidiaries are mainland companies.

What About Revenue from VAT-Related Activities?

Free zone companies that are also registered for VAT because they make taxable supplies within or into the mainland need to reconcile their corporate tax and VAT return positions carefully. Revenue reported in your quarterly VAT returns for the year must be consistent with the revenue you declare in your annual corporate tax return. The FTA is actively cross-referencing these filings. A company that reports AED 10 million in output supplies on its VAT returns but only AED 8 million in revenue on its corporate tax return will be flagged for review.

4. Qualifying Activities vs. Excluded Activities: The Complete Lists

The distinction between qualifying and excluded activities is where most QFZP assessments succeed or fail. Ministerial Decision No. 229 of 2025 (effective retroactively from 1 June 2023) sets out the definitive lists, replacing the earlier MD 265 of 2023. These lists were further clarified by the FTA in the Free Zone Persons Guide (CTGFZP1) and updated by Ministerial Decision No. 230 of 2025 regarding recognised price reporting agencies for commodity trading.

4.1 Qualifying Activities (Article 2(1) of MD 229/2025)

Qualifying Activity | Scope and Key Details

(a) Manufacturing of goods or materials | Production, improvement, or assembly of products from raw materials or components. Includes repair and maintenance of rotable components. Distribution of manufactured goods is a separate activity and must be assessed independently.

(b) Processing of goods or materials | Preparation, treatment, transformation, or conversion of goods. Broader than manufacturing; covers industrial processing, refining, and similar activities.

(c) Trading of qualifying commodities | Physical trading of metals, minerals, industrial chemicals, energy, and agriculture commodities with a quoted price on a Recognised Commodities Exchange Market or from a recognised price reporting agency (per MD 230/2025). Includes associated derivative hedging and structured financing: prepayment, factoring, forfaiting, countertrade, warehouse receipt financing, export receivable financing, Islamic trade finance, and streaming. Goods packaged for retail sale excluded. 51% test: if distribution/warehousing/logistics revenue exceeds 51% of total revenue, this activity does not qualify.

(d) Holding of shares and securities | Must be held for investment purposes for an uninterrupted 12-month period. Short-term trading does not qualify.

(e) Ownership, management, operation of ships | International transport of passengers, goods, or livestock. Towing, dredging, bareboat chartering included. Local (domestic) transport does not qualify.

(f) Reinsurance services | Regulated under Federal Decree-Law No. 48 of 2023 or No. 14 of 2018. Direct insurance is excluded.

(g) Fund and wealth management | Regulated fund management activities under UAE financial services legislation.

(h) Headquarter services to related parties | Administration, oversight, management of group companies. Includes senior management, captive insurance, procurement, business planning, risk management, coordination.

(i) Treasury and financing to related parties or own account | Expanded under MD 229/2025 to include financing for the QFZP’s own account (self-investment). Income on surplus funds is qualifying income.

(j) Ownership, management, operation of aircraft | Similar scope to shipping. Includes leasing of aircraft and rotable components for international operations.

(k) Distribution of goods in/from a Designated Zone | Buying and selling tangible goods imported through the Designated Zone. High-sea sales qualify. Foreign goods for UAE mainland must enter through the Designated Zone.

(l) Logistics services | Storage and transportation on behalf of another person without taking title. Cargo handling, warehousing, freight forwarding, customs brokerage, document preparation.

(m) Qualifying intellectual property | Patents, copyrighted software, and functionally equivalent rights. Marketing IP (trademarks) excluded. Nexus formula applies (see Section 7).

4.2 Excluded Activities (Article 2(2) of MD 229/2025)

The following activities are excluded. Revenue from these counts as non-qualifying income. If it exceeds the de minimis threshold, you lose QFZP status for five years.

Excluded Activity | Exceptions

(a) Transactions with natural persons | Exceptions: shipping (e), fund management (g), HQ services (h), distribution from Designated Zones (k) may involve natural persons.

(b) Banking activities | Exception: treasury/financing to related parties or own account (i) and regulated fund management (g).

(c) Insurance activities | Exception: reinsurance (f) and captive insurance to related parties under HQ services (h).

(d) Finance and leasing activities | Exceptions: treasury to related parties (i), commodity trading financing (c), ship/aircraft leasing (e/j).

(e) Ownership/exploitation of immovable property | Exception: commercial property in a free zone where the transaction is with another free zone person. Residential property excluded in all cases.

(f) Ancillary activities to any excluded activity | If it supports or is closely related to an excluded activity, it is also excluded. A broad catch-all the FTA can apply widely.

4.3 Real-World Scenarios

Scenario 1 DMCC IT consulting firm: Provides software development to other free zone entities (qualifying Category A) and to mainland UAE corporates (qualifying Category B). Also provides IT support to individual consumers via an online platform (excluded transactions with natural persons). If individual consumer revenue exceeds the de minimis threshold, QFZP status is lost.

Scenario 2 JAFZA trading company: Imports electronics from China into JAFZA (a Designated Zone), stores them, and sells to mainland UAE distributors who resell. Qualifies under distribution from a Designated Zone. If the same company starts selling directly to end consumers (natural persons), that revenue is excluded.

Scenario 3 IFZA holding company: Holds shares in three mainland subsidiaries and receives dividends exempt under Article 23 participation exemption. Also provides management services to subsidiaries (qualifying HQ services). However, leasing office furniture to an unrelated mainland company would be non-qualifying.

Scenario 4 RAK ICC trademark licensor: Licensing a brand name (trademark) to mainland retailers. Marketing-related IP is explicitly excluded from qualifying IP. If trademark licensing is the only income, the company cannot be a QFZP because 100% of revenue is non-qualifying.

5. The De Minimis Rule: Where Most Businesses Lose QFZP Status

Under Article 3 of Ministerial Decision No. 229 of 2025, your non-qualifying revenue must not exceed the lower of 5% of your total revenue or AED 5 million. This is the single most important threshold for any QFZP.

How to calculate: Identify all revenue from excluded activities and from non-qualifying transactions with non-free zone persons. Divide by total revenue. Compare to both the 5% limit and the AED 5 million cap. If either is exceeded, you fail.

Important: Revenue earned through a mainland Domestic Permanent Establishment (branch) of your free zone company is not included in the de minimis calculation, because that revenue is already taxed at 9%. The de minimis test applies only to income of the free zone business itself.

Worked Example 1 Passes

Company A (DMCC) has total free zone revenue of AED 10 million. AED 9.6 million from consulting to free zone companies (qualifying). AED 400,000 from a service to a mainland individual (excluded). Non-qualifying: 400,000 ÷ 10,000,000 = 4.0%. Below 5% and below AED 5M. Passes. The AED 400,000 is taxed at 9%. The AED 9.6 million at 0%.

Worked Example 2 Fails

Company B (JAFZA) has total revenue of AED 7.3 million. AED 6.1M from distribution (qualifying). AED 700,000 from leasing warehouse space to a mainland firm (excluded). AED 500,000 from services to mainland individuals (excluded). Total non-qualifying: AED 1.2M ÷ AED 7.3M = 16.4%. Exceeds 5%. Company B loses QFZP status entirely. All income taxable at 9%, producing approximately AED 624,750 in tax. Cannot reclaim QFZP status until 2031.

Worked Example 3 The AED 5 Million Cap

Company C (DIFC) has total revenue of AED 200 million. AED 192M from regulated fund management (qualifying). AED 8M from consulting to mainland individuals (excluded). Non-qualifying: 8M ÷ 200M = 4.0% below 5%. But AED 8M exceeds the AED 5M absolute cap. Fails despite being below 5%. This cap catches large businesses.

The Cost of Failure

You do not just pay 9% on excess non-qualifying income. You pay 9% on your entire taxable income for that year, and you are locked out for four more years. For Company B, the total additional tax over five years (assuming stable income) is approximately AED 3.1 million. For larger businesses, the figure can exceed AED 10 million. Additionally, if you filed as a QFZP and the FTA later determines you were not qualified, you face penalties for incorrect filing, potential interest, and a Voluntary Disclosure obligation for each affected year. This is why monitoring revenue streams monthly not annually is non-negotiable.

6. Substance Requirements: What “Adequate” Actually Means

The substance requirement separates genuine free zone operations from paper companies. Cabinet Decision No. 100 of 2023 requires that a QFZP’s core income-generating activities take place in the free zone. The FTA’s Free Zone Guide (CTGFZP1) provides examples, but the assessment is always case-by-case. The FTA has indicated that substance audits will be a focus in 2026.

Core income-generating activities (CIGAs) are the significant functions that drive business value. For a trading company: negotiation, execution, settlement of trades. For a consulting firm: delivery of advisory services. For a holding company: strategic decision-making. For a manufacturer: production oversight, quality control. Administrative functions like HR, IT support, basic bookkeeping, and office management are not CIGAs.

To satisfy the substance test, you need three things in your free zone:

1. Adequate qualified employees. People with the skills and authority to perform CIGAs, physically based in the free zone. A single visa holder working remotely from mainland Dubai does not count.

2. Adequate assets. Office space, equipment, technology needed for CIGAs. A virtual office or flexi-desk is unlikely to satisfy this for a manufacturing or trading business, though it may be adequate for a holding company.

3. Adequate operating expenditure. Meaningful operating costs in the free zone: rent, salaries, utilities, professional fees. The FTA looks for a business that genuinely operates from the free zone, not one that merely parks a license there.

Outsourcing CIGAs: You can outsource to related parties or third parties in a UAE free zone only. For qualifying intellectual property, outsourcing is more flexible: to any UAE party or non-related parties outside the UAE. In all cases, you must maintain documented supervision.

7. The IP Nexus Formula: How Qualifying IP Income Is Calculated

If your QFZP earns income from qualifying intellectual property (patents, copyrighted software, or functionally equivalent rights), the qualifying portion is determined by a nexus formula in Article 4 of Ministerial Decision No. 229 of 2025, based on OECD BEPS guidelines.

The formula: Qualifying IP Income = (Qualifying Expenditure + Uplift Expenditure) ÷ Overall Expenditure × Overall Income from Qualifying IP

Qualifying Expenditure: R&D costs incurred directly by the QFZP, or outsourced to unrelated parties.

Uplift Expenditure: Qualifying Expenditure increased by 30%, capped at Overall Expenditure. Rewards businesses that do R&D themselves.

Overall Expenditure: Total expenditure on the IP, including acquisition costs and related-party R&D. If you acquired the IP rather than developing it, the qualifying ratio drops.

Practical implication: If you bought a patent from a related party and did minimal R&D yourself, most of your IP income will be taxed at 9%. If you developed the IP in-house with your free zone R&D team, more qualifies for 0%. The FTA requires full documentation proving ownership and detailed R&D expenditure records.

8. Designated Zones vs. Free Zones: Why the Distinction Matters

Free Zone (for corporate tax purposes) is any zone listed under UAE legislation. DMCC, IFZA, DIFC, ADGM, Meydan, RAK ICC, and dozens more. Being in a free zone is one of the six QFZP conditions.

Designated Zone (for VAT purposes) is a subset of free zones meeting specific criteria under Cabinet Decision No. 59 of 2017. JAFZA, SAIF Zone, and Khalifa Industrial Zone are examples. Only businesses in Designated Zones can claim the “distribution of goods in or from a Designated Zone” qualifying activity under paragraph (k) of MD 229/2025.

If your free zone is not a Designated Zone, you cannot use the distribution qualifying activity, even if you physically import and re-export goods. Check whether your free zone is a Designated Zone before building your QFZP strategy around distribution. For VAT purposes, goods transferred from a Designated Zone to the mainland are treated as an import and trigger a VAT obligation reflected in your VAT return.

9. QFZP Status During the Start-Up Phase

Can you claim QFZP status with no revenue yet? Based on the FTA’s Free Zone Guide (CTGFZP1), yes with conditions. If your company is in a genuine start-up phase with no revenue, the absence of qualifying income does not automatically disqualify you. You can file as a QFZP anticipating future qualifying income. However, there is no income to benefit from the 0% rate during this period.

Watch out for interest income: If your start-up deposits working capital in an interest-bearing account, that income needs assessment. Treasury for own account is now a qualifying activity under MD 229/2025, which helps. But for start-ups with zero qualifying revenue, even small non-qualifying amounts represent 100% of total revenue, potentially triggering the de minimis threshold.

Our recommendation: maintain substance requirements (office, employees, assets) and keep detailed records of your business plan, licence activities, and intended operations. If the FTA queries your QFZP claim during a start-up period, demonstrate you are a genuine business with a credible path to qualifying income.

10. Transfer Pricing Obligations for QFZPs

QFZPs are subject to full transfer pricing compliance under Ministerial Decision No. 97 of 2023. Every transaction with a related party free zone, mainland, or overseas must be at arm’s length terms and documented accordingly.

Why this matters more for QFZPs: When a QFZP transacts with a related mainland company, there is a direct tax incentive to shift profits to the 0%-taxed entity. The FTA scrutinises this closely. Charging above-market management fees from a QFZP to mainland subsidiaries, or below-market prices on goods flowing from mainland to a JAFZA entity, are classic transfer pricing risks.

QFZPs must maintain a disclosure form with their corporate tax return and, where required, a master file and local file. The local file must include functional analysis, comparability analysis, and transfer pricing method documentation. The FTA can request this at any time during an audit. If your accounting records do not clearly separate related-party transactions, restructure your chart of accounts before year-end.

11. When the 0% Rate Is Not Worth It: QFZP vs. Mainland Comparison

The 0% rate comes with costs and restrictions that reduce or eliminate the advantage for certain businesses:

Factor | QFZP (Free Zone) | Mainland (9% Rate)

Tax rate on qualifying income | 0% | 9% (0% on first AED 375K)

Mandatory audit | Yes, at all revenue levels | Only if revenue exceeds AED 50M

Transfer pricing compliance | Full compliance required | Full compliance required

Small Business Relief | Not available | Available (revenue < AED 3M, until Dec 2026)

Tax loss carryforward | Not available | Available (10-year carryforward)

Group relief / loss transfers | Not available | Available

Business restructuring relief | Not available | Available

Tax group formation | Not available | Available

Selling to mainland individuals | Excluded activity (risks QFZP) | No restriction

Revenue from immovable property | Excluded (except FZ commercial) | Taxable at 9% but no QFZP risk

Compliance cost | Higher (audit + TP + monitoring) | Lower for small businesses

Risk of disqualification | 5-year lockout if conditions fail | Not applicable

When mainland may be better: If your free zone company earns less than AED 3 million in revenue and could benefit from Small Business Relief (which treats taxable income as zero under Ministerial Decision No. 73 of 2023), the net tax outcome is the same as QFZP, but without the mandatory audit, substance monitoring, or five-year disqualification risk. Note Small Business Relief expires 31 December 2026, so this changes from 2027.

When QFZP is clearly better: If your free zone company generates AED 5 million+ in annual profit from qualifying activities, the tax saving at 0% (AED 450,000+ per year vs. 9%) far outweighs compliance costs. The net benefit grows with scale.

12. Key Changes Under Ministerial Decisions 229 and 230 of 2025

In August 2025, the Ministry of Finance issued Ministerial Decision No. 229 of 2025 and Ministerial Decision No. 230 of 2025, both effective retroactively from 1 June 2023. Key changes:

Expanded commodity trading: Broader definition of qualifying commodities. No longer need to be in “raw form.” Goods packaged for retail sale still excluded. Structured financing transactions now included.

51% revenue test: If 51%+ of revenue comes from distribution, warehousing, logistics, or inventory management, you do not qualify under commodity trading.

Treasury for own account: Investment income on QFZP’s own surplus funds now expressly qualifying.

Audit standards: References Ministerial Decision No. 84 of 2025. QFZPs must have audited financials for all periods from 1 June 2023. If your 2023/24 financials are not yet audited, address this urgently.

Because both decisions are retroactive, review positions taken in prior-year corporate tax returns. The penalty regime makes voluntary correction cheaper than being caught during an FTA audit.

13. How to File as a QFZP: Practical Steps

QFZP status is declared on your annual corporate tax return through the FTA’s EmaraTax portal. No separate application. Here is the process:

Step 1: Register for corporate tax. Obtain a TRN from the FTA. If already VAT-registered, you use the same EmaraTax account but need a separate CT registration.

Step 2: Prepare your financials. Engage an auditor for audited statements under ISA/IFRS. Your accounting records must clearly separate qualifying income, non-qualifying income, and DPE revenue. Restructure your chart of accounts if needed.

Step 3: Prepare transfer pricing documentation. Complete the transfer pricing disclosure form that accompanies the return. Prepare master file and local file if related-party transactions exceed thresholds.

Step 4: Calculate your de minimis position. Map every revenue stream. If close to either threshold, review whether transactions can be restructured within the law.

Step 5: File the corporate tax return. Select QFZP status and report qualifying (0%) and non-qualifying (9%) income separately. Due within nine months of year-end. For December 2025 year-ends: 30 September 2026. For June 2026 year-ends: 31 March 2027.

Step 6: Pay any tax due. 9% on non-qualifying income. Payment due same deadline as return. Late payment triggers penalties.

✅ Need Help With Your QFZP Filing? Book a Free Consultation

14. How E-Invoicing Will Affect Free Zone Companies from Mid-2026

Starting July 2026, the UAE begins its phased rollout of mandatory e-invoicing. For QFZPs, the implications are significant. When every invoice is transmitted digitally through an Accredited Service Provider, the FTA will see, at a transaction level, who your customers are (free zone vs. mainland vs. individual), what activities the invoice relates to, and how revenue breaks down. Discrepancies between e-invoicing data and your corporate tax return’s qualifying vs. non-qualifying breakdown will be flagged automatically.

Free zone companies estimating their de minimis position at year-end or approximating revenue classifications will find that approach no longer viable once e-invoicing is mandatory. Every invoice needs correct categorisation in real-time. The businesses that will manage this smoothly are those with clean accounting systems and proper revenue stream tagging already in place.

15. QFZP Compliance Checklist for 2026

Review these items quarterly not just at year end to course-correct before a breach becomes permanent:

1. Confirm your entity is legally registered in a UAE free zone and the registration is active.

2. Map every revenue stream to a qualifying activity. Flag any involving natural persons, mainland immovable property, direct insurance, or banking.

3. Calculate your non-qualifying revenue percentage monthly. Set an internal alert at 3% as a buffer before the 5% threshold.

4. Verify CIGAs are performed by qualified personnel physically in the free zone.

5. Confirm adequate physical presence: office space, equipment, and assets matching the scale of operations.

6. Ensure operating expenditure in the free zone is proportionate to income claimed as qualifying.

7. Review all outsourcing. If CIGAs are outsourced, confirm the recipient is in a UAE free zone with documented supervision.

8. Engage an auditor for annual financial statements. Mandatory regardless of revenue size.

9. Prepare transfer pricing documentation for all related-party transactions.

10. Review new contracts or activities each quarter. Assess impact on QFZP status and de minimis.

11. Cross-reference corporate tax position with VAT filings. Revenue inconsistencies are a primary FTA audit trigger.

12. File corporate tax return within nine months of financial year-end.

13. Begin e-invoicing preparation if revenue exceeds AED 50M (mandatory January 2027) or plan for the July 2027 universal deadline.

Frequently Asked Questions

What is a Qualifying Free Zone Person in UAE corporate tax?

A QFZP is a legal entity registered in a UAE free zone that meets specific conditions under Article 18 of the Corporate Tax Law: deriving qualifying income, maintaining adequate substance, preparing audited financial statements, staying within the de minimis threshold, and not electing into the standard 9% regime. Qualifying income is taxed at 0%.

Do free zone companies have to pay corporate tax in the UAE?

Yes. All free zone companies are taxable persons and must register with the FTA, file annual returns, and comply with all reporting requirements including transfer pricing. The only benefit of QFZP status is that qualifying income is taxed at 0% instead of 9%. Non-qualifying income is always taxed at 9%.

What happens if my free zone company fails the QFZP conditions?

You lose QFZP status from the start of the tax period. Your entire income for that year is taxed at 9%. You are also disqualified for the next four consecutive tax periods. You can only retest in the sixth year.

Can I sell to mainland UAE customers and still be a QFZP?

It depends on the activity. Services to mainland corporates under qualifying activities generally produce qualifying income. Transactions with natural persons (individuals) are excluded activities. Selling goods from outside a Designated Zone to mainland is problematic. Each transaction must be individually assessed.

Is the audit mandatory for all free zone companies?

Yes, if claiming QFZP status. All QFZPs must have audited financial statements regardless of revenue. Mainland companies only need audits if revenue exceeds AED 50 million. This is a key cost difference.

What is the de minimis rule for QFZPs?

Non-qualifying revenue must not exceed 5% of total revenue or AED 5 million, whichever is lower. Exceeding this triggers full disqualification for the current year and the next four years.

Can a free zone company benefit from Small Business Relief?

No. QFZPs are excluded from Small Business Relief under Ministerial Decision No. 73 of 2023. If your free zone company has revenue under AED 3 million, evaluate whether opting out of QFZP status and claiming Small Business Relief (until 31 December 2026) produces a better outcome after accounting for audit costs saved and loss carryforward benefits gained.

How did the 2025 Ministerial Decisions change QFZP rules?

MD 229/2025 expanded commodity trading, introduced the 51% revenue test, allowed treasury for own account, and referenced MD 84/2025 audit standards. MD 230/2025 specified recognised price reporting agencies. All retroactive to 1 June 2023.

What is the difference between a Free Zone and a Designated Zone?

A Free Zone is any zone under UAE legislation. A Designated Zone is a subset meeting specific VAT criteria under Cabinet Decision No. 59 of 2017. Only Designated Zone businesses can use the distribution qualifying activity. Not all free zones are Designated Zones.

Do QFZPs need transfer pricing compliance?

Yes. Full compliance under Ministerial Decision No. 97 of 2023. All related-party transactions must be at arm’s length. The FTA scrutinises QFZP intercompany pricing closely because of the 0% vs. 9% profit-shifting incentive.

Conclusion: The 0% Rate Is Powerful, But It Demands Precision

The UAE’s free zone corporate tax regime remains one of the most attractive in the world. A genuine 0% rate on qualifying income, backed by a transparent legal framework and over 40 designated free zones, is a powerful incentive. But the days of simply holding a free zone license and assuming you pay no tax are over.

The QFZP regime requires continuous compliance across six conditions, with the de minimis threshold acting as a tripwire that can cost millions over a five-year lockout. The 2025 amendments, while expanding certain qualifying activities, tightened the rules around genuine trading versus logistics relabelling. From mid-2026, e-invoicing will give the FTA real-time visibility into whether your revenue streams match your corporate tax return.

The businesses that benefit most are those that understand exactly where their income sits, monitor quarterly, invest in substance, and work with advisors who know qualifying from excluded at a transaction level.

At UAE Tax Filing, we specialise in free zone corporate tax compliance. We help businesses assess QFZP eligibility, structure operations to protect the 0% rate, prepare audited statements, handle annual filing, manage VAT obligations, maintain proper accounting records, and monitor de minimis thresholds throughout the year.