On February 23, 2026, the UAE Ministry of Finance published the official Electronic Invoicing Guidelines, Version 1.0. Three documents dropped simultaneously: the main implementation guideline, the Accredited Service Provider (ASP) selection guide, and the mandatory fields specification. After two years of announcements, consultations, and postponements, the rules are now final. The technical architecture is defined. The deadlines are confirmed. The penalties are published. As Middle East Briefing reported, the UAE has moved decisively from legislative design to operational execution.

For most UAE businesses, the headline that matters is this: your existing invoicing process, whether it involves PDFs, paper invoices, or emailed Excel files, will stop being legally valid for B2B and B2G transactions by 2027. Every invoice you issue to another business or a government entity must be in structured XML format, transmitted through an Accredited Service Provider on the Peppol network, and reported to the FTA in near real-time. The PDF you email to your client today will not qualify as a valid invoice tomorrow.

Our original e-invoicing preparation guide covered the early framework when details were still emerging. This article updates that guide with everything that changed on February 23, translates the regulatory language into plain decisions for SME owners, and provides the practical action plan your business needs before the July 2026 pilot begins.

"Most of our clients still invoice by PDF. Some still use Word documents. The February 23 guidelines made it clear that none of these will be valid once e-invoicing becomes mandatory. The good news is that SMEs have until July 2027. The bad news is that the system changes required to get there take 6 to 12 months. If you start in January 2027, you will not be ready by July."

Jazim, CEO, UAE Tax Filing LLC

What Changed on February 23, 2026

Before February 23, e-invoicing in the UAE was a policy direction with a timeline. After February 23, it is a technical specification with mandatory fields, defined architecture, and confirmed penalties. The Ministry of Finance guidelines published three things that were previously missing:

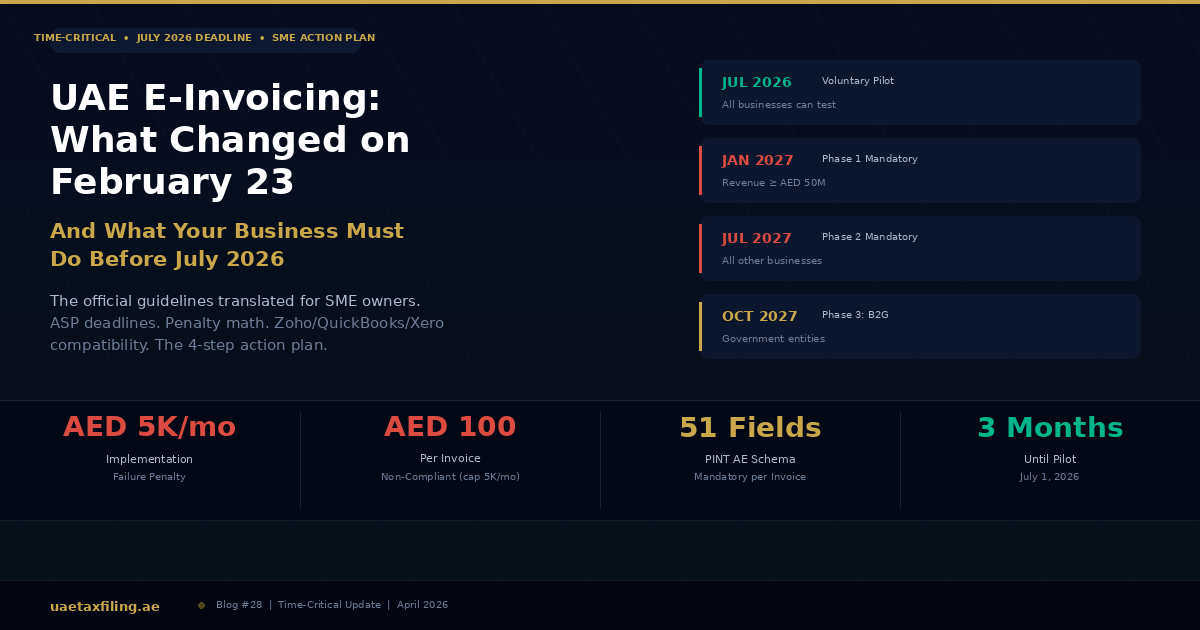

The PINT AE schema with 51 mandatory fields. Every electronic invoice must now contain 51 specific data elements in a structured format. These are not optional metadata. They are mandatory fields that the ASP validates before transmitting the invoice. Missing a single field means the invoice is rejected by the system. The fields include standard information (supplier TRN, buyer TRN, invoice number, date, line items, VAT amounts, totals) and UAE-specific additions (currency codes, payment terms, delivery information, and tax category codes). The full specification follows the Peppol International Invoice format adapted for the UAE, hence 'PINT AE.' This is not a PDF with extra fields. It is a structured XML document that no human reads but every system must produce.

The 5-corner Peppol model confirmed. The UAE system uses a decentralized architecture where invoices flow from supplier (Corner 1) to the supplier's ASP (Corner 2), then to the buyer's ASP (Corner 3), then to the buyer (Corner 4). Simultaneously, Corner 2 reports the tax data to the FTA (Corner 5). As ClearTax's technical guide documented, both the supplier's and buyer's ASPs report to the FTA, giving the authority real-time visibility into every B2B transaction. This is continuous transaction control: the FTA sees every invoice as it is issued, not just at the end of the quarter when the VAT return is filed.

The ASP appointment deadlines finalized. The guidelines confirmed the exact dates for each phase. Phase 1 businesses (annual revenue AED 50 million or more) must appoint their ASP by July 31, 2026 and go live with mandatory e-invoicing by January 1, 2027. Phase 2 businesses (revenue under AED 50 million) must appoint their ASP by March 31, 2027 and go live by July 1, 2027. Government entities must be ready for B2G e-invoicing by October 1, 2027. As Tally Solutions' phase-by-phase guide confirmed, the voluntary pilot from July 1, 2026 is penalty-free, giving businesses a window to test their systems without risk.

The scope clarified: broader than most expected. E-invoicing applies to any person conducting business in the UAE, regardless of VAT registration status. This means even businesses below the AED 375,000 VAT registration threshold are in scope for e-invoicing if they issue invoices for B2B or B2G transactions. The guidelines also confirmed that intra-group transactions within a VAT group are in scope and not excluded solely because they are between group members. B2C transactions are currently excluded.

The Timeline: Four Phases, Three Deadlines, One System

July 1, 2026: Voluntary pilot begins. Any business can join voluntarily. No penalties apply during the pilot. The purpose is to test ASP connectivity, validate invoice formats, and identify system gaps before mandatory enforcement begins. Businesses participating in the pilot gain a significant advantage: they discover problems when the problems are free, not when they cost AED 5,000 per month. Our 2026 tax changes guide covered the pilot announcement before the February 23 details were published.

January 1, 2027: Phase 1 mandatory (revenue AED 50M+). All businesses with annual revenue of AED 50 million or more must have an active ASP, fully integrated e-invoicing systems, and the ability to issue every B2B and B2G invoice in structured XML format. PDFs issued after this date are not valid invoices for these businesses. The ASP must be appointed by July 31, 2026, giving these businesses approximately 5 months from the appointment deadline to go live. As Raes Associates documented, large businesses represent approximately 20% of VAT-registered taxpayers but account for over 80% of total invoice volume, which is why they are prioritized.

July 1, 2027: Phase 2 mandatory (all other businesses). This is the deadline that affects the majority of UAE SMEs. Every business conducting B2B or B2G transactions, regardless of revenue size or VAT registration status, must be fully e-invoicing compliant. The ASP appointment deadline is March 31, 2027. That gives you 3 months between appointing the ASP and going live, which is tight for businesses that have not started preparation. If your business uses Zoho Books, QuickBooks, Xero, or any other accounting platform, you need to confirm that your software either supports the PINT AE format natively or can integrate with an ASP that handles the conversion.

October 1, 2027: Phase 3 (B2G transactions). Federal and state government entities must be able to receive and process e-invoices by this date. For businesses that sell to government clients, this means your e-invoicing system must be fully operational before you can invoice any government entity after October 1, 2027.

Not sure which phase your business falls into or what your ASP appointment deadline is? Our accounting team assesses your e-invoicing readiness, identifies your phase, and helps you plan the transition. Message us on WhatsApp.

What an ASP Is and Why You Cannot Skip It

An Accredited Service Provider is a technology vendor certified by the UAE Ministry of Finance to handle the validation, conversion, transmission, and reporting of electronic invoices. Think of the ASP as the bridge between your accounting system and the FTA. Your system produces invoice data. The ASP converts it into the PINT AE XML format, validates it against the 51 mandatory fields, transmits it to the buyer's ASP, and simultaneously reports the tax data to the FTA.

You cannot transmit invoices directly to the FTA. The architecture requires an ASP as the intermediary. This is by design: the ASP ensures format compliance, data completeness, and validation before the invoice enters the system. An invoice that fails validation is rejected by the ASP, not by the FTA. You fix it before it becomes a compliance issue.

Choosing an ASP is a strategic decision. As Middle East Briefing's compliance checklist noted, the ASP sits at the center of validation, transmission, and compliance. The factors that matter: whether the ASP supports your accounting software (Zoho, QuickBooks, Xero, SAP, Oracle, Tally), the monthly cost per invoice or per transaction, the ASP's onboarding timeline (some ASPs need 2-3 months to integrate with your systems), and whether the ASP handles both the supplier side (sending invoices) and the buyer side (receiving invoices). The Ministry of Finance maintains a list of approved ASPs on its portal, and this list is expected to grow throughout 2026 as more providers complete their accreditation.

The appointment process. You appoint your ASP through the EmaraTax portal. The appointment must be completed before your phase deadline (July 31, 2026 for Phase 1, March 31, 2027 for Phase 2). Once appointed, the ASP begins the integration process with your accounting system. This integration involves data mapping (aligning your system's invoice fields with the 51 mandatory PINT AE fields), testing (generating sample e-invoices and validating them against the schema), and go-live (switching from PDF/paper to structured electronic invoices).

The Penalty Framework: What Non-Compliance Costs

Cabinet Decision No. 106 of 2025 establishes the administrative penalties for e-invoicing non-compliance. These penalties are separate from the VAT and CT penalty frameworks covered in our penalties guide. They apply specifically to failures related to the electronic invoicing system.

AED 5,000 per month for failure to implement the system or appoint an ASP by the deadline. This is a recurring monthly penalty that continues until compliance is achieved. If a Phase 2 business misses the July 1, 2027 deadline and does not implement until January 2028, the accumulated penalty is AED 30,000 (6 months x AED 5,000). This penalty applies even if the business continues to issue PDF invoices that are otherwise correct for VAT purposes. The issue is the format and transmission method, not the invoice content.

AED 100 per invoice or credit note not issued or transmitted in the correct format. This applies per individual invoice, capped at AED 5,000 per month. A business that issues 200 invoices per month and fails to transmit any of them electronically would face AED 5,000 per month (the cap), not AED 20,000. For low-volume businesses (under 50 invoices per month), the penalty is proportional: 50 non-compliant invoices = AED 5,000.

AED 1,000 per day for failure to notify the FTA of system failures. If your e-invoicing system goes down and you do not notify the FTA promptly, a daily penalty accrues until notification is made. This penalty incentivizes rapid communication with the FTA when technical problems occur, rather than silently reverting to PDF invoicing during outages.

The compounding math: A Phase 2 business that misses the July 2027 deadline and continues issuing PDFs for 6 months faces: AED 30,000 in implementation failure penalties (6 x AED 5,000) plus up to AED 30,000 in per-invoice penalties (6 x AED 5,000 cap). Total potential exposure: AED 60,000, plus any VAT-related penalties if the FTA determines that non-compliant invoices affect the accuracy of VAT returns.

The 4-Step SME Action Plan: What to Do Between Now and July 2027

This action plan is for Phase 2 businesses (annual revenue under AED 50 million), which represents the vast majority of UAE SMEs. If your revenue exceeds AED 50 million, your timeline is shorter and you should already be in active preparation.

Step 1: Assess Your Current Invoicing System (April to June 2026)

Start by answering three questions. First, what software do you use to generate invoices? If you use Zoho Books, QuickBooks Online, Xero, or a similar cloud platform, check whether the vendor has announced PINT AE support or ASP integration for the UAE. Most major platforms are expected to release e-invoicing modules in 2026, but the timeline varies by vendor. If you use Excel, Word, or a custom-built system, you will likely need to either switch to a platform that supports e-invoicing or use an ASP that accepts manual data uploads and converts them to XML.

Second, how many invoices do you issue per month? This determines the ASP pricing tier and the complexity of the integration. A business issuing 20 invoices per month has a different implementation path than one issuing 2,000. Third, do you issue invoices to government entities? If yes, you will need to be e-invoicing compliant for B2G transactions by October 1, 2027, which may affect your ASP selection (not all ASPs support B2G transmission from day one).

This assessment takes one to two weeks and costs nothing. Do it now so you have a clear picture of the gap between your current process and the required end state.

Step 2: Select and Appoint an ASP (July 2026 to March 2027)

Your ASP appointment deadline is March 31, 2027, but selecting the right ASP takes time. The Ministry of Finance maintains a list of approved providers on its portal. When evaluating ASPs, the criteria that matter most for SMEs are: compatibility with your accounting software, pricing (per-invoice fees vs monthly retainers), onboarding support (does the ASP handle the data mapping or do you need your own IT team?), and whether the ASP provides both sending and receiving capabilities.

For businesses using standard cloud accounting platforms, the ASP integration may be as simple as connecting a module. For businesses using custom ERP systems, the integration may require development work. Get quotes from at least two ASPs. Compare not just the monthly cost but the onboarding timeline and the level of support provided during the transition period.

Consider joining the voluntary pilot (starting July 1, 2026) if your ASP is ready. The pilot is penalty-free and gives you a risk-free window to test the system with real invoices. As Tally Solutions noted, businesses that voluntarily implement e-invoicing are not subject to administrative penalties during the pilot phase, and the testing period provides an effective way to identify gaps before mandatory enforcement begins.

Step 3: Integrate and Test (January to May 2027)

Once your ASP is appointed, the integration work begins. This involves data mapping (aligning your invoice fields with the 51 PINT AE mandatory fields), system configuration (connecting your accounting software to the ASP's transmission platform), testing (generating sample invoices, transmitting them through the ASP, and validating that the FTA receives the data correctly), and staff training (your accounts team needs to understand the new workflow, including how to handle invoice rejections, credit notes, and system errors).

The testing phase is critical. A single missing mandatory field causes invoice rejection. A mismatched TRN causes validation failure. A currency code error causes the invoice to be flagged. These are not complex errors, but they require that every field in your system produces data in the exact format the PINT AE schema expects. Test with at least 50 invoices across different invoice types (standard, credit note, debit note) before going live.

This step interacts with your VAT return process. Once e-invoicing is live, the FTA will have real-time visibility into every invoice you issue. Your quarterly VAT return must reconcile perfectly with the invoices transmitted through the ASP. Any discrepancy will be flagged automatically. Our 9 mistakes article covered the VAT-CT revenue mismatch as the number one automated audit trigger; e-invoicing will add a third data source (the ASP transmission log) to the cross-referencing.

Step 4: Go Live and Monitor (June to July 2027)

By June 2027, your system should be producing compliant e-invoices for every B2B transaction. The go-live is not a single-day event but a transition: you stop issuing PDFs and start issuing structured XML invoices through your ASP. From July 1, 2027, every B2B invoice that is not transmitted through the e-invoicing system is non-compliant and attracts the AED 100 per-invoice penalty.

After go-live, monitor three things: invoice rejection rates (any rejected invoice means a data quality issue that needs fixing), ASP uptime (if the ASP has an outage, you must notify the FTA to avoid the AED 1,000/day penalty), and VAT return reconciliation (the invoices transmitted through the ASP must match the figures on your quarterly VAT return).

Our accounting team manages e-invoicing readiness as part of every engagement: assessing your current system, identifying your ASP options, coordinating the integration, and ensuring your VAT returns reconcile with the ASP transmission data. Talk to us on WhatsApp.

How E-Invoicing Changes Your VAT and CT Compliance

E-invoicing is not just an invoicing reform. It is a tax compliance reform. As The National reported, the tax impact comes from every transaction being reported in real-time to the FTA automatically. Applying the correct VAT treatment from the start becomes essential because there is no gap between issuing the invoice and the FTA seeing it.

Real-time FTA visibility into your transactions. Today, the FTA sees your data quarterly (when you file your VAT return) and annually (when you file your CT return). With e-invoicing, the FTA sees every B2B invoice as it is issued. This means errors that previously survived until the quarterly VAT return (an incorrect VAT rate, a missing TRN, an improperly classified zero-rated supply) are now visible immediately. The FTA's audit systems will cross-reference the real-time invoice data against your filed VAT returns, creating a triple-check: ASP data, VAT return data, and CT return data must all align.

The end of invoice manipulation. Backdating invoices, issuing invoices with incorrect amounts and correcting them later, or issuing invoices outside the accounting system will no longer be possible once e-invoicing is live. Every invoice is timestamped, transmitted, and recorded by the ASP. Every credit note must reference the original invoice. The FTA has a complete, tamper-proof record of every B2B transaction. For businesses with clean records, this changes nothing. For businesses with informal invoicing practices, this is a structural disruption.

Impact on CT record-keeping. The CT law requires seven years of record retention. E-invoicing automates part of this: the ASP stores transmitted invoices digitally, and the PINT AE format ensures they are structured, searchable, and audit-ready. However, e-invoicing only covers sales invoices and credit notes. Purchase invoices, contracts, bank statements, payroll records, and other supporting documents must still be maintained separately. Your IFRS financial statements and CT return working papers are not replaced by e-invoicing data.

Reverse charge transactions. Our reverse charge guide covered the January 1, 2026 changes that removed the self-invoicing requirement. Under e-invoicing, the reverse charge treatment must be correctly coded in the invoice's tax category fields. An imported service that triggers reverse charge must be identified as such in the PINT AE mandatory fields. Incorrect coding will cause the ASP to reject the invoice or, worse, transmit it with the wrong VAT treatment, creating a discrepancy with your VAT return.

Five Things SMEs Get Wrong About E-Invoicing

1. 'We have until 2027, so we do not need to start now.' The July 2027 deadline is the go-live date. The ASP appointment deadline is March 31, 2027. The integration and testing phase takes 3 to 6 months for most SMEs. If you appoint your ASP on March 31 and need 4 months to integrate, your earliest possible go-live is August 2027. You are already one month late and accumulating AED 5,000 per month in penalties. Start the assessment now. Appoint the ASP by late 2026. Begin testing in Q1 2027. Go live by June.

2. 'Our accountant will handle it.' Your accountant handles your books, your VAT returns, and your CT filing. E-invoicing is a technology integration project that involves your accounting software, an ASP, data mapping, API connections, and staff training. Your accountant needs to be involved (they must understand the new invoice workflow), but the implementation requires IT capability or ASP onboarding support that most accounting firms do not provide in-house. Ask your tax firm whether they offer e-invoicing readiness services or whether you need a separate technology partner.

3. 'We send PDFs by email, which is already electronic.' A PDF is not an e-invoice. An e-invoice is a structured XML document that meets the PINT AE schema, contains all 51 mandatory fields, and is transmitted through an ASP on the Peppol network. A PDF is an image of an invoice. It cannot be validated, transmitted, or reported automatically. Sending a PDF by email after July 2027 is the same as handing someone a paper invoice: the FTA does not see it, it does not satisfy the e-invoicing requirement, and it triggers the AED 100 per-invoice penalty.

4. 'E-invoicing only applies to VAT-registered businesses.' The February 23 guidelines explicitly state that e-invoicing applies to any person conducting business in the UAE, regardless of VAT registration status. If you issue B2B invoices, you are in scope. If you are below the AED 375,000 VAT registration threshold but still invoice other businesses for services rendered, you must comply with e-invoicing requirements. The invoicing mandate and the VAT registration threshold are separate obligations.

5. 'We can just use a free online XML converter.' The PINT AE schema is UAE-specific. Generic XML converters do not produce compliant output. The invoice must be transmitted through an approved ASP, not just converted to XML and emailed. The ASP validates the invoice against the schema, adds required metadata, transmits it on the Peppol network, and reports the tax data to the FTA. A DIY XML file uploaded to an email achieves none of this.

E-invoicing preparation is not optional and it is not something to start in 2027. We assess your current system, identify your phase deadline, recommend ASP options compatible with your accounting software, and coordinate the transition alongside your VAT and CT filing. Start the conversation on WhatsApp.

Frequently Asked Questions

When does e-invoicing become mandatory in the UAE?

January 1, 2027 for businesses with revenue of AED 50 million or more. July 1, 2027 for all other businesses. A voluntary pilot begins July 1, 2026.

What is an Accredited Service Provider (ASP)?

A technology vendor certified by the Ministry of Finance to validate, convert, transmit, and report electronic invoices on the Peppol network. You must appoint one before your phase deadline.

Are PDFs still valid invoices after the mandate?

No. Only structured XML invoices transmitted through an ASP are valid for B2B and B2G transactions after your mandatory compliance date. PDFs, paper invoices, and emailed spreadsheets are non-compliant.

Does e-invoicing apply to businesses that are not VAT-registered?

Yes. The February 23 guidelines confirm that e-invoicing applies to any person conducting business in the UAE, regardless of VAT registration status, for B2B and B2G transactions.

What are the penalties for not complying?

AED 5,000 per month for failure to implement the system or appoint an ASP. AED 100 per non-compliant invoice (capped at AED 5,000/month). AED 1,000 per day for failure to notify the FTA of system failures.

Are B2C transactions included?

Not currently. The 2026-2027 mandate covers B2B and B2G transactions only. B2C transactions are expected to be added in a future phase.

Will my accounting software support e-invoicing?

Major platforms (Zoho Books, QuickBooks Online, Xero, SAP, Oracle, Tally) are expected to release PINT AE modules in 2026. Check with your vendor for a confirmed timeline. If your software does not support it, your ASP may handle the format conversion.

How much does an ASP cost?

Pricing varies by provider and volume. Expect per-invoice fees (AED 0.50 to AED 5 per invoice) or monthly retainers (AED 500 to AED 5,000+ depending on volume and complexity). Get quotes from at least two providers.

Can I join the voluntary pilot?

Yes. Any business can join from July 1, 2026. No penalties apply during the pilot. It is the safest way to test your system before mandatory enforcement begins.

How does e-invoicing affect my VAT and CT filing?

The FTA will have real-time visibility into your invoices. Your VAT return figures must match the invoices transmitted through the ASP. Any discrepancy will be flagged automatically, adding a third cross-reference layer beyond the existing VAT-CT reconciliation.

The PDF Era Is Ending. The Preparation Window Is Open.

E-invoicing is the largest operational change to UAE tax compliance since VAT was introduced in 2018. It affects every business that issues invoices to other businesses or government entities, regardless of size or VAT registration status. The timeline is clear: voluntary pilot in July 2026, mandatory for large businesses in January 2027, mandatory for everyone by July 2027.

The businesses that start assessment now will choose their ASP calmly, integrate at their own pace, test during the penalty-free pilot, and go live with confidence. The businesses that wait until March 2027 will rush the ASP appointment, scramble through integration, skip testing, and face penalties from day one.

The February 23 guidelines removed the last excuse for waiting. The rules are published. The fields are defined. The deadlines are confirmed. The only remaining variable is whether your business starts preparing now or starts panicking later.

Start now.