If you own three companies, you file three corporate tax returns, manage three compliance calendars, and pay three separate CT liabilities. Your profitable trading company pays 9% on its gains while your loss-making startup burns through cash with no tax benefit until it eventually turns profitable on its own. Your total group tax bill is higher than it needs to be, and the administrative overhead is tripled.

Article 40 of the UAE Corporate Tax Law offers a solution: the tax group. Two or more related companies can elect to be treated as a single taxable entity, filing one consolidated return under one Tax Registration Number. Losses from one company offset profits from another. Intra-group transactions are disregarded. One return replaces three.

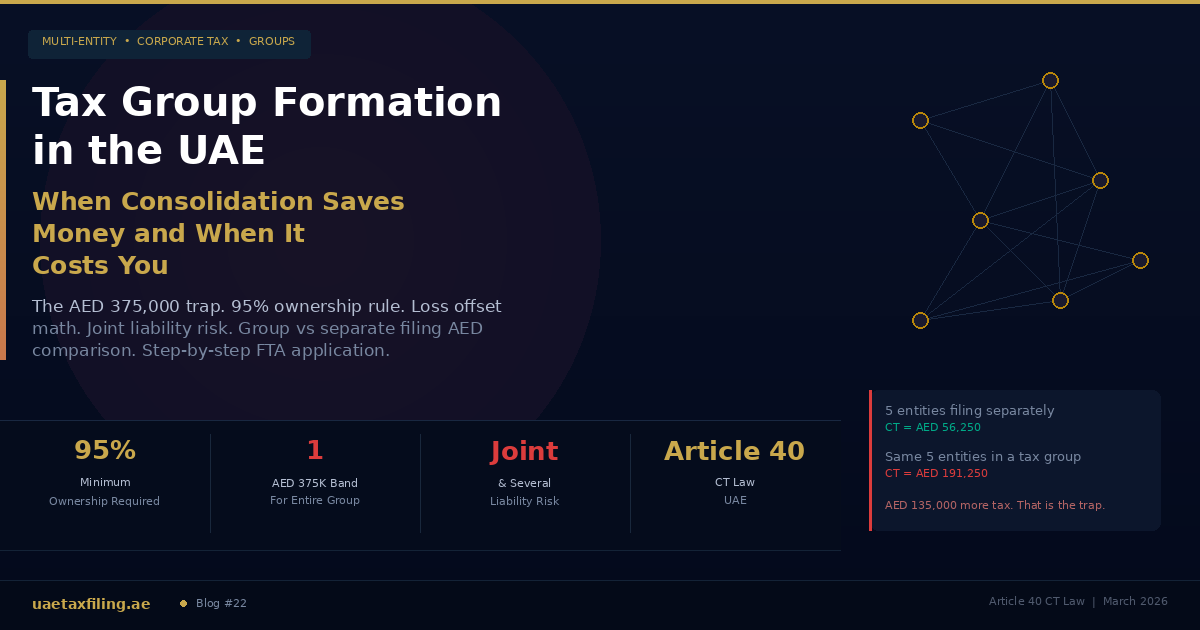

That sounds like an obvious win. In many cases, it is. But the tax group comes with a trap that nobody talks about plainly: when you consolidate, you lose four of those five AED 375,000 zero-rate bands. For groups of small, profitable companies, the cost of losing those bands can exceed the benefit of loss offset by AED 100,000 or more per year. As Khaleej Times reported, the decision to form a tax group requires a detailed evaluation specific to each entity structure.

"Tax groups are not a compliance shortcut. They are a strategic decision with permanent consequences. Joint and several liability means every entity in the group becomes responsible for every other entity's tax debt. You need to model both scenarios, group and separate, with real numbers before you apply."

Jazim, CEO, UAE Tax Filing LLC

What Is a Tax Group Under UAE Corporate Tax?

A tax group is a structure where two or more juridical persons (companies) elect to be treated as a single taxable entity for CT purposes. As defined in Article 40 of the Corporate Tax Law, once the FTA approves the application, the parent company becomes the representative member. It files one consolidated CT return on behalf of the entire group, prepares consolidated financial statements, and settles the group's CT liability.

The parent company receives a single Tax Registration Number (TRN) for the group. Each subsidiary retains its individual TRN for other purposes (such as VAT filing), but the CT filing is consolidated. The group operates as one taxpayer for CT, not multiple.

Tax groups are optional. As Sovereign PPG's guide explained, a tax group is only formed if the qualifying entities apply and the FTA approves. There is no automatic grouping, even for 100%-owned subsidiaries.

The 8 Eligibility Conditions

Every condition must be met. Failing on even one disqualifies the group. The FTA checks these at application and can dissolve a group if conditions are later breached.

The 95% rule is the strictest in the region. Compare this to the UAE VAT group formation threshold of just 50% control. A parent company that owns 90% of a subsidiary cannot include that subsidiary in a CT tax group. The 95% applies to share capital, voting rights, and entitlement to profits and net assets. All three must be at or above 95%. Ownership can be direct or through intermediary entities (e.g., Parent owns 100% of Holding Co, which owns 95% of Subsidiary = qualifies), but the chain must maintain the 95% level throughout.

QFZPs cannot join. This is the condition that surprises most free zone companies. A Qualifying Free Zone Person enjoying the 0% CT rate cannot be part of a tax group. If a free zone entity wants to join a group, it must opt out of the 0% rate and be taxed at 9% on all income. In most cases, this defeats the purpose. The exception is a free zone entity that is already paying 9% because its income is non-qualifying, in which case joining a group may enable loss offset that the entity cannot achieve alone.

Not sure if your multi-entity structure qualifies for a tax group? Our corporate tax team evaluates every condition, models both scenarios (group vs separate), and advises on the structure that minimizes your total CT liability. Message us on WhatsApp.

The AED 375,000 Trap: When Grouping Costs You More

This is the section no competitor publishes with clear AED math. Under UAE CT law, the first AED 375,000 of taxable income is taxed at 0%. This band applies per taxable person. When five companies file separately, each gets its own AED 375,000 band. When those same five companies form a tax group, the group gets one band. Five become one.

For groups of small, consistently profitable companies, this is devastating. Here is the math:

Filing separately, the five companies pay AED 56,250 in total CT. As a tax group, they pay AED 191,250. The group pays AED 135,000 more in tax every year for the privilege of filing one return instead of five. Over five years, that is AED 675,000 in additional CT that could have been avoided by staying separate.

This is not a theoretical edge case. It affects every group of related small businesses. A holding company with five restaurant outlets, each earning AED 400,000 to 600,000 in profit, will pay significantly more CT as a group than as separate entities. A family with five rental LLCs, each generating modest profits, faces the same math. The administrative convenience of one return does not justify AED 135,000 per year in additional tax.

When does the trap not apply? When one or more entities in the group are loss-making. The AED 375,000 band is irrelevant for a company with zero taxable income. A loss-making entity has no band to lose. If the group contains a mix of profitable and unprofitable companies, the loss offset benefit can outweigh the band reduction cost.

When Tax Groups Save Money: Loss Offset Between Entities

The primary tax benefit of a group is loss offset. Losses from one member reduce the taxable income of the group. Without a group, a loss-making company carries its losses forward and can only use them when that specific company becomes profitable. Inside a group, those losses reduce the group's consolidated taxable income immediately.

Filing separately, the profitable entity pays AED 236,250 in CT. The loss-making entity pays nothing and carries its AED 1,200,000 loss forward. As a group, the AED 1,200,000 loss reduces the group's taxable income from AED 3,000,000 to AED 1,800,000. Group CT: AED 128,250. The group saves AED 108,000 in the current year.

The loss-making entity also benefits: its AED 1,200,000 loss is used immediately rather than sitting unused on its balance sheet for years. As EAS MEA's strategic analysis noted, the ability to offset profits in one company with losses in another is the single most powerful benefit of a tax group, but it only matters when your group actually has a mix of profitability.

The decision framework: If all your entities are profitable and earning above AED 375,000 each, stay separate. If you have a meaningful spread between profitable and unprofitable entities, group formation can deliver five-figure annual savings. If your group is growing and you expect new subsidiaries to be loss-making in their early years, the group structure lets the established profitable entities absorb those startup losses immediately rather than waiting years for each new entity to become profitable on its own.

Beyond Loss Offset: Other Benefits of Tax Groups

Intra-group transactions disregarded. Transactions between group members are eliminated in the consolidated return. A management fee charged by the parent to a subsidiary does not create income for the parent or a deduction for the subsidiary at the group level. This simplifies transfer pricing compliance: within the group, you do not need to prove that every intercompany charge is at arm's length for CT purposes. Outside the group (transactions with non-members), transfer pricing rules still apply fully.

One CT return instead of multiple. Administrative efficiency is real. One EmaraTax submission instead of five. One IFRS consolidation instead of five separate sets of financial statements. One September 30 deadline instead of five. For groups with dedicated accounting support, this translates to measurable cost savings in professional fees.

Asset and liability transfers within the group. Transfers of assets and liabilities between group members can be done at tax net book value, meaning no gain or loss is recognized for CT purposes. This enables internal restructuring, asset consolidation, and operational optimization without triggering a CT event. However, if an asset is subsequently transferred to a non-group party within a specific period, the deferred gain may be 'clawed back' and become taxable.

The Critical Risk: Joint and Several Liability

This is the risk that every business owner must understand before signing a tax group application. As PwC documented, when a tax group is formed, the parent company and each subsidiary become jointly and severally liable for the group's CT obligations during the periods they are members.

Joint and several liability means the FTA can collect the entire group's tax debt from any single member. If Entity A owes AED 500,000 in CT and cannot pay, the FTA can demand payment from Entity B, Entity C, or the parent company. The FTA does not need to pursue Entity A first. It can go directly to whichever member has the most assets or the easiest collection path. The FTA's audit capacity is growing rapidly, with 93,000 inspection visits in 2024 alone, and the penalty framework for non-payment applies to any entity the FTA chooses to pursue within the group.

This risk is manageable when all entities are healthy and well-capitalized. It becomes dangerous when one member faces financial difficulty. If a subsidiary enters liquidation or insolvency while still a group member, the remaining members inherit its CT liability. The FTA can limit joint liability to specific members with prior approval, but this is not automatic and requires a separate application.

Before forming a tax group, ask: if the weakest entity in my group fails to pay its share of the CT bill, can the remaining entities absorb the full liability without distress? If the answer is no, the group structure may create more risk than it eliminates.

CT Tax Group vs VAT Tax Group: They Are Not the Same

A common misconception is that forming a CT tax group automatically creates a VAT tax group, or vice versa. As PwC's UAE group taxation guide confirmed, the CT and VAT group rules are entirely separate. Different ownership thresholds, different eligibility conditions, different formation processes. A company can be in a CT group but not a VAT group, or in a VAT group but not a CT group.

The most significant difference is the ownership threshold: 95% for CT groups versus 50% for VAT groups. A parent company with a 70% subsidiary can include it in a VAT group but not a CT group. The QFZP exclusion is another key difference: free zone entities at 0% CT cannot join a CT group but can join a VAT group.

For multi-entity businesses, this means you may need to manage two different group structures across two different taxes, with different members in each. Your VAT returns and your CT return will be filed by different group compositions. Your accounting team must track which entities are in which group for which tax.

How to Form a Tax Group: Step by Step

Step 1: Verify eligibility. Confirm all 8 conditions for every entity. Check ownership percentages, financial year-end dates, accounting standards, and QFZP/exempt status. If any entity fails any condition, it cannot be included.

Step 2: Model both scenarios. Calculate the total CT liability under separate filing AND under group filing. Include the AED 375,000 band impact, loss offset potential, and administrative cost savings. If group filing costs more in CT than it saves in administration, do not proceed.

Step 3: Prepare documentation. Gather trade licences, financial statements, organizational charts showing ownership percentages, and a signed consent from all entities agreeing to form the group.

Step 4: Submit the application. Apply through the FTA's EmaraTax portal. The parent company submits the application on behalf of all proposed members. The FTA reviews and either approves or requests additional information. As Shuraa Tax noted, the group formation is effective from the tax period specified in the application, unless the FTA sets a different date.

Step 5: Ongoing compliance. The parent company files consolidated CT returns, prepares consolidated financial statements, and manages all CT correspondence with the FTA on behalf of the group. New entities can be added to the group by submitting a notice to the FTA. Entities can leave the group, but the remaining members must still meet the eligibility conditions. If the parent company no longer qualifies, the group is dissolved.

If the group dissolves, each entity must re-register as an independent taxpayer and file individual returns going forward. Any deferred gains on intra-group asset transfers may crystallize on dissolution. Plan the exit before you plan the entry.

We model both scenarios for your specific group structure: total CT under separate filing vs group filing, with the AED 375K band impact, loss offset calculations, and joint liability assessment. Our corporate tax team handles the EmaraTax application while our accounting team prepares the consolidated financials. Start the conversation on WhatsApp.

Loss Transfer Without a Tax Group: The 75% Alternative

Forming a full tax group is not the only way to use losses across entities. The UAE CT law allows a separate mechanism: loss transfer between commonly owned entities, even without a tax group. Under this provision, a company can transfer its current-year losses to another company in the same group, provided the companies are at least 75% commonly owned (compared to 95% for a full tax group).

The 75% threshold makes this accessible to more structures, but the rules are stricter in other ways. The loss can only be transferred for the same financial year, meaning current-year losses only. Unlike inside a tax group where losses automatically offset consolidated profits, a loss transfer requires a specific election and documentation. The loss cannot be carried forward by the receiving company; it must be used in the year it is transferred.

This mechanism is valuable for groups that do not meet the 95% ownership threshold or that include QFZP entities (which cannot join a CT group but can participate in loss transfers at the 75% level, subject to conditions). It is also useful for groups that want the loss offset benefit without accepting the joint and several liability that comes with full group formation.

The interaction between loss transfers and Small Business Relief matters here. If the loss-receiving company has elected SBR, transferred losses are wasted because SBR already treats the company as having zero taxable income. As our SBR analysis explained, the election destroys the ability to use or receive transferred losses. If you have entities in both profit and loss positions, evaluate the loss transfer route before electing SBR for any entity in the group.

Timing: When to Form and When to Wait

As Khaleej Times reported, if all conditions are met from the start of the tax period, the group can be formed for that period. But if structural changes were made during the current period to meet the conditions (such as increasing ownership from 90% to 95%), the group cannot be formed until the following year.

This means planning ahead. If you intend to form a group for your 2026 tax period, the 95% ownership and all other conditions must be in place as of January 1, 2026 (for calendar-year companies). Acquiring the additional 5% of a subsidiary's shares in March 2026 does not qualify the group for 2026. You must wait until 2027.

The September 30, 2026 CT filing deadline applies to the group return just as it applies to individual returns. A newly formed group filing its first consolidated return faces the same deadline pressure, but with additional complexity: the IFRS consolidation process, elimination of intra-group transactions, and reconciliation of individual entity accounts into one consolidated set. Start the consolidation process in April, not September.

If you discover after filing individual returns that grouping would have been cheaper, it is too late for that period. The FTA does not allow retroactive group formation. The voluntary disclosure mechanism corrects errors in filed returns, but the choice to file separately versus as a group is a strategic election, not an error. Plan the structure before the period begins.

Planning a group structure for 2027? Our VAT and CT advisory team ensures your ownership, accounting standards, and financial year alignment are in place before the tax period starts. Talk to us on WhatsApp.

Frequently Asked Questions

What is a tax group under UAE corporate tax?

A structure where two or more related UAE companies are treated as a single taxable entity. The parent company files one consolidated CT return and settles CT on behalf of the entire group.

What is the ownership requirement for a UAE tax group?

The parent must hold at least 95% of each subsidiary's share capital, voting rights, and entitlement to profits and net assets. Ownership can be direct or through intermediary entities.

Can free zone companies join a tax group?

Not if they are Qualifying Free Zone Persons at the 0% CT rate. A QFZP must exit the 0% rate and be taxed at 9% to join a group. In most cases, this makes grouping disadvantageous for free zone entities.

What is the AED 375,000 trap?

Each company filing separately gets its own 0% band on the first AED 375,000 of taxable income. In a tax group, the entire group gets only one band. For groups of small, profitable companies, this means significantly higher total CT.

When does a tax group save money?

When the group has a mix of profitable and loss-making entities. Losses from one member offset profits of others immediately, reducing total group CT. The larger the losses relative to profits, the greater the saving.

What is joint and several liability?

Every member of the tax group is responsible for the entire group's CT liability. If one member cannot pay, the FTA can collect from any other member. This risk is the most important consideration before forming a group.

Can I add or remove entities from a tax group?

Yes. New entities can be added by notice to the FTA. Entities can leave, but the remaining group must still meet all eligibility conditions. If the parent company leaves or no longer qualifies, the group is dissolved.

Is a CT tax group the same as a VAT tax group?

No. They have different ownership thresholds (95% CT vs 50% VAT), different eligibility rules, and different formation processes. A company can be in one group but not the other.

How do I apply to form a tax group?

Through EmaraTax. The parent company submits the application with supporting documents (trade licences, financials, ownership charts, consent letters). The FTA reviews and approves or requests additional information.

What happens if a tax group is dissolved?

Each entity re-registers as an independent taxpayer and files individual returns. Deferred gains on intra-group asset transfers may become taxable on dissolution.

Group or Separate: The Answer Is in the Numbers

Tax group formation is a math problem, not a compliance convenience. The administrative savings from filing one return instead of five are real, but they are small compared to the potential CT impact of losing four AED 375,000 bands. Conversely, the loss offset benefit from grouping can deliver six-figure annual savings for structures that mix profitable and unprofitable entities.

The decision must be modeled with your specific numbers before any application is submitted to the FTA. What are each entity's projected profits and losses for the next three years? What is the total CT under separate filing? What is the total CT under group filing? What is the net difference? And critically: can every entity in the group absorb joint liability if one member defaults?

The businesses that get this right treat the tax group decision as a strategic investment, not a checkbox. They run the math annually, because the answer can change as entities grow, contract, or shift between profitability and loss. What saved you AED 108,000 this year might cost you AED 135,000 next year if your loss-making entity turns profitable.

Run the numbers. Then decide.