Every quarter, thousands of UAE businesses sit down to file their VAT return through the FTA’s EmaraTax portal, and every quarter, a significant number of them make avoidable mistakes that trigger penalties, attract audit attention, or leave money on the table. If you’ve been filing VAT returns since 2018, you might think you’ve got the process down. But 2026 has introduced changes that make accuracy more important than it has ever been.

The new penalty regime under Cabinet Decision 129/2025 takes effect on 14 April 2026, and it restructures how the FTA penalises late filings, late payments, and incorrect returns. On top of that, the 2026 amendments to the VAT Law and Tax Procedures Law have tightened input VAT recovery rules, introduced a five year limit on VAT refund claims, and expanded the FTA’s audit powers. The FTA conducted 93,000 inspection visits in 2024, a 135% increase from the prior year, and that pace is only accelerating in 2026.

This guide walks you through the entire quarterly VAT return filing process on the EmaraTax portal, box by box. More importantly, it flags the specific errors that get UAE businesses into trouble and shows you how to avoid them. Whether you handle VAT compliance in house or work with a tax consultant, this is the reference you need before your next filing deadline.

Book Your Free VAT Filing Consultation

1. Who Must File a VAT Return in the UAE

If your business is registered for VAT with the Federal Tax Authority, you must file a VAT return for every tax period, no exceptions. This applies whether you made taxable supplies during the period or not. Even a nil return (where you had no transactions) must be submitted. Skipping a period because “nothing happened” is one of the most common mistakes small businesses make, and it carries the same penalty as a late filing.

The mandatory VAT registration threshold in the UAE is AED 375,000 in annual taxable supplies. Businesses with taxable supplies or expenses between AED 187,500 and AED 375,000 can register voluntarily. Once registered, filing is compulsory regardless of turnover levels. This includes freelancers who hold a VAT registration, free zone companies making taxable supplies, and mainland LLCs of all sizes.

2. Quarterly vs. Monthly Filing: Which Applies to You

The FTA assigns your filing frequency when you register. Most businesses in the UAE file quarterly. Monthly filing is typically assigned to businesses with annual taxable supplies of AED 150 million or above, though the FTA retains discretion to assign monthly filing to other businesses based on risk profile or sector. You cannot change your filing frequency without FTA approval.

Your filing frequency, tax period dates, and due dates are all visible inside your EmaraTax account. Check this before every filing cycle. For quarterly filers, the standard periods are January to March, April to June, July to September, and October to December. The return and payment are both due within 28 days after the end of the tax period. For Q1 2026 (January to March), that means your filing deadline is 28 April 2026. If the 28th falls on a weekend or public holiday, the deadline extends to the next business day.

3. Documents You Need Before You Start

Filing a VAT return without your records in order is how errors happen. Before you log into EmaraTax, gather and reconcile the following for the quarter:

Sales records and tax invoices: Every tax invoice you issued during the period, organized by standard rated (5%), zero rated (0%), and exempt supplies. Your totals here must match your accounting records exactly. If you issued credit notes or debit notes during the quarter, these need to be factored into your adjustments.

Purchase records and supplier invoices: All invoices received from suppliers where you paid VAT. Verify that each invoice contains the supplier’s Tax Registration Number (TRN), the correct VAT amount, and a proper description of the goods or services. Under the 2026 amendments, the FTA can now deny input VAT recovery if the transaction is connected to tax evasion and you knew or should have known. Supplier due diligence is no longer optional.

Import records: Customs declarations for any goods imported into the UAE. If you imported services from outside the UAE, you must account for VAT under the reverse charge mechanism. Note that from 1 January 2026, self invoicing for reverse charge transactions has been removed. You no longer issue a tax invoice to yourself, but you still need supporting documents: contracts, purchase orders, delivery confirmations, and payment evidence.

Bank statements: Your bank records for the quarter, reconciled against your sales and purchase ledgers. The FTA cross references reported figures with financial data during audits, and discrepancies between your VAT return and your bank activity are a primary audit trigger.

Previous VAT return: Keep your last filed return accessible. You will need it to verify carried forward balances and ensure continuity between periods.

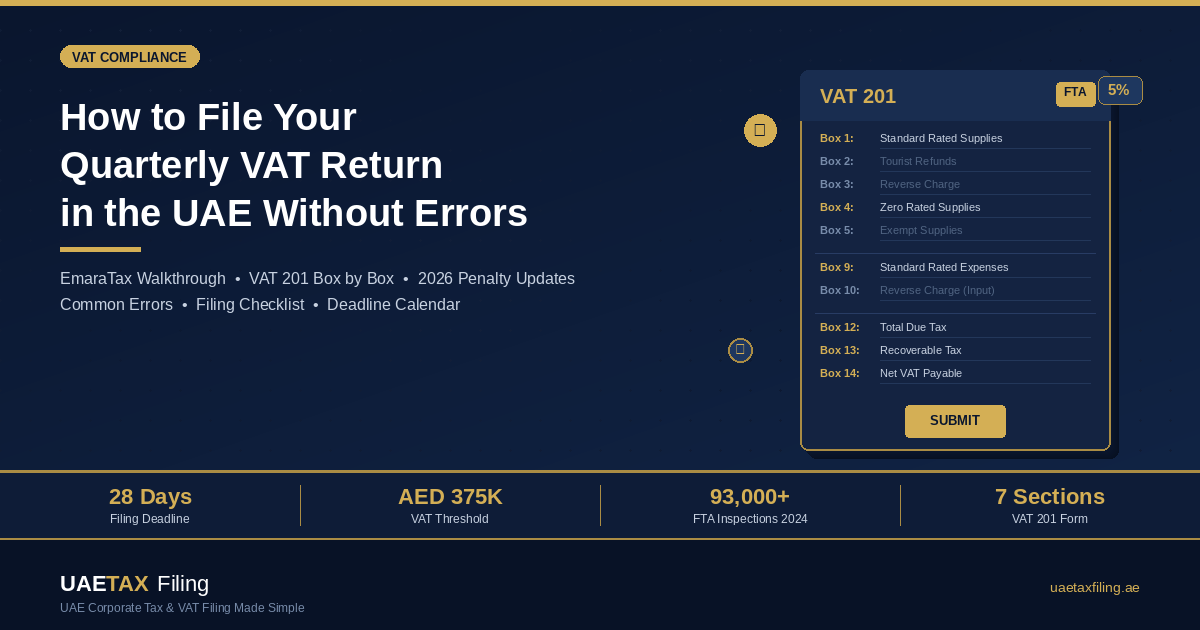

4. Step by Step: Filing the VAT 201 Form on EmaraTax

The VAT 201 is the standard return form used by all VAT registrants in the UAE. It is filed exclusively through the FTA’s EmaraTax portal. There is no offline submission option. Here is how to complete it, section by section.

Step 1: Log In and Access Your Return

Log into EmaraTax using your credentials or UAE Pass. Select your taxable person profile, then navigate to VAT, then My Filings, then View All. You will see a list of your tax periods. Click “File” next to the period you are submitting. The portal will display filing instructions. Read the checkbox declaration and click “Start.”

Step 2: Review Pre Populated Details

EmaraTax auto fills your TRN, business name, address, tax period dates, and return due date. Verify all of this. If anything is incorrect (for example, your address changed during the quarter), update your registration details separately before filing.

Step 3: VAT on Sales and All Other Outputs (Boxes 1 to 8)

This is where you report all VAT collected from customers during the period.

Box 1: Standard Rated Supplies in Each Emirate. This is the box that trips up the most businesses. You must report your standard rated (5%) supplies broken down by Emirate based on the place of supply rules, not where your office is located. For businesses with a single fixed establishment, the Emirate is straightforward. For businesses operating across multiple Emirates, you must allocate sales to each Emirate based on where the supply was made or received. Enter the net supply amount (excluding VAT) and the corresponding VAT amount.

Box 2: Tax Refunds Provided to Tourists. Only relevant if you participate in the Tourist Refund Scheme. Most businesses leave this at zero.

Box 3: Supplies Subject to Reverse Charge. Report the value of supplies you made where the recipient is responsible for accounting for VAT under the reverse charge mechanism. This typically applies to specific categories defined by the FTA.

Box 4: Zero Rated Supplies. Report all supplies taxed at 0%. This includes exports of goods and services, international transport, first supply of residential property within three years of completion, and certain education and healthcare supplies. You still report these even though no VAT is collected. Failing to report zero rated supplies is an error that can distort your return ratios and trigger FTA queries.

Box 5: Exempt Supplies. Certain financial services, bare land, local passenger transport, and residential property (after first supply) are exempt. Report the total value here. Remember: you cannot claim input VAT on purchases directly attributable to exempt supplies.

Boxes 6 and 7: Adjustments and Corrections. If you issued credit notes, made corrections to previously reported figures (where the error was AED 10,000 or less), or need to adjust for bad debts, enter the adjustments here. Errors above AED 10,000 cannot be corrected through the return. Those require a Voluntary Disclosure (Form 211).

Box 8: Totals. This is auto calculated by the portal. It sums your output VAT for the period. Double check that the total matches your own calculations before moving on.

Step 4: VAT on Expenses and All Other Inputs (Boxes 9 to 11)

Box 9: Standard Rated Expenses. Enter the total value of purchases on which you paid 5% VAT and the corresponding VAT amount. Only include purchases where you have valid tax invoices from VAT registered suppliers. If you are claiming input VAT on a purchase and the supplier’s TRN is invalid or the invoice is incomplete, the FTA can disallow the recovery during an audit.

Box 10: Supplies Subject to Reverse Charge (Input Side). If you imported services or certain goods and accounted for VAT under reverse charge, report both the output VAT (in Box 3) and the input VAT recovery here. The net effect is usually zero, but the reporting must be correct on both sides.

Box 11: Adjustments to Input VAT. Similar to the output adjustments, enter any corrections to input VAT here. This includes adjustments for partially exempt businesses using the input tax apportionment method. If this is the first return period of your tax year, check whether an annual adjustment is required.

Step 5: Net VAT Due (Boxes 12 to 15)

The portal calculates these automatically. Box 12 shows total output VAT due. Box 13 shows total recoverable input VAT. Box 14 shows the net amount: if output exceeds input, you owe the FTA. If input exceeds output, you have a credit. Box 15 lets you request a refund of excess recoverable tax. If you do not request a refund, the credit carries forward to the next period. Under the 2026 VAT amendments, refund claims are now subject to a strict five year limit from the end of the relevant tax period. Do not let credits sit indefinitely.

Step 6: Declaration and Submission

Scroll to the declaration section, verify the authorised signatory details, tick the confirmation box, and click Submit. You will receive a reference number and a confirmation email from the FTA. Download a copy of the submitted return for your records. You can edit the return until the filing deadline passes, but once the deadline is gone, any corrections require a Voluntary Disclosure.

Step 7: Make the Payment

Submitting the return and making the payment are two separate actions on EmaraTax. Filing the return on time but paying late still incurs a late payment penalty. Navigate to My Payments after submission and settle the amount due via bank transfer or approved payment gateway. The payment must clear into the FTA’s account by the deadline. Bank transfers initiated on the last day may not arrive in time, so pay early.

5. The Seven Most Common VAT Return Errors (and How to Avoid Them)

After years of working with UAE businesses on their VAT compliance, these are the errors we see most frequently. Every one of them is avoidable with the right process.

Error 1: Misclassifying supplies between standard rated, zero rated, and exempt. The boundaries are not always obvious. A common example: the first supply of a completed residential building is zero rated, but the subsequent supply of that same property is exempt. Getting this wrong affects both your output VAT and your input VAT recovery position.

Error 2: Claiming input VAT without valid tax invoices. You need a proper tax invoice from a VAT registered supplier to recover input VAT. A receipt or a proforma invoice is not sufficient. Verify that every invoice contains the supplier’s TRN, a sequential invoice number, the date of issue, the buyer and seller details, a line by line breakdown of goods or services, the VAT rate, and the VAT amount.

Error 3: Forgetting to report reverse charge transactions on both sides. The reverse charge must appear in your output (Box 3) and your input (Box 10). If you only record one side, the return is mathematically wrong, and the FTA’s systems will flag the discrepancy.

Error 4: Incorrect Emirate wise allocation. Box 1 requires standard rated supplies broken down by Emirate. Allocating everything to Dubai because that’s where your office sits is wrong if you made supplies in Sharjah or Abu Dhabi. The FTA uses this data for revenue distribution among the Emirates, and they check it.

Error 5: Not filing nil returns. If your business had no activity during a quarter, you still must file a return showing zeros. The FTA’s system does not distinguish between “didn’t file” and “filed late.” Both trigger the same penalty.

Error 6: Correcting errors above AED 10,000 in the next return instead of filing a Voluntary Disclosure. The law is specific: if an error affects your payable tax by more than AED 10,000, it must be corrected through a Voluntary Disclosure (Form 211). Correcting it in the next return does not satisfy the legal requirement and can result in additional penalties if discovered during an FTA audit.

Error 7: Filing on time but paying late. Many businesses treat the filing deadline and the payment deadline as separate. They are not. Both the return and the payment are due within 28 days of the period end. Under the new penalty regime effective 14 April 2026, late payment penalties compound quickly. A payment initiated on the last day via bank transfer that arrives a day late is treated as late.

6. VAT Return Filing Deadlines for Q1 to Q4 2026

Plan these into your financial calendar now. Missing any of them has become significantly more expensive under the revised penalty structure.

Tax Period | Period Dates | Filing and Payment Deadline

Q1 2026 | 1 January to 31 March | 28 April 2026

Q2 2026 | 1 April to 30 June | 28 July 2026

Q3 2026 | 1 July to 30 September | 28 October 2026

Q4 2026 | 1 October to 31 December | 28 January 2027

If the 28th falls on a Saturday, Sunday, or UAE public holiday, the deadline moves to the next business day. Always verify the exact date in your EmaraTax account, as the FTA may adjust dates in specific circumstances.

7. What Happens If You File Late or Incorrectly

The FTA does not issue warnings for late filings. Penalties are applied automatically through the system. Here is what you are looking at under the current and incoming penalty frameworks:

Late filing: Under the current regime, the first offence carries a penalty of AED 1,000. A repeat offence within 24 months doubles to AED 2,000. Under the new regime from 14 April 2026 onward, these amounts are restructured, but the principle remains: repeated non compliance escalates the cost every time.

Late payment: A percentage based penalty is applied to the outstanding VAT amount. The longer you wait, the more it compounds. This is the penalty that catches businesses off guard because it grows daily.

Incorrect returns: If an error results in underpaid tax and is discovered by the FTA (rather than voluntarily disclosed by you), the penalty can reach significant multiples of the unpaid amount. This is why voluntary disclosure before an audit is always cheaper than being caught.

The 2026 amendments also mean the FTA now cross references your VAT returns with your corporate tax filings. If your VAT return shows revenue of AED 5 million for the year but your corporate tax return shows AED 4.2 million, expect a query. Consistency across all your FTA filings has become a compliance requirement in practice, even if no single law says so explicitly.

8. How E Invoicing Will Change VAT Filing from Mid 2026

Starting July 2026, the UAE begins its phased rollout of mandatory e invoicing. While the first phase is voluntary, businesses with annual revenue of AED 50 million or more must comply by January 2027, and all VAT registered businesses must comply by July 2027.

E invoicing will fundamentally change how VAT returns work. When every invoice you issue and receive is transmitted in a structured digital format through an Accredited Service Provider, the FTA will have real time visibility into your transactions. This means discrepancies between your invoices and your VAT return will be flagged automatically, not just during audits. Businesses that have been filing approximate figures or rounding aggressively will find that approach no longer viable.

If your business is above the AED 50 million threshold, start evaluating Accredited Service Providers now. If you are below the threshold, use the lead time to clean up your invoicing processes. Proper invoicing today makes accurate VAT filing significantly easier, and it prepares you for the mandatory phases ahead.

9. Pre Filing Checklist: 10 Steps to an Error Free VAT Return

Use this checklist before every quarterly filing. Completing these steps before you log into EmaraTax will cut your filing time in half and virtually eliminate the risk of errors.

1. Reconcile your sales ledger to your bank deposits for the quarter.

2. Reconcile your purchase ledger to your bank payments for the quarter.

3. Verify every input VAT claim is supported by a valid tax invoice with a correct TRN.

4. Confirm the correct classification of all supplies: standard rated, zero rated, or exempt.

5. Allocate standard rated supplies to the correct Emirate based on place of supply rules.

6. Account for reverse charge transactions on both the output and input sides.

7. Process all credit notes and debit notes issued or received during the quarter.

8. Check for any errors from previous periods that require a Voluntary Disclosure.

9. Verify your VAT account balance and any carried forward credits from the prior period.

10. Confirm the payment method and ensure funds are available to pay before the deadline.

10. When to Handle Filing In House vs. When to Get Help

If your business has straightforward domestic sales at 5%, a small number of suppliers, and no imports or exports, filing your VAT return in house is entirely feasible. The EmaraTax portal is designed for self service, and with proper bookkeeping throughout the quarter, the actual filing takes less than an hour.

The picture changes when your business involves mixed supplies (standard rated, zero rated, and exempt), significant imports or exports, reverse charge obligations, inter company transactions, multi Emirate operations, or approaching the e invoicing thresholds. In these situations, the risk of error increases, and the cost of errors under the 2026 penalty regime makes professional support a sound investment rather than an expense.

At UAE Tax Filing, we handle quarterly VAT return preparation and filing for over 500 UAE businesses. Our process includes full reconciliation, supply classification review, input VAT verification, and portal submission. We have never missed an FTA deadline.

Frequently Asked Questions

How do I file a VAT return in the UAE step by step?

Log into the EmaraTax portal, navigate to VAT, then My Filings, then View All. Click File next to your current tax period. Complete the VAT 201 form by entering your output VAT (sales), input VAT (purchases), any adjustments, and review the net VAT due. Tick the declaration and click Submit. Then navigate to My Payments and settle any VAT due before the deadline.

What is the deadline for filing a VAT return in the UAE?

VAT returns must be filed and paid within 28 days after the end of the tax period. For quarterly filers, Q1 2026 is due by 28 April 2026, Q2 by 28 July 2026, Q3 by 28 October 2026, and Q4 by 28 January 2027. If the 28th falls on a weekend or public holiday, the deadline moves to the next business day.

Do I need to file a VAT return if I had no sales during the quarter?

Yes. Every VAT registered business must file a return for every tax period, even if there were no transactions. This is called a nil return. Failing to file a nil return carries the same penalty as filing any other return late.

What happens if I make an error on my VAT return?

If the error affects your payable tax by AED 10,000 or less, you can correct it in the next VAT return. If the error exceeds AED 10,000, you must file a Voluntary Disclosure (Form 211) through EmaraTax. Voluntary disclosure before an FTA audit results in significantly lower penalties than errors discovered during an audit.

Can the FTA reject my input VAT claim?

Yes. Under the 2026 VAT amendments, the FTA can deny input VAT recovery if the supply is connected to VAT evasion and the business knew or should have known. This makes supplier due diligence essential. Always verify your supplier’s TRN and ensure invoices meet all requirements.

How does e invoicing affect VAT return filing?

Starting mid 2026, e invoicing will give the FTA real time visibility into business transactions. Invoices will be validated digitally against VAT returns, making discrepancies immediately visible. Businesses should prepare by ensuring their invoicing processes are accurate and compliant before the mandatory phases begin.

What is the penalty for late VAT return filing in 2026?

Under the current regime, the first late filing incurs a penalty of AED 1,000, with repeat offences doubling to AED 2,000 within 24 months. The new penalty regime under Cabinet Decision 129/2025, effective from 14 April 2026, restructures these penalties. Late payment penalties are percentage based and compound over time.

Conclusion: File Accurately, File Early, File With Confidence

VAT return filing in the UAE is not particularly difficult when your records are in order and you understand what goes into each box of the VAT 201 form. The difficulty comes from neglecting the preparation: messy books, unverified supplier invoices, incorrect supply classifications, and last minute scrambles on deadline day.

With the 2026 penalty changes, expanded FTA audit activity, and the looming e invoicing mandate, the cost of getting it wrong is higher than it has ever been. But the path to getting it right is straightforward: keep clean records throughout the quarter, reconcile before you file, and submit early enough that your payment clears before the deadline.

If your business needs support with VAT return filing, quarterly reconciliation, or a full VAT compliance review, our team at UAE Tax Filing is ready to help. We handle everything from monthly bookkeeping to corporate tax filing, so your numbers are always audit ready.

Book Your Free VAT Filing Consultation