A Dubai LLC incorporated in September 2019. Seven years of trading, never heard of corporate tax until a client asked for the company's Tax Registration Number on a purchase order in early 2025. The owner checked EmaraTax and realized the company was not registered. By then, the registration deadline (October 31, 2024 for September-issued licences) had already passed. The FTA had already assessed the AED 10,000 late registration penalty. The owner had two reactions: panic about the penalty, and confusion about why nobody told them.

This story repeats across thousands of UAE businesses. The FTA reported over 543,000 CT registrations completed by the end of 2025, but the total number of businesses that should have registered is significantly higher. As Middle East Briefing documented, many businesses remain unaware that CT registration is mandatory for all juridical persons regardless of revenue, that the deadline was staggered by licence issuance month, and that missing the deadline carries a flat AED 10,000 penalty per entity. Some businesses with multiple trade licences owe AED 10,000 per licence.

There is, however, a lifeline. The FTA's Public Clarification CTP006, effective April 14, 2025, created a formal waiver for the late registration penalty. If you register late but file your first corporate tax return within seven months (instead of the standard nine) from the end of your first tax period, the AED 10,000 penalty is waived. If you already paid the penalty, the FTA credits or refunds it. As Flying Colour Tax's analysis documented, this is a genuine opportunity for thousands of businesses that missed their registration window.

This is the guide to CT registration from the beginning: who must register, when the deadline was (and what to do if you missed it), the CTP006 penalty waiver with worked examples, the EmaraTax registration process step by step, the documents required, and what happens after your TRN is issued. Our VAT registration guide covers the VAT side; this article covers the CT side. Together they are the two foundational registration articles every UAE business needs.

"Half the clients who come to us for CT filing have not registered yet. They assumed registration and filing were the same thing. They are not. Registration creates your TRN and tells the FTA you exist. Filing is the annual return you submit through that TRN. You cannot file without registering first, and you cannot register without paying the AED 10,000 penalty if you missed your deadline. Unless you know about CTP006."

Jazim, CEO, UAE Tax Filing LLC

Who Must Register for Corporate Tax

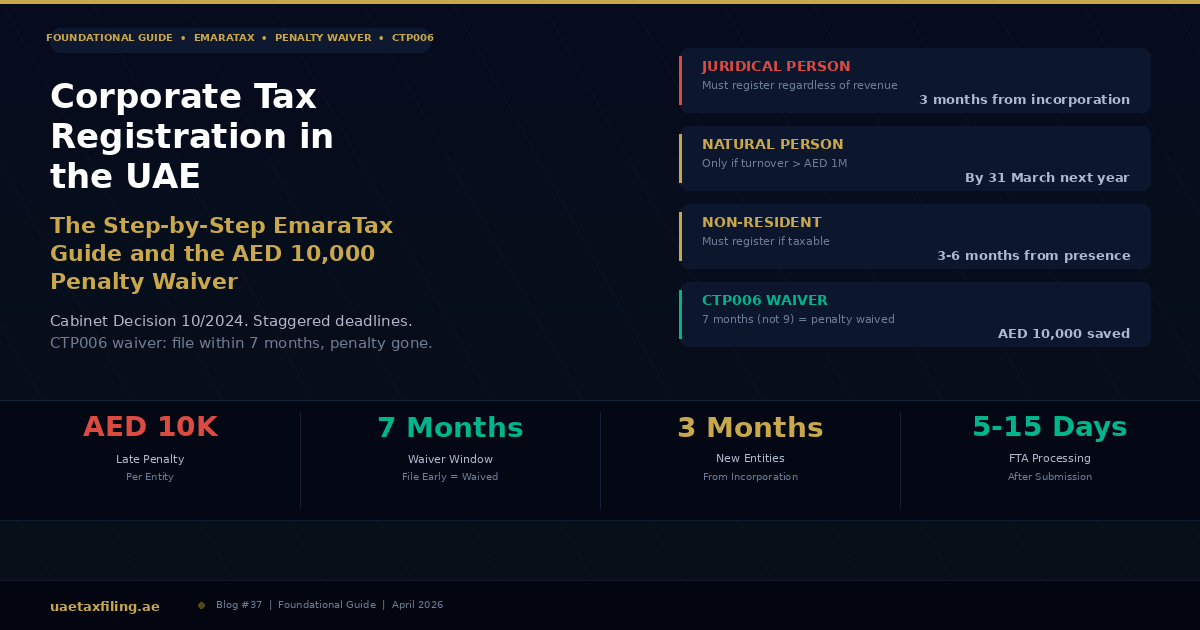

Article 51 of Federal Decree-Law No. 47 of 2022 requires every taxable person to register with the FTA and obtain a Tax Registration Number (TRN). As Deloitte's analysis of the registration decision documented, the obligation extends to every category of taxable person, and the FTA issued Decision No. 3 of 2024 to set specific deadlines for each category.

All juridical persons, regardless of revenue. Every UAE-incorporated company (LLC, sole establishment, civil company, partnership, free zone FZE, free zone FZCO), every branch of a foreign company registered in the UAE, and every entity established or recognized under UAE law must register. There is no revenue threshold for juridical persons. A company earning AED 0 and a company earning AED 100 million have the same registration obligation. The AED 375,000 figure that many businesses confuse with a 'registration threshold' is actually the zero-rate band: the first AED 375,000 of taxable income is taxed at 0%, and income above that is taxed at 9%. It has nothing to do with whether you need to register. As our real cost of CT article explains, many businesses owe AED 0 in tax but must still register and file.

Natural persons above AED 1 million turnover. Freelancers, sole proprietors, and individuals conducting business activity in the UAE must register only if their business turnover exceeds AED 1 million in a Gregorian calendar year. Turnover below AED 1 million does not trigger CT registration. Note that three income categories are excluded from the turnover calculation: employment income (salary), personal investment income (dividends, bank interest), and real estate investment income (rental income from property held without a licence). A freelancer earning AED 800,000 from consulting and AED 400,000 from rental income assesses the threshold on AED 800,000 only. Our freelancer CT guide and influencer guide cover the natural person rules in detail.

Non-resident entities with UAE presence. A foreign company with a Permanent Establishment (PE) in the UAE must register within six months of the PE's existence (for PEs established before March 1, 2024) or within six months from the date the PE is established (for PEs after March 1, 2024). A foreign company with a nexus in the UAE (earning UAE-source income without a PE) must register within three months. As Virtuzone's deadline guide confirms, non-resident companies deriving only state-sourced income without a PE or nexus are not required to register.

Exempt persons. Certain entities (government bodies, government-controlled entities meeting specific conditions, qualifying investment funds, pension funds, qualifying public benefit entities) may be exempt from CT but are still required to apply to the FTA for exempt status. This application is a form of registration. Exempt status is not automatic: you must apply, be approved, and maintain the conditions.

The Staggered Deadline Schedule: When Your Business Should Have Registered

FTA Decision No. 3 of 2024, effective March 1, 2024, established a staggered deadline system for resident juridical persons that existed before March 1, 2024. The deadline depends on the month in which the trade licence was originally issued, regardless of the year. As the FTA's official announcement confirmed, if a company holds multiple licences, the licence with the earliest issuance date determines the deadline.

The deadline schedule for pre-March 2024 entities:

January or February licence: deadline was May 31, 2024. March or April licence: deadline was June 30, 2024. May licence: deadline was July 31, 2024. June licence: deadline was August 31, 2024. July licence: deadline was September 30, 2024. August or September licence: deadline was October 31, 2024. October or November licence: deadline was November 30, 2024. December licence: deadline was December 31, 2024. Entities with no licence as of March 1, 2024: deadline was May 31, 2024.

For entities incorporated on or after March 1, 2024: the registration application must be submitted within three months from the date of incorporation, establishment, or recognition. A company incorporated on June 15, 2024 had a deadline of September 15, 2024. A company incorporated on January 10, 2026 has a deadline of April 10, 2026. This three-month rule applies to every new entity going forward and is the rule that most startups need to follow.

For natural persons: individuals whose business turnover exceeded AED 1 million during the 2024 calendar year had a registration deadline of March 31, 2025. For individuals exceeding the threshold in 2025, the deadline is March 31, 2026. The pattern continues each year: register by March 31 of the year following the year the threshold was crossed.

If you missed your deadline: Every deadline listed above has already passed. If your business has not yet registered, you are in late registration status and the AED 10,000 penalty has been assessed (or will be assessed when you register). The penalty is applied at the point of registration, not at the point of the missed deadline. Some businesses do not realize the penalty exists until they try to register and see it on their EmaraTax account. The good news: the CTP006 waiver may apply.

The CTP006 Penalty Waiver: How to Get the AED 10,000 Back

Public Clarification CTP006, effective April 14, 2025, is the FTA's formal initiative to waive the late registration penalty for businesses that act quickly on their first CT return. This is not a rumor, not an informal concession, and not a case-by-case exception. It is a published, structured waiver program with clear eligibility conditions. As Flying Colour Tax's detailed analysis confirmed, it applies to penalties arising from June 1, 2023 onward and covers both natural and juridical persons.

The eligibility condition: file your first corporate tax return within seven months from the end of your first tax period. The standard CT return deadline is nine months after the tax period ends. CTP006 shortens that to seven months for waiver eligibility. If you meet the seven-month window, the late registration penalty is waived. If you already paid the penalty, the FTA processes a credit to your EmaraTax corporate tax account or a refund upon application.

Worked examples

Example 1: Calendar-year company. First tax period: January 1, 2024 to December 31, 2024. Standard return deadline: September 30, 2025 (9 months). CTP006 waiver deadline: July 31, 2025 (7 months). If the company registered late but filed its first CT return by July 31, 2025, the AED 10,000 penalty is waived.

Example 2: April-March financial year. First tax period: April 1, 2024 to March 31, 2025. Standard return deadline: December 31, 2025. CTP006 waiver deadline: October 31, 2025. File by October 31 and the penalty is waived.

Example 3: New company incorporated July 2024. Registration deadline: October 2024 (3 months from incorporation). Company did not register until February 2025. AED 10,000 penalty assessed. First tax period ends December 31, 2024. CTP006 waiver deadline: July 31, 2025. If the company files its first return by July 31, 2025, the penalty is waived despite the late registration.

How to claim the waiver. Register for CT on EmaraTax (even if late). Prepare and file your first CT return within the seven-month window. The FTA's system automatically checks the filing date against the CTP006 condition. If the condition is met and the penalty has not yet been paid, it is waived from the account. If the penalty has already been paid, the FTA credits the amount to the EmaraTax account; a formal refund application may be needed to transfer the credit to the business's bank account.

The waiver has an expiry risk: The seven-month window from your first tax period end is fixed. It does not extend because you registered late. A business with a first tax period ending December 31, 2024 must file by July 31, 2025 regardless of when it actually registered. If it registers in August 2025 (after the seven-month window has already closed), the waiver is no longer available. Register and file as quickly as possible to preserve the waiver window.

The CTP006 waiver is time-sensitive and requires your first CT return to be filed correctly and on time. Our corporate tax team handles the entire process: late registration on EmaraTax, first return preparation, and filing within the seven-month window to trigger the waiver. Message us on WhatsApp.

The EmaraTax Registration Process: Step by Step

All CT registration is handled through the FTA's EmaraTax portal. There is no offline alternative. The process takes approximately 15-20 minutes if you have all documents prepared. The FTA typically processes applications within 5 to 15 business days.

Step 1: Create or access your EmaraTax account

If you already have an EmaraTax account (from VAT registration or excise registration), log in with your existing credentials. If this is your first interaction with EmaraTax, create a new account using a valid email address and UAE mobile number for two-factor authentication. The FTA recommends linking your account to UAEPass for identity verification. For companies, the person creating the account must be an authorized signatory (typically a director, partner, or someone holding a valid Power of Attorney).

Step 2: Create a Taxable Person profile

Within EmaraTax, create a new Taxable Person profile if one does not already exist. Enter your trade licence number, legal form (LLC, sole establishment, FZE, branch), and authorized signatory details. Each legal entity requires its own profile. Related companies cannot share a profile unless they are forming a tax group. If you are a natural person registering for CT, select the individual/natural person option and enter your Emirates ID details.

Step 3: Start the CT registration application

Go to the Taxable Person Account and click 'Register' under 'Corporate Tax.' The form will ask for your entity type (resident juridical person, non-resident juridical person, natural person), the date of incorporation or licence issuance, and the effective date of your first tax period. For most businesses, the first tax period starts on the later of June 1, 2023 (when CT took effect) or the date the entity was established.

Step 4: Complete the registration form

The form requires: entity details (legal name, trade name, licence number, date of incorporation), contact information (registered address, email, phone), financial year details (start and end month, first tax period dates), authorized representative details (name, Emirates ID, passport, role), banking details (UAE IBAN in the entity's name for any future refunds or credits), and business activity description (select from the FTA's activity codes). For free zone entities, the form also asks about qualifying income status and whether you intend to elect as a Qualifying Free Zone Person.

Step 5: Upload supporting documents

The FTA requires the following documents in PDF format (maximum 15 MB per file): a valid trade licence (must be current and active), Memorandum of Association or partnership agreement, passport copies of all owners, partners, or directors, Emirates ID of the authorized signatory, Power of Attorney or Board Resolution authorizing the person completing the registration (if not the owner), proof of business address (tenancy contract or Ejari), and bank account details (IBAN) for a UAE bank account in the entity's name. For branches of foreign companies, additional documents include the parent company's certificate of incorporation and the UAE branch licence.

Step 6: Submit and await TRN issuance

Review all fields, confirm the declaration (that the information is accurate and complete), and submit. EmaraTax generates a reference number. The FTA reviews within 5 to 15 business days. If additional information is needed, the FTA sends a query through EmaraTax notifications. Once approved, your 15-digit Corporate Tax TRN appears in the dashboard. This TRN is separate from your VAT TRN (if you have one): different registrations, different numbers, different returns.

Step 7: Post-registration setup

Once your CT TRN is issued, several things must happen. First, confirm your first tax period dates in EmaraTax and note the filing deadline (nine months from the end of the tax period, per our CT deadlines guide). Second, set up your accounting software to track income and expenses by CT-relevant categories (separating deductible from non-deductible expenses). Third, begin preparing your IFRS financial statements for the first tax period. Fourth, decide whether SBR applies (if revenue is under AED 3 million) or whether loss carry-forward planning is needed (if the first period is a loss year). Our CT return filing guide covers everything from this point forward.

Registration vs Filing: Two Separate Obligations That Most Businesses Confuse

Registration is the one-time process of enrolling your entity with the FTA and receiving a TRN. Filing is the annual submission of your CT return through that TRN. You cannot file without being registered. Being registered does not automatically file anything.

Registration creates the TRN. It tells the FTA your entity exists and is subject to CT. It sets the first tax period dates and establishes the annual filing cadence. Registration is a one-time event (unless the entity deregisters and re-registers).

Filing submits the annual return. Each year, within nine months of the tax period end, you submit the CT return through EmaraTax using your TRN. The return reports taxable income, deductions, reliefs, and the CT payable (if any). Filing happens every year for as long as the entity is registered. Our EmaraTax CT return walkthrough covers the filing process.

The confusion costs money. Many business owners assume that registering and filing are the same thing, or that you only need to register when you have tax to pay. Both assumptions are wrong. Registering late costs AED 10,000. Not filing after registration costs AED 500 per month for the first 12 months and AED 1,000 per month thereafter. Both penalties are separate and cumulative: a business that registered late and then filed late owes both.

Whether you need to register for the first time, claim the CTP006 waiver on a late registration, or prepare your first CT return, our team manages the entire compliance chain from registration through filing. Talk to us on WhatsApp.

CT Registration vs VAT Registration: Different Obligations, Different Thresholds

Our VAT registration guide covers the VAT side in full. The key differences:

CT registration is mandatory for all juridical persons regardless of revenue. An LLC earning AED 0 must register. VAT registration is mandatory only when taxable supplies exceed AED 375,000. Most new businesses register for CT months or years before they become VAT-registered.

Both use EmaraTax but generate separate TRNs. Your CT TRN and VAT TRN are different numbers. They appear on different returns. One does not substitute for the other. A business that has a VAT TRN is not automatically registered for CT (and vice versa).

The penalties are separate. Late CT registration: AED 10,000. Late VAT registration: AED 10,000. A business that is late on both owes AED 20,000. The registrations must be done independently through separate applications on EmaraTax.

Six Mistakes Businesses Make With CT Registration

1. Assuming registration is not needed because the business earns below AED 375,000. The AED 375,000 is the zero-rate band, not a registration threshold. All juridical persons must register. A dormant company with AED 0 revenue must register. The AED 10,000 penalty applies regardless of whether the business owes any tax.

2. Not registering because VAT registration is already done. CT and VAT are separate registrations. Having a VAT TRN does not mean you are CT-registered. Both must be completed independently.

3. Using the wrong licence date to calculate the deadline. If you hold multiple trade licences, the deadline is based on the licence with the earliest issuance date, not the most recent. A company with one licence issued in March and another issued in November uses the March date, which placed it in the March-April band with a June 30, 2024 deadline.

4. Missing the CTP006 waiver window by filing too late. The waiver requires filing your first CT return within seven months of the first tax period end. If you register in month six but need two months to prepare the return, you miss the seven-month window and lose the waiver. Register and start return preparation simultaneously.

5. Not registering a dormant or inactive company. A company that has ceased trading but has not been formally dissolved or deregistered from the commercial registry is still a juridical person. It must register for CT. It must file a nil return. Ignoring it does not make the obligation disappear. The AED 10,000 registration penalty and the AED 500/month filing penalty both apply to dormant entities.

6. Confusing the registration deadline with the filing deadline. Registration has its own deadline (staggered by licence month for pre-2024 entities, 3 months from incorporation for new entities). Filing has a different deadline (9 months from tax period end, or 7 months for CTP006 waiver). They are independent timelines. Our deadlines guide maps every critical date.

What to Do If You Are Already Late: The Action Plan

If your registration deadline has passed and you have not yet registered, here is the practical action plan.

Step 1: Check whether the CTP006 waiver window is still open. Calculate seven months from the end of your first tax period. If that date has not yet passed, the waiver is still available. If it has passed, the AED 10,000 penalty is not waivable and must be paid.

Step 2: Register immediately on EmaraTax. Do not wait. Every day of delay does not increase the registration penalty (it is a flat AED 10,000), but it reduces the time available to prepare and file your first return within the seven-month waiver window. Gather your documents, complete the form, and submit.

Step 3: Begin preparing your first CT return simultaneously. Do not wait for the TRN to be issued before starting return preparation. Gather your financial statements, organize your deductible and non-deductible expenses), and engage a tax advisor to prepare the return. The moment the TRN is issued, you should be ready to file within days, not weeks.

Step 4: File the return within the seven-month window. If you meet the deadline, the penalty is waived. If you miss it by even one day, the full AED 10,000 applies. Treat the seven-month date as a hard deadline.

Step 5: If the waiver window has passed, pay the penalty and move forward. The AED 10,000 is a sunk cost. Do not let it delay further compliance. Register, file your return (even if past the nine-month deadline, which carries its own late filing penalty), and bring your compliance current. Continued non-compliance compounds: AED 10,000 registration + AED 500-1,000 per month in late filing + 14% per annum interest on unpaid tax. As our penalty guide documents, the compounding effect of multiple missed deadlines is far more expensive than the initial AED 10,000.

Frequently Asked Questions

Do all UAE businesses need to register for corporate tax?

All juridical persons (LLCs, free zone entities, branches) must register regardless of revenue. Natural persons (freelancers, sole traders) must register only if business turnover exceeds AED 1 million per calendar year.

What is the penalty for late CT registration?

AED 10,000 per entity, applied as a flat administrative penalty under Cabinet Decision No. 10 of 2024. The penalty is assessed at the point of registration if the deadline has passed.

Can the AED 10,000 late registration penalty be waived?

Yes. Under Public Clarification CTP006 (effective April 14, 2025), the penalty is waived if you file your first corporate tax return within seven months (instead of nine) from the end of your first tax period. If already paid, the FTA credits or refunds it.

Is CT registration the same as VAT registration?

No. They are completely separate obligations with different thresholds, different TRNs, and different returns. CT registration is mandatory for all juridical persons regardless of revenue. VAT registration is mandatory only when taxable supplies exceed AED 375,000.

How long does CT registration take on EmaraTax?

The application takes 15-20 minutes. FTA review and TRN issuance typically takes 5 to 15 business days depending on document completeness.

What documents do I need for CT registration?

Valid trade licence, Memorandum of Association, passport copies of owners/directors, Emirates ID of the authorized signatory, Power of Attorney or Board Resolution, proof of address (tenancy/Ejari), and bank account details (UAE IBAN).

My company is dormant. Do I still need to register?

Yes. A dormant company that has not been formally dissolved is still a juridical person and must register for CT. It must also file nil returns. Non-compliance with a dormant entity attracts the same penalties as an active business.

What is the deadline for new companies incorporated in 2026?

Three months from the date of incorporation. A company incorporated on March 15, 2026 must register by June 15, 2026.

My company holds multiple trade licences. Which one determines my deadline?

The licence with the earliest issuance date. If you have licences issued in March and November, the March licence determines the deadline.

What happens after I receive my CT TRN?

You must file an annual CT return within nine months of your tax period end. Set up your accounting software, prepare IFRS financial statements, and decide on SBR or standard filing. Our CT return filing guide covers the process from this point.

Register Now. File Early. Save AED 10,000.

Corporate tax registration is not optional, not revenue-dependent, and not something that can wait until you 'start making money.' Every LLC, every free zone company, every branch, every sole establishment in the UAE is obligated to register. The deadlines have all passed for entities that existed before March 2024. New entities have three months from incorporation. The penalty for missing any of these deadlines is AED 10,000.

But the CTP006 waiver changes the calculation for businesses that act quickly. Register now, even if late. Prepare your first return immediately. File within seven months of your first tax period end. If you meet that window, the AED 10,000 is waived or refunded. If you miss it, the penalty stands. The difference between AED 10,000 and AED 0 is a matter of timing, not eligibility.

The registration takes 15 minutes. The return preparation takes longer. Start both today.

We register businesses for CT on EmaraTax, prepare the first return, and file within the CTP006 waiver window to eliminate the AED 10,000 penalty. For businesses already registered, we handle the annual CT return filing and ongoing compliance. Start on WhatsApp.