A restaurant in Business Bay crosses AED 375,000 in food sales. A freelance designer in Dubai Marina earns AED 200,000 and spends AED 190,000 on equipment. An Indian SaaS company sells a AED 50,000 software licence to a Dubai client. All three businesses face the same question: do I need to register for VAT? The answer is different for each of them, and the difference is not just about the number.

The restaurant must register. Its taxable supplies crossed the mandatory threshold. It has 30 days from the date the threshold was exceeded to submit a registration application on EmaraTax. Missing the deadline triggers an AED 10,000 penalty plus retroactive VAT liability on every taxable sale made since the threshold was crossed. The designer can register voluntarily (her taxable expenses exceed AED 187,500, even though her revenue does not reach AED 375,000), but whether she should depends on a cost-benefit calculation that most articles about VAT registration never run. The Indian SaaS company must register as a non-resident supplier making taxable supplies in the UAE, regardless of amount, unless the UAE buyer accounts for the VAT through the reverse charge mechanism.

This is the guide to getting VAT registration right from the start. When registration is mandatory, when it is optional, when it is not yet available, the exact EmaraTax process with field-level detail, the documents the FTA requires (and the ones that get applications rejected), the voluntary registration cost-benefit math with AED examples, and the five procedural mistakes that cause delays, rejections, or penalties. Once you are registered, our quarterly VAT return guide covers how to file. This article covers everything that comes before that first return.

"VAT registration is the first compliance decision most UAE businesses make, and many get it wrong before they even start. Some register too late and pay the AED 10,000 penalty. Some register too early when they are not eligible and the FTA rejects the application. Some register voluntarily without understanding the quarterly filing obligation it creates. The registration itself takes 20 minutes on EmaraTax. The decision of whether and when to register takes much longer and matters much more."

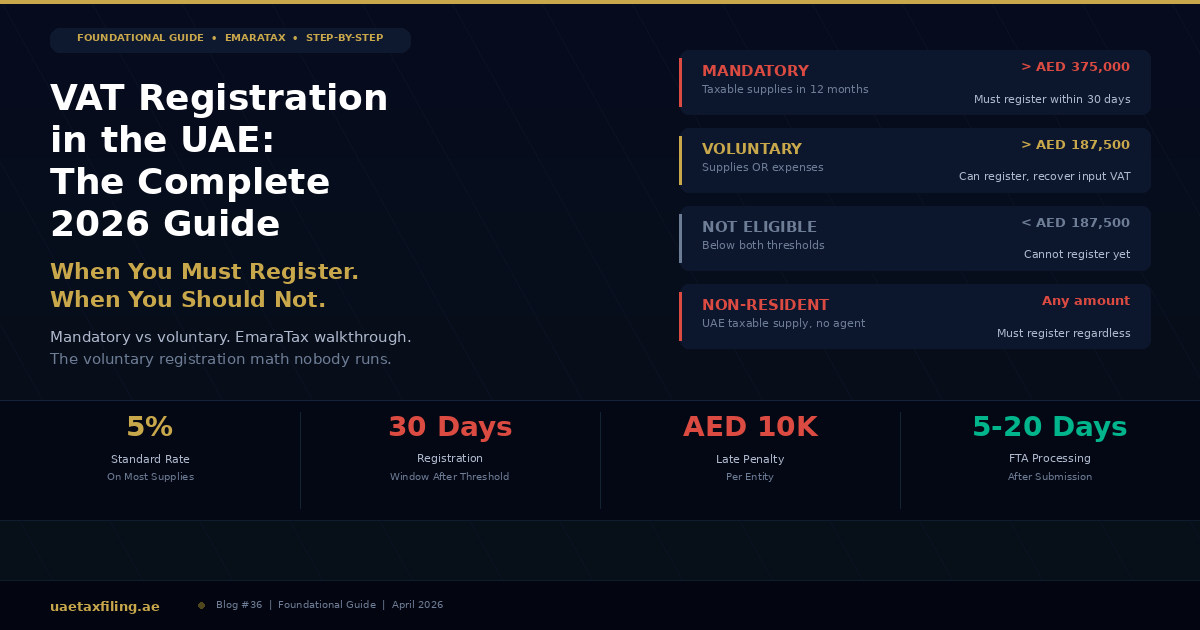

Mandatory Registration: The AED 375,000 Threshold

Under Federal Decree-Law No. 8 of 2017 (as amended by Federal Decree-Law No. 16 of 2025), VAT registration is mandatory when the total value of a business's taxable supplies and imports exceeds AED 375,000. As the UAE Government's official VAT portal and the FTA's registration page both confirm, there are two tests for crossing the threshold, and either one is sufficient to trigger the obligation.

Test 1: The backward-looking test. If the total value of your taxable supplies and imports exceeded AED 375,000 over the previous 12 calendar months (a rolling period, not a financial year), you must register. The 12-month window moves forward every month. If your cumulative supplies for the period April 2025 to March 2026 cross AED 375,000, you are obligated to register as of the date the threshold was exceeded. You have 30 days from that date to submit the registration application.

Test 2: The forward-looking test. If you anticipate that your taxable supplies and imports will exceed AED 375,000 within the next 30 days, you must register immediately. This test catches businesses that sign a large contract (for example, a single AED 400,000 project) that will push them over the threshold before the 12-month rolling period catches up. The forward-looking test is based on reasonable expectation: signed contracts, confirmed purchase orders, or demonstrable order patterns.

What counts toward the threshold. Taxable supplies at the standard 5% rate count. Zero-rated supplies (exports, healthcare, education, first supply of residential property) also count because they are still 'taxable supplies,' just at 0%. Exempt supplies (certain financial services, bare land, local passenger transport) do NOT count. Import of goods subject to VAT also counts. A business with AED 300,000 in standard-rated domestic sales and AED 100,000 in zero-rated exports has AED 400,000 in taxable supplies and must register.

The 30-day registration window. Once either test is triggered, the business has 30 calendar days to submit the registration application through EmaraTax. The 30 days begin from the date the threshold was exceeded (backward test) or the date the business became aware it would be exceeded (forward test). As UAE Expert Hub's 2026 guide documented, missing the 30-day window triggers the AED 10,000 late registration penalty, which the FTA enforces consistently.

Retroactive liability. Late registration does not just cost the penalty. The FTA expects the business to account for VAT on every taxable supply made since the date it should have been registered. If a business should have registered on January 1 but registers on April 1, it owes 5% VAT on all taxable supplies from January through March, even though it never charged VAT to its customers during that period. The business absorbs this cost from its own margin. This retroactive exposure can be significantly larger than the AED 10,000 penalty itself.

Voluntary Registration: The AED 187,500 Threshold and When It Makes Sense

Businesses that have not crossed the mandatory AED 375,000 threshold may still register voluntarily if their taxable supplies, imports, or taxable expenses exceed AED 187,500 in the previous 12 months or are expected to exceed that amount in the next 30 days. As the FTA's official guidance confirms, voluntary registration is based on either taxable supplies or taxable expenses, meaning a business with high expenses but low revenue can still qualify.

Why voluntary registration exists. The primary benefit is input VAT recovery. A business that is not VAT-registered cannot claim back the 5% VAT it pays on business expenses. A registered business can. For startups with significant setup costs (fit-out, equipment, professional fees, marketing) but limited initial revenue, voluntary registration allows recovery of the VAT on those costs. The recovered VAT improves cash flow during the critical early months when every dirham matters.

The voluntary registration cost-benefit math

This is the analysis that most articles about VAT registration skip entirely. Voluntary registration is not free. It creates ongoing obligations: quarterly VAT return filing, record-keeping requirements, VAT-compliant invoicing, and the administrative time or accountant cost associated with each. The question is whether the input VAT recovered exceeds the compliance cost.

Scenario A: Startup with high setup costs. A new café investing AED 400,000 in fit-out, kitchen equipment, and furniture before opening. VAT on those expenses: AED 20,000 (5% of AED 400,000). First-year ongoing expenses (rent, supplies, utilities, marketing) estimated at AED 240,000, with VAT of AED 12,000. Total recoverable input VAT in year one: AED 32,000. Compliance cost: quarterly filing at approximately AED 1,500-2,000 per quarter through an accounting service = AED 6,000-8,000 per year. Net benefit: AED 24,000-26,000. Voluntary registration is clearly worth it.

Scenario B: Freelance consultant with low expenses. A management consultant earning AED 250,000 per year with minimal expenses: co-working space AED 18,000, laptop AED 5,000, software AED 3,000, phone AED 2,000. Total VAT-bearing expenses: AED 28,000. Recoverable input VAT: AED 1,400 (5% of AED 28,000). Compliance cost: quarterly filing at AED 1,500-2,000 per quarter = AED 6,000-8,000 per year. Net cost: AED (4,600) to AED (6,600). Voluntary registration costs more than it recovers. The consultant should wait until revenue crosses AED 375,000 and mandatory registration kicks in.

Scenario C: E-commerce importer in setup phase. A new Amazon seller importing AED 300,000 in inventory before listing. Import VAT: AED 15,000 (paid at customs). First shipment of goods: AED 200,000 additional inventory, VAT AED 10,000. Total recoverable in the first 6 months: AED 25,000. Compliance cost: AED 3,000-4,000 for two quarterly returns. Net benefit: AED 21,000-22,000. As our e-commerce VAT guide covers, marketplace sellers should register early when they import significant inventory because the input VAT on imported goods is substantial.

The decision rule. If your annual VAT-bearing business expenses exceed approximately AED 120,000-160,000, the input VAT recovery (AED 6,000-8,000) exceeds the typical compliance cost (AED 6,000-8,000). Above that expense level, voluntary registration makes financial sense. Below it, the compliance cost exceeds the recovery, and you should wait for mandatory registration.

Not sure whether voluntary registration makes sense for your business? Our VAT team runs the cost-benefit calculation using your actual expense profile and advises on the timing that maximizes your input VAT recovery. Message us on WhatsApp.

Who Cannot Register (Yet)

If your taxable supplies, imports, and taxable expenses are all below AED 187,500, you are not eligible for VAT registration. The FTA will reject your application. You cannot register preemptively in anticipation of future growth unless you have documented evidence (signed contracts, purchase orders) that the threshold will be exceeded within 30 days.

This matters for very early-stage startups that have incorporated but not yet begun trading. A company with a trade licence but zero revenue and zero expenses cannot register for VAT. It must wait until either expenses or anticipated supplies cross AED 187,500. Our startup CT guide covers the registration sequence: typically CT registration comes first (mandatory for all juridical persons regardless of revenue), followed by VAT registration once the threshold is met.

Non-Resident Businesses: Registration Without a Threshold

The AED 375,000 mandatory threshold does not apply to non-resident businesses. As the FTA confirms, non-resident businesses that make taxable supplies in the UAE must register for VAT regardless of the value of those supplies, unless there is another person in the UAE responsible for settling the VAT on those supplies (the reverse charge mechanism).

In practice, this means: a foreign company selling goods delivered to the UAE (imported by the UAE buyer) does not need to register if the buyer handles import VAT. A foreign company providing services to a UAE business does not need to register if the UAE business accounts for VAT under reverse charge. But a foreign company that sells directly to UAE consumers (B2C), operates a fixed establishment in the UAE, or provides services where no reverse charge applies must register from the first dirham of UAE taxable supply.

The EmaraTax Registration Process: Step by Step

All VAT registration is handled through the FTA's EmaraTax portal. There is no offline or paper-based alternative. The process takes approximately 20-30 minutes to complete if you have all documents prepared in advance. The FTA typically reviews and approves applications within 5 to 20 business days.

Step 1: Create your EmaraTax account

Go to EmaraTax on the FTA website and create a user account. You will need an email address and a UAE mobile number for two-factor authentication. If you previously had an FTA e-Services account (the old portal), your credentials were migrated to EmaraTax, but you may need to reset your password on first login. The FTA recommends linking your EmaraTax account to UAEPass for faster identity verification on subsequent logins.

Step 2: Create a Taxable Person profile

Within EmaraTax, create a new Taxable Person profile for your business entity. You will need your trade licence number, legal form (sole proprietor, LLC, partnership, branch of foreign company), and the authorized signatory's details (passport, Emirates ID). Each legal entity requires a separate profile. Related companies cannot share a single profile unless they form a VAT group.

Step 3: Start the VAT registration application

Click 'View' to access the Taxable Person Account, then click 'Register' under 'Value Added Tax.' Select the registration type: mandatory (you have exceeded AED 375,000), voluntary (you exceed AED 187,500 in supplies or expenses), or non-resident (you make UAE taxable supplies from outside the UAE).

Step 4: Complete the registration form

The form requires: business details (legal name, trade name, licence number, date of incorporation), contact information (address, email, phone), financial information (expected annual turnover, date the threshold was exceeded or is expected to be exceeded), banking details (UAE IBAN in the entity's name for future refunds), customs registration number (if the business imports goods), and declaration of any other business activities or related entities in the UAE.

Step 5: Upload supporting documents

The FTA requires the following documents in PDF or DOC format (maximum 15 MB per file): a valid trade licence (must be current, not expired), Memorandum of Association or partnership agreement, passport copies of all owners/partners, Emirates ID of the authorized signatory, proof of the threshold being met (at least five VAT invoices showing expenses exceeding the threshold, or purchase orders and contracts showing expected revenue), bank letter confirming account details (optional but recommended, the account must be in the entity's name for companies), and customs information if the business imports goods. As Fastlane's 2026 registration guide documents, document preparation is the step that determines whether the application is approved in 5 days or delayed for weeks.

Step 6: Submit and await TRN issuance

Review all fields and documents, then submit. EmaraTax generates a reference number for tracking. The FTA reviews within 5 to 20 business days. If the FTA needs additional information, they send a query through EmaraTax (check your notifications regularly during this period). Once approved, your 15-digit Tax Registration Number (TRN) appears in your EmaraTax dashboard. Download your VAT registration certificate (the FTA charges AED 250 for a printed certificate if you need a physical copy).

Step 7: Post-registration setup

Once registered, four things must happen immediately. First, configure your accounting software with the correct 5% VAT tax codes and your TRN. Second, update all invoice templates to include your TRN, the correct VAT rate, and the VAT amount on every line item (Article 65 compliance). Third, confirm your first VAT return period with the FTA (the period is assigned automatically, typically quarterly). Fourth, start tracking input VAT on all business purchases from the registration effective date. Our quarterly VAT return guide covers everything from this point forward.

We handle the entire registration process for clients: document preparation, EmaraTax submission, FTA query responses, and post-registration software setup. Registration typically completes in 5-10 business days when we submit. Talk to us on WhatsApp.

VAT Registration vs CT Registration: Two Separate Obligations

Many business owners confuse VAT registration with corporate tax registration. They are completely separate obligations with different thresholds, different triggers, and different consequences. Both are done through EmaraTax, but they are independent applications.

VAT registration is based on taxable supplies exceeding AED 375,000 (mandatory) or AED 187,500 (voluntary). It applies to any business regardless of legal form. Once registered, you file quarterly VAT returns and charge 5% VAT on taxable supplies. Not every business needs to register for VAT (only those above the threshold).

CT registration is mandatory for all juridical persons (LLCs, free zone entities, branches of foreign companies) regardless of revenue. Natural persons (sole proprietors, freelancers) must register only if business turnover exceeds AED 1 million. CT registration does not require you to charge anything to customers. It creates an annual filing obligation for the corporate tax return. Our influencer CT guide covers the natural person threshold in detail.

The timing sequence for a new business. A new Dubai LLC must register for CT immediately upon incorporation (regardless of revenue). It must register for VAT only once taxable supplies cross AED 375,000. Many businesses are CT-registered for months or years before they become VAT-registered, because the CT threshold is zero (all entities must register) while the VAT threshold requires AED 375,000 in taxable activity. Our 2026 tax changes guide covers both registration frameworks in the broader compliance context.

What Happens After You Register: The Ongoing Obligations

Quarterly VAT return filing (Form VAT 201). Most businesses file quarterly (some high-turnover entities file monthly if directed by the FTA). The return is due by the 28th of the month following the end of the tax period. For Q1 2026 (January to March), the return is due by April 28, 2026. Our VAT return filing guide walks through the entire process.

VAT-compliant invoicing. Every tax invoice must include: supplier name and TRN, buyer name and TRN (for B2B supplies over AED 10,000), sequential invoice number, date of supply, description of goods or services, quantity, unit price, VAT rate and amount, and total amount including VAT. Non-compliant invoices prevent the buyer from claiming input VAT, which damages your business relationships. The upcoming e-invoicing mandate will make this even more critical from 2027.

Record-keeping for five years. All records supporting VAT calculations (invoices, credit notes, import declarations, expense receipts, bank statements, contracts) must be retained for at least five years. Real property records must be kept for seven years. The FTA can request an audit file at any time, and incomplete records result in penalties and unfavorable audit assessments.

Input VAT recovery. Once registered, you can recover the 5% VAT you pay on business expenses by deducting it as input VAT on your quarterly return. If input VAT exceeds output VAT (common for exporters and businesses in setup phase), the excess creates a credit balance that can be refunded through VAT 311 or carried forward against future output VAT. The new 5-year limitation on VAT credit expiration means you must claim refunds within five years or lose the credit permanently.

Deregistration if circumstances change. If your taxable supplies drop below AED 187,500 for a consecutive 12-month period, you must apply for deregistration within 20 business days. Failure to deregister when required triggers its own penalty. Deregistration requires filing a final VAT return and accounting for 'deemed supply' VAT on any assets for which input VAT was previously claimed (you effectively repay the input VAT on assets you retain after deregistration).

Five Mistakes That Get VAT Registration Applications Rejected or Delayed

1. Applying without sufficient proof of the threshold. The FTA requires at least five VAT invoices or contracts proving that the threshold was crossed or will be crossed. Many businesses apply with only 2-3 invoices and the application is returned for additional documentation. For voluntary registration based on expenses, the five invoices must show taxable expenses, not revenue. Gather documentation before starting the application.

2. Submitting an expired trade licence. The trade licence attached to the application must be valid and current. An expired licence is the most common reason for instant rejection. If your licence is due for renewal, renew it first, then apply for VAT registration.

3. Bank account mismatch. The UAE IBAN provided must be in the name of the legal entity (for companies) or in the personal/sole establishment name (for individuals). If the bank account name does not match the entity name on the trade licence, the FTA will query the application. This is a common problem for businesses that have recently changed their legal name or for sole proprietors using a personal account with a different name format.

4. Not disclosing related entities. The registration form asks whether the applicant has other business interests in the UAE. Failing to disclose related companies, partner entities, or other trade licences held by the same owner creates a compliance issue that the FTA's cross-referencing systems will catch. If you own multiple businesses, disclose all of them. The FTA may determine that two related entities should form a VAT group rather than registering separately.

5. Registering when not yet eligible. Businesses below the AED 187,500 voluntary threshold cannot register. Submitting an application with supplies and expenses both below AED 187,500 will be rejected. Some business owners apply early 'to be safe,' but the FTA does not accept preemptive applications without evidence of the threshold being met or about to be met. Wait until you have documentation showing the threshold is crossed or imminent.

The Penalty Framework for Registration Failures

Our penalty regime guide covers the full VAT penalty framework. For registration specifically:

Late registration: AED 10,000. Applied per entity that fails to register within 30 days of crossing the mandatory threshold. This is a fixed penalty, not a percentage. It applies regardless of whether the business has since registered. The penalty is assessed retroactively once the FTA identifies the late registration, which can happen during a routine FTA audit or through cross-referencing of customs import data against VAT registration records.

Retroactive VAT liability. In addition to the penalty, the business must account for 5% VAT on all taxable supplies made from the date it should have been registered until the actual registration date. This retroactive liability is the business's cost, not the customer's, because the business never charged VAT during the unregistered period. A business that should have registered in January but registered in July owes 5% of six months of taxable supplies. On AED 500,000 in sales during that period, the retroactive liability is AED 25,000, paid from the business's own funds.

Late filing after registration: AED 1,000 first offense, AED 2,000 repeat within 24 months. Once registered, the quarterly return filing obligation begins immediately. Missing the filing deadline (28th of the month following the quarter end) triggers the late filing penalty. As of April 2026, late payment penalties shift to 14% per annum calculated monthly, replacing the previous compounding model.

Errors on filed returns. Errors with a VAT impact under AED 10,000 can be corrected on the next quarterly return. Errors exceeding AED 10,000 require a voluntary disclosure through EmaraTax within 20 business days of discovery. Failing to self-correct leads to significantly higher penalties if the FTA discovers the error first.

Frequently Asked Questions

When must I register for VAT in the UAE?

When your taxable supplies and imports exceed AED 375,000 over the previous 12 months, or when you expect them to exceed that amount within the next 30 days. You have 30 days from the trigger date to submit your application.

Can I register voluntarily before reaching AED 375,000?

Yes, if your taxable supplies, imports, or taxable expenses exceed AED 187,500. Voluntary registration allows you to recover input VAT on business expenses, but creates quarterly filing obligations.

How long does VAT registration take on EmaraTax?

The online application takes 20-30 minutes. FTA review and TRN issuance typically takes 5 to 20 business days, depending on completeness and FTA workload.

What documents do I need?

Valid trade licence, Memorandum of Association, passport copies of owners, Emirates ID, at least 5 VAT invoices or contracts proving the threshold, bank letter with IBAN details, and customs registration if you import goods. All in PDF or DOC, max 15 MB each.

What is the penalty for late VAT registration?

AED 10,000 fixed penalty per entity, plus retroactive VAT liability on all taxable supplies made during the unregistered period.

Is VAT registration the same as corporate tax registration?

No. They are separate obligations with different thresholds. CT registration is mandatory for all juridical persons regardless of revenue. VAT registration is mandatory only when taxable supplies exceed AED 375,000.

Do free zone companies need to register for VAT?

Yes, if their taxable supplies exceed the threshold. Free zone companies benefit from zero-rated treatment on certain transfers within and between designated zones, but must still register and file returns.

Should I register voluntarily as a startup?

Only if your VAT-bearing business expenses exceed approximately AED 120,000-160,000 per year. Below that level, the input VAT recovery (approximately AED 6,000-8,000) does not justify the compliance cost.

What is a TRN?

A Tax Registration Number, a unique 15-digit identifier issued by the FTA upon VAT registration. It must appear on all invoices, returns, and FTA correspondence.

Can I deregister from VAT if my business shrinks?

Yes. If taxable supplies fall below AED 187,500 for 12 consecutive months, you must apply for deregistration within 20 business days. A final return and deemed supply calculation are required.

Register Once, Register Right

VAT registration is a one-time process that creates a permanent compliance framework for your business. Get it right from the start, and the quarterly returns, input VAT recovery, and FTA Audit File generation all follow a clean path. Get it wrong, and you spend the first year correcting retroactive liabilities, fixing rejected applications, and rebuilding records that should have been maintained from day one.

The mandatory threshold is AED 375,000. The voluntary threshold is AED 187,500. The late registration penalty is AED 10,000 plus retroactive VAT. The FTA processing time is 5-20 business days. The application takes 20 minutes if your documents are prepared. The voluntary registration decision depends on a cost-benefit calculation that is specific to your expense profile, not on a generic recommendation.

Know your numbers. Check your rolling 12-month total monthly. Have your documents ready before the threshold hits. Register within the 30-day window. Set up your accounting software and invoicing on day one. Then file your first VAT return on time and start building the clean compliance record that keeps the FTA satisfied and your business running without friction.

From threshold assessment to EmaraTax submission to post-registration software setup, we handle the entire VAT registration process. Your TRN is issued, your invoicing is compliant, and your first return is filed correctly. Start on WhatsApp.