A startup spent AED 800,000 in its first year and earned AED 400,000. Net loss: AED 400,000. CT payable: AED 0. Most owners stop thinking about tax at that point. Zero tax, nothing to pay, nothing to worry about. But that AED 400,000 loss is not nothing. Under the UAE CT law, it is a deferred tax asset. It can be carried forward to the next year, and the year after that, and every year after that, indefinitely, until it is used up. When the business becomes profitable, the carried-forward loss offsets the profit, and the CT bill shrinks by up to AED 36,000.

Unless the owner ticked the wrong box on the CT return. If they elected Small Business Relief in the loss year, the loss is destroyed. SBR treats taxable income as zero. A loss is negative taxable income. Treating it as zero means the loss does not exist for CT purposes. It cannot be carried forward. The future AED 36,000 saving disappears permanently. The SBR election saved AED 0 in the loss year (because CT was already AED 0 on a loss) and cost AED 36,000 in future years. One checkbox. AED 36,000.

This is the most expensive mistake in UAE corporate tax that almost nobody talks about. This article covers the mechanics of tax loss carry-forward under Articles 37, 38, and 39 of the CT Law, the 75% utilization cap, the 50% ownership continuity test, the group loss transfer rules, and the SBR trap that turns a bad year into a permanently worse outcome. Our how much does CT actually cost article showed the effective rate for most businesses is 0% to 4%. This article shows how losses from unprofitable periods reduce that rate even further, if you handle them correctly.

"Every startup founder and new business owner who comes to us after a loss year asks the same question: do I need to file a CT return if I made a loss? The answer is yes. Not because you owe tax, but because the return is what creates the loss record. If you do not file, or if you elect SBR without understanding the consequences, the loss disappears from the system. You cannot get it back. Filing correctly in a loss year is worth more than filing correctly in a profitable year, because the loss year creates the asset that reduces the profitable year."

Jazim, CEO, UAE Tax Filing LLC

How Tax Loss Carry-Forward Works Under the UAE CT Law

Article 37 of the UAE Corporate Tax Law (Federal Decree-Law No. 47 of 2022) establishes the basic rule: a taxable person can offset a tax loss incurred in one period against the taxable income of subsequent periods. As PwC's deductions summary documents, the offset is subject to a 75% cap per period, and any unused remainder carries forward indefinitely to further subsequent periods. There is no time limit on how long a loss can be carried forward. A loss from 2024 can be used in 2030, 2035, or 2045, as long as the ownership and business continuity conditions are met.

The sequence matters. When you have a carried-forward loss and current-year taxable income, the loss must be applied before it can roll to the next year. You cannot choose to skip a year and save the loss for later. If your business earns AED 200,000 in taxable income and you have AED 300,000 in carried-forward losses, you must offset 75% of AED 200,000 (= AED 150,000) from the loss, reducing your taxable income to AED 50,000. The remaining AED 150,000 of the loss rolls forward to the next period. You cannot voluntarily decline to use the loss in the current year.

Losses that cannot be carried forward. Three categories of losses are excluded. First, losses incurred before the effective date of UAE CT (before your first CT tax period, which started on or after June 1, 2023). A company that lost money in the financial year ending December 31, 2022 cannot carry that loss into the CT regime. Second, losses incurred before a person became a taxable person. As Flying Colour Tax's analysis explains, a natural person who had business turnover below AED 1 million (and therefore was not a taxable person) cannot carry forward losses from those pre-registration years. Third, losses from exempt income or qualifying free zone income cannot be carried forward against regular taxable income. A QFZP that earns qualifying income at 0% cannot generate a loss from that income stream that offsets non-qualifying income.

The 75% Utilization Cap: You Always Pay Some CT

The most important mechanical rule: in any given tax period, you can only offset up to 75% of that period's taxable income using carried-forward losses. The remaining 25% is always taxable at 9%, regardless of how much loss you have accumulated. As Crowe UAE's loss provisions analysis confirms, this cap ensures that profitable businesses always pay some CT, even if they have large prior-year losses.

Worked example: Your company had a loss of AED 500,000 in Year 1. In Year 2, the company earns AED 800,000 in taxable income (after all deductions). You can offset 75% of AED 800,000 = AED 600,000 from the carried-forward loss. But you only have AED 500,000 in losses, so you use the full AED 500,000. Taxable income after loss offset: AED 300,000. Less AED 375,000 zero-rate band: AED 0 taxable. CT = AED 0. The entire AED 500,000 loss was consumed, and the AED 375,000 band reduced the remaining income to zero. In this scenario, the loss saved AED 45,000 in CT (9% of AED 500,000).

Large loss example: Your company had a loss of AED 2,000,000 in Year 1 (a major capital investment year). In Year 2, taxable income is AED 1,800,000. You can offset 75% = AED 1,350,000 from the loss. Taxable income after offset: AED 450,000. Less AED 375,000 band: AED 75,000 taxable at 9% = AED 6,750 CT payable. Remaining loss carried to Year 3: AED 650,000 (AED 2M minus AED 1.35M). Even with AED 2 million in losses, the company still pays AED 6,750 in CT because of the 75% cap. As WellTax's analysis noted, despite the clear benefits, many businesses fail to fully use their losses because they do not understand the cap mechanics or do not maintain proper records of the loss balance.

The SBR Destroyer: The Most Expensive Checkbox Mistake in UAE Corporate Tax

This is the section that could save you AED 36,000 or more. Read it carefully.

Small Business Relief (covered in depth in our SBR guide) is available to businesses with revenue below AED 3 million. When elected, SBR treats taxable income as zero. No CT payable. No complex return. It sounds like an obvious choice for any qualifying business, and for profitable businesses, it usually is. But for businesses that made a loss, SBR is a trap.

The mechanics of the trap. When SBR treats taxable income as zero, it does not distinguish between positive and negative taxable income. A profit of AED 200,000 becomes zero (good, you saved CT). A loss of AED 400,000 also becomes zero (bad, you lost the loss). The loss is not recognized. It is not recorded on the return as a carried-forward asset. It simply does not exist in the CT system. Once the SBR election is made and the return is filed, the loss is gone permanently. There is no mechanism to go back and undo the election to recover the loss.

The AED math of the mistake: A consulting firm with AED 2.5 million revenue had a loss of AED 400,000 in 2024 (heavy investment in staff, office setup, marketing before revenue fully materialized). The owner's accountant elected SBR because revenue was under AED 3 million and 'it is simpler.' CT in 2024: AED 0 (it would have been AED 0 anyway, because you cannot owe CT on a loss). SBR saved: AED 0. In 2025, the business becomes profitable with AED 600,000 in taxable income. Without SBR in 2024, the firm could offset AED 400,000 of the loss against AED 600,000 (capped at 75% = AED 450,000, so the full AED 400,000 is used). Taxable income drops to AED 200,000, below the AED 375,000 band. CT = AED 0. With SBR in 2024, the loss is gone. Taxable income in 2025: AED 600,000. Less AED 375,000 band: AED 225,000 at 9% = AED 20,250 CT payable. The SBR election in 2024 cost AED 20,250 in 2025. If the firm remains profitable at similar levels in 2026, the total cost of the 2024 SBR election rises to AED 36,000 or more over two years. One checkbox. AED 36,000.

When SBR is still the right choice in a loss year. If the loss is tiny (under AED 50,000) and the simplification benefit of SBR outweighs the future saving (9% of AED 50,000 = AED 4,500 maximum), SBR may be reasonable. If the business is closing and will never be profitable again, carrying forward the loss has no value. If the business has revenue well under AED 1 million and the owner's time spent on a full CT return exceeds the value of the loss, SBR is defensible. But for any business with a meaningful loss (AED 100,000+) and a reasonable expectation of future profitability, SBR in a loss year is almost never worth it.

The SBR decision in a loss year requires forward-looking analysis, not a default checkbox. Our corporate tax team models the multi-year impact of electing or not electing SBR based on your actual loss amount and projected future profitability. The answer takes 30 minutes to calculate and can save AED 20,000 to AED 100,000. Message us on WhatsApp.

The 50% Ownership Continuity Test: What Happens When You Sell the Business

Tax losses belong to the entity, not the owner. But the right to use those losses depends on who owns the entity. Article 39 of the CT Law establishes two conditions for loss carry-forward, and both must be met.

Condition 1: 50% ownership continuity. The same person or persons must continuously own at least 50% of the shares (or ownership interest) from the beginning of the tax period in which the loss was incurred to the end of the tax period in which the loss is used. If ownership drops below 50%, the loss may be forfeited. As Chambers & Partners' UAE practice guide confirms, losses can be carried forward indefinitely provided that at least 50% ownership continuity is maintained.

Condition 2: Business continuity (the safety net). If ownership does change by more than 50%, the losses can still be preserved if the business continues to operate the same or a similar business activity. A company that was a consulting firm when the loss was incurred, and remains a consulting firm after the ownership change, can still carry forward the loss. A company that was a consulting firm and is now a furniture trading business after the ownership change cannot. The activity must remain substantially similar.

Practical scenario: partial sale. Mr. A owns 100% of Company X. Company X has AED 300,000 in carried-forward losses. Mr. A sells 40% of Company X to an investor. Ownership continuity: Mr. A still holds 60%, which exceeds the 50% threshold. The losses are fully preserved. If Mr. A sells 60% instead (retaining only 40%), the 50% threshold is breached. The losses survive only if Company X continues the same or a similar business.

The stock exchange exception. Companies listed on a recognized stock exchange are exempt from both the ownership continuity and business continuity tests. Share trading on public markets does not affect loss carry-forward for listed entities. This exemption exists because public company ownership changes continuously through market trading, and imposing a 50% continuity test would be impractical.

Planning for a future sale. If you know you may sell the business in the next few years, the loss carry-forward planning is critical. Use the losses as quickly as possible before the sale (by ensuring the business generates enough taxable income to absorb the losses within the 75% cap). If the sale will exceed the 50% threshold, ensure the buyer commits contractually to continuing the same business activity. Document the business continuity requirement in the sale agreement. Without this, the buyer may restructure the business and forfeit the losses that were factored into the acquisition valuation. Our transfer pricing guide covers the broader implications of ownership changes on intercompany transactions.

Group Loss Transfer: Moving Losses Between Related Companies

Article 38 of the CT Law allows a taxable person to transfer its tax losses to another taxable person within the same corporate group. This is powerful: a loss-making subsidiary can transfer its losses to a profitable parent (or sibling), reducing the group's total CT bill. As Crowe UAE's provisions guide documents, the transfer is subject to specific conditions.

The conditions for group loss transfer. First, one entity must hold at least 75% direct or indirect ownership in the other, or a third entity must hold at least 75% in both. Second, both entities must be UAE tax-resident juridical persons. Third, both must have the same financial year and use the same accounting standards (typically IFRS). Fourth, neither can be an exempt person or a Qualifying Free Zone Person. Our tax group formation guide covers the broader group structuring considerations, including when to form a formal tax group versus using standalone group loss transfers.

Worked example: ParentCo (UAE mainland LLC) owns 100% of SubCo (UAE mainland LLC). ParentCo earned AED 1,200,000 in taxable income. SubCo incurred a loss of AED 400,000 (it is a new venture still in early stage). Both have December 31 financial year-end, both use IFRS. SubCo can transfer AED 400,000 of its loss to ParentCo. ParentCo's taxable income reduces to AED 800,000. Less AED 375,000 band: AED 425,000 taxable at 9% = AED 38,250. Without the transfer, ParentCo would pay 9% on AED 825,000 (AED 1.2M minus AED 375K) = AED 74,250. The group loss transfer saved AED 36,000 (AED 74,250 minus AED 38,250). SubCo's loss is consumed by the transfer and is no longer available for carry-forward in SubCo.

The 75% cap still applies. The transferred loss is subject to the same 75% utilization cap in the receiving entity. If ParentCo's taxable income is AED 500,000 and SubCo transfers AED 500,000 in losses, ParentCo can only use 75% of AED 500,000 = AED 375,000 from the loss. The remaining AED 125,000 does not roll back to SubCo; it is lost. This means that group loss transfers should be sized carefully to match the receiving entity's capacity to absorb them within the 75% cap. Over-transferring wastes losses.

Group loss transfers require precise sizing, proper documentation, and coordinated filing across both entities. Our accounting team manages the calculation, prepares the transfer election on both CT returns, and ensures the group structure meets all four conditions. Talk to us on WhatsApp.

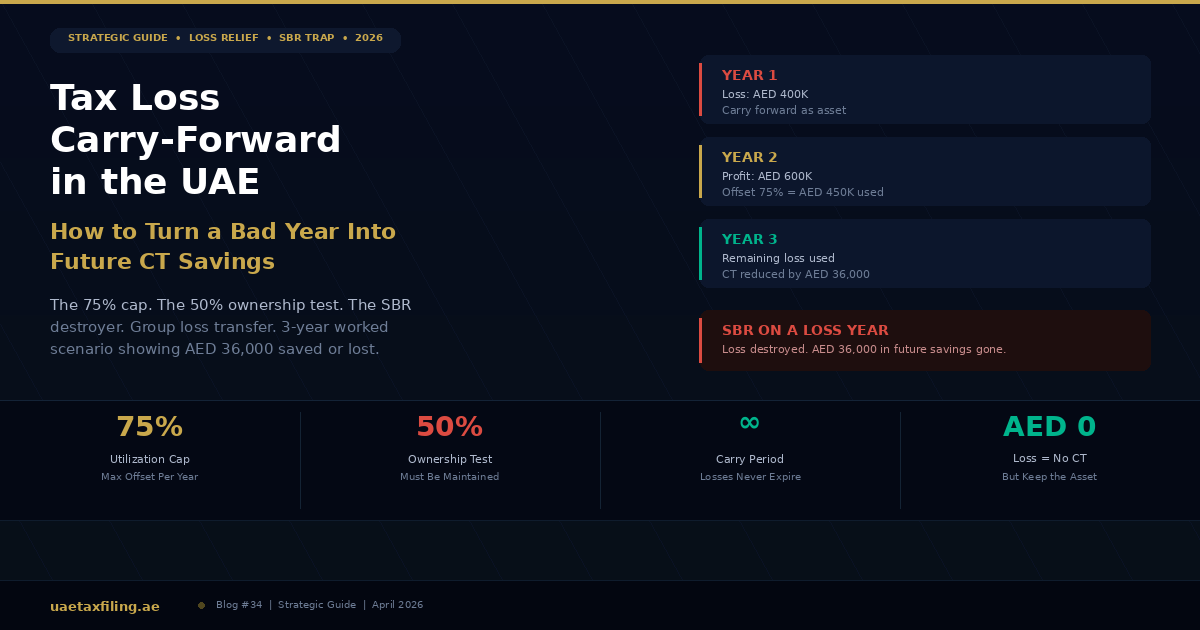

The Full 3-Year Scenario: AED 400,000 Loss Into AED 36,000 Saved

A technology startup, incorporated January 2024. Calendar-year financial period. Let us walk through three years of CT treatment.

Year 1 (2024): The loss year

Revenue: AED 400,000 from early clients. Expenses: AED 800,000 (founder salaries AED 480,000, office AED 60,000, software development AED 120,000, marketing AED 80,000, legal and licensing AED 35,000, other AED 25,000). Net loss: AED (400,000). Our startup CT guide covers first-year registration and filing obligations.

CT return treatment (NO SBR elected): Loss of AED 400,000 recorded on the CT return. CT payable: AED 0. Loss carried forward to Year 2: AED 400,000. This is a deferred tax asset worth up to AED 36,000 (9% of AED 400K) in future CT savings.

If SBR had been elected: Taxable income treated as AED 0. Loss not recognized. Carried-forward balance: AED 0. Future saving destroyed: up to AED 36,000. SBR saved: AED 0 (CT was already zero on a loss). Net impact of the wrong choice: negative AED 36,000.

Year 2 (2025): First profitable year

Revenue: AED 1,200,000. Expenses: AED 600,000. Taxable income before loss offset: AED 600,000. Carried-forward loss available: AED 400,000.

Loss offset calculation: 75% of AED 600,000 = AED 450,000 maximum offset. Loss available: AED 400,000. Full AED 400,000 is offset (below the 75% cap). Taxable income after offset: AED 200,000. Less AED 375,000 zero-rate band: AED 0 taxable. CT payable: AED 0. Carried-forward loss remaining: AED 0 (fully used). Without the loss, CT would have been 9% of (AED 600,000 minus AED 375,000) = 9% of AED 225,000 = AED 20,250. The loss saved AED 20,250 in Year 2.

Year 3 (2026): Continued profitability

Revenue: AED 1,800,000. Expenses: AED 800,000. Taxable income: AED 1,000,000. No carried-forward loss remaining (fully used in Year 2). Less AED 375,000 band: AED 625,000 taxable at 9% = AED 56,250 CT payable. Filing deadline: September 30, 2027.

If the Year 1 loss had been AED 800,000 instead of AED 400,000, AED 400,000 would remain after Year 2 offset. In Year 3, 75% of AED 1,000,000 = AED 750,000 maximum offset. The remaining AED 400,000 loss would reduce taxable income to AED 600,000, less AED 375,000 band = AED 225,000 at 9% = AED 20,250 CT. Without the remaining loss, CT would be AED 56,250. The additional saving from the carried-forward remainder: AED 36,000 (AED 56,250 minus AED 20,250). Larger losses extend the benefit over more years.

Total CT saving from the AED 400,000 Year 1 loss: AED 20,250 in Year 2. AED 0 additional in Year 3 (loss fully consumed in Year 2). Total: AED 20,250. If the loss had been AED 800,000: AED 20,250 in Year 2 plus AED 36,000 in Year 3 = AED 56,250 total. The loss is a deferred tax asset worth 9% of the loss amount, realized over the years it takes to absorb against future profits.

What the FTA Expects: Documentation and Record-Keeping

Carrying forward a loss is not automatic. The loss must be properly documented on the CT return in the year it is incurred, and the carried-forward balance must be tracked accurately across subsequent returns. The FTA's audit framework includes verification of loss carry-forward claims as a standard audit procedure.

In the loss year: File the CT return on time (deadline: nine months after the tax period end). Report the loss accurately on the return. Maintain the underlying IFRS financial statements that support the loss calculation. Keep all supporting documentation (invoices, contracts, bank statements, payroll records) for at least seven years. The loss is only valid if the return is filed. An unfiled return means the loss does not exist in the FTA's system.

In subsequent years: Report the carried-forward loss balance on each year's CT return. Apply the 75% cap correctly. Track the remaining balance after each year's offset. If the FTA audits a profitable year where you applied a loss offset, they will look back at the loss year to verify the loss amount. If the loss year return is missing, inaccurate, or unsupported, the offset will be disallowed, CT will be reassessed, and penalties will apply.

For group loss transfers: Both entities must include the transfer election on their respective CT returns. The transferring entity reports the reduction in its carried-forward loss balance. The receiving entity reports the loss received and the offset applied. Both returns must be filed for the same tax period. A mismatch in timing (one entity filed, the other did not) can invalidate the transfer.

Six Mistakes Businesses Make With Tax Losses

1. Electing SBR in a loss year. The most expensive mistake. SBR in a loss year saves AED 0 and destroys the future value of the loss. Always model the multi-year impact before electing SBR when the current year is a loss.

2. Not filing the CT return in the loss year. A loss only exists if it is reported on a filed return. An unfiled return means no loss record, no carry-forward, and no future benefit. Plus the AED 500 (first offense) or AED 1,000 (subsequent) late filing penalty applies regardless of whether you owe tax.

3. Attempting to carry forward pre-CT losses. Losses from financial years before the first CT period (before June 1, 2023) cannot be carried forward. Some businesses attempt to include historical losses on their first CT return. The FTA will disallow them.

4. Ignoring the 75% cap. Offsetting more than 75% of current-year taxable income is not permitted. Filing a return that offsets 100% of income using losses will be corrected by the FTA, resulting in a reassessment and possible penalties for incorrect filing. If you discover the error before the FTA does, file a voluntary disclosure to self-correct.

5. Selling more than 50% without checking loss eligibility. A sale of a business where the buyer changes the business activity forfeits the losses. If the carried-forward losses are a meaningful asset, they should be protected in the sale agreement through business continuity provisions.

6. Over-transferring group losses. Transferring more loss than the receiving entity can absorb within the 75% cap wastes the excess. The excess does not bounce back to the transferring entity. Size the transfer to match the receiving entity's absorption capacity, and keep any remainder in the loss-making entity for future carry-forward.

Frequently Asked Questions

How long can I carry forward tax losses in the UAE?

Indefinitely. There is no time limit. A loss from 2024 can be used in 2030 or later, as long as the 50% ownership continuity and business continuity conditions are met.

What is the maximum loss I can offset in any given year?

75% of that year's taxable income. The remaining 25% is always taxable at 9%. You cannot eliminate CT entirely using carried-forward losses (though the AED 375,000 zero-rate band may still bring the final CT to zero).

Does SBR affect my ability to carry forward losses?

Yes. Electing SBR treats taxable income as zero, which means losses are not recognized. A loss year with SBR elected produces no carried-forward loss. The loss is permanently destroyed.

Can I carry losses backward to previous years?

No. The UAE does not allow loss carryback. Losses can only be applied forward against future taxable income.

Can I transfer losses between companies in my group?

Yes, if: one entity holds 75% or more of the other (or a third entity holds 75% of both), both are UAE-resident juridical persons, both have the same financial year and accounting standards, and neither is exempt or a QFZP.

What happens to my losses if I sell more than 50% of the company?

The losses may be forfeited unless the company continues to operate the same or a similar business activity after the ownership change. Listed companies are exempt from this test.

Do I need to file a CT return in a loss year?

Yes. The return is what creates the loss record in the FTA's system. An unfiled return means no recognized loss and no carry-forward benefit. Late filing also attracts penalties.

Can free zone companies carry forward losses?

QFZPs cannot carry forward losses from qualifying income (which is taxed at 0%). Losses from non-qualifying income (taxed at 9%) can be carried forward under the standard rules.

How do I track my carried-forward loss balance?

The balance should be reported on each year's CT return. Maintain a running schedule showing: opening balance, current-year loss (if any), offset applied (capped at 75%), group transfers (if any), and closing balance. Your tax advisor or accountant should maintain this schedule.

Is the loss carry-forward automatic?

No. The loss must be reported on a filed CT return. The carry-forward must be claimed on subsequent returns. Both steps require active filing. Without proper accounting records and timely CT return filing, losses are not preserved.

A Loss Is Not Nothing. It Is a Deferred Tax Asset.

Every AED of tax loss is worth up to 9 fils in future CT savings. An AED 400,000 loss is worth up to AED 36,000. An AED 1,000,000 loss is worth up to AED 90,000. These are not hypothetical numbers. They are real dirhams that stay in your bank account in the years when your business becomes profitable, provided you handled the loss year correctly.

Handling it correctly means: filing the CT return on time, not electing SBR in a loss year (unless the loss is trivial and you will never be profitable), maintaining proper financial statements and supporting documentation, and tracking the carried-forward balance across subsequent returns. Handling it incorrectly means: not filing, electing SBR by default, failing to maintain records, or selling more than 50% of the business without protecting the losses in the transaction documents.

The UAE CT regime is generous with losses. Indefinite carry-forward. Group transfer options. No carryback, but no expiry either. The rules are favorable. The only risk is procedural: making the wrong election, missing a filing, or failing to document the loss. Get the procedure right, and the bad year pays dividends for years to come.

Loss carry-forward planning is part of every year-end review we conduct. We model the SBR trade-off, size group transfers, track carried-forward balances, and ensure your loss years create the maximum future CT saving. Start the conversation on WhatsApp.