An AED 10,000 penalty notification appears on your EmaraTax dashboard. Late CT registration. You had no idea the deadline had passed. Your accountant did not mention it. Your business partner thought VAT registration was the same as CT registration. The penalty is there, the clock is ticking, and nobody told you that the FTA gives you exactly 40 business days to challenge it before it becomes permanent.

Our penalty guide covers what each penalty is, how it is triggered, and how much it costs. Our new penalty regime article covers the April 2026 changes under Cabinet Decision 129/2025. Our voluntary disclosure guide covers how to fix errors before the FTA finds them. Our audit guide covers what to expect during an FTA examination. This article covers the next step: what to do after a penalty has been assessed. The formal process for challenging it, requesting a waiver, applying for an installment plan, or escalating to the Tax Disputes Resolution Committee (TDRC) and the courts. This is the procedural article that sits between 'I have a penalty' and 'how do I make it go away.'

The answer depends on whether the penalty was correctly assessed (in which case, you can request a waiver or installment plan) or incorrectly assessed (in which case, you file a reconsideration requesting the FTA to reverse it). The distinction matters because the process, the evidence, and the likely outcome are different for each path. As Kayrouz & Associates' enforcement analysis documented, the gap between the cost of self-correction and the cost of FTA discovery is where reconsideration requests live. Getting the process right within the 40-day window is what separates a resolved dispute from a permanent financial loss.

"Half the reconsideration requests we file succeed. The other half fail because the evidence was not prepared properly or the deadline was missed. The FTA is not unreasonable. They have a formal process, they follow it, and they reverse penalties when the evidence justifies it. But the evidence must be structured, documented, and submitted within the window. A phone call to the FTA asking for leniency does not work. A properly packaged reconsideration request does."

Jazim, CEO, UAE Tax Filing LLC

Three Paths After Receiving a Penalty: Choose the Right One

Path 1: Reconsideration Request (the penalty is wrong). File a reconsideration request through EmaraTax asking the FTA to review and reverse the penalty. This is for situations where the penalty was issued in error: the FTA assessed a penalty based on incorrect information, you were not actually late, the amount is miscalculated, or the underlying decision (assessment, refund denial, registration refusal) was factually wrong. The reconsideration asks the FTA to re-examine its own decision.

Path 2: Penalty Waiver Request (the penalty is technically correct, but you have a reasonable excuse). You accept that the underlying obligation existed and was not met on time, but you argue that circumstances beyond your control caused the non-compliance. As the FTA's reconsideration portal confirms, you can submit a waiver request alongside a reconsideration, or independently. Force majeure events, system failures, first-offense situations where the error has been rectified, and documented staff or advisor failures are grounds for waiver requests.

Path 3: Installment Plan (you accept the penalty but cannot pay it all at once). The FTA allows businesses to apply for installment payment of penalties. This is not a reduction in the amount owed but a structured payment schedule that prevents further enforcement action while you pay down the balance over time. Useful for businesses facing accumulated penalties (multiple months of late filing, for example) where the total exceeds current cash reserves.

All three can be filed simultaneously. You can submit a reconsideration request (arguing the penalty is wrong), a waiver request (arguing you have a reasonable excuse), and an installment plan application (in case both are rejected) at the same time through EmaraTax. This is the recommended approach for significant penalties: cover all bases within the 40-day window.

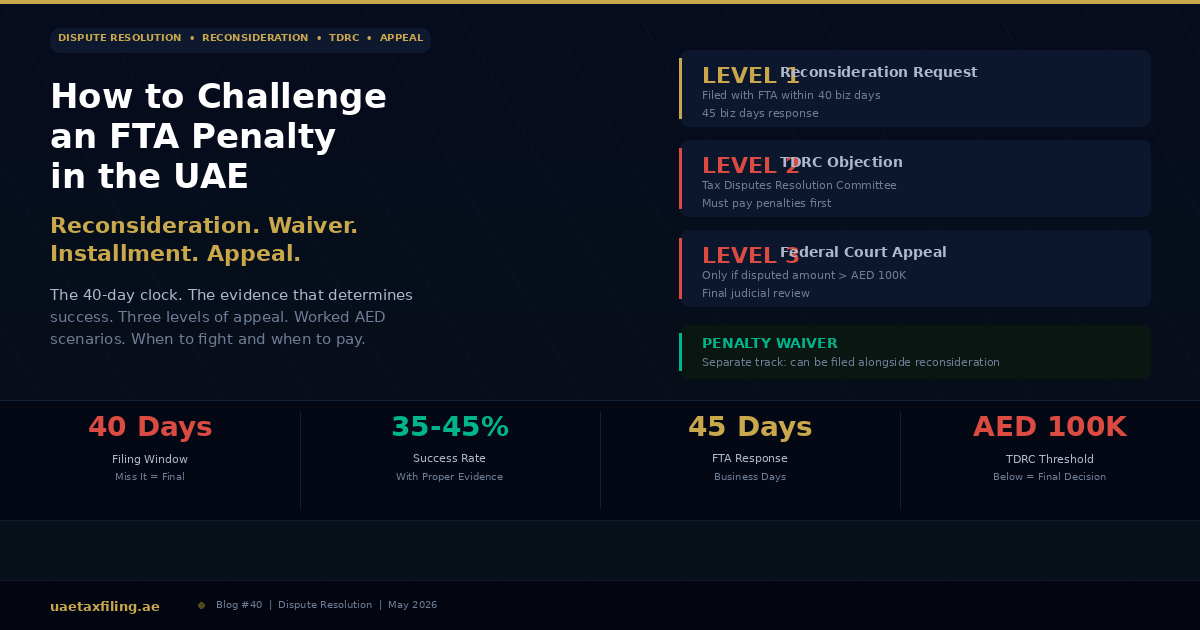

Level 1: The Reconsideration Request (Your First and Best Chance)

The 40-business-day window. From the date the FTA issues its decision (penalty notice, assessment, refund denial, registration refusal), you have 40 business days to submit a reconsideration request through EmaraTax. This is the hard deadline. As the UAE Government's official dispute resolution page confirms, once the 40-day window expires, the right to challenge the decision at this level is lost permanently. There is no extension, no late filing, no second chance. Mark the date on the day you receive the notification.

Who can file. The reconsideration request can be submitted by the taxable person directly, by a registered Tax Agent appointed on EmaraTax, or by a Legal Representative. Tax advisors who are not registered Tax Agents cannot submit reconsideration requests on behalf of clients. This is an important distinction: your accountant or bookkeeper may not have the authority to file unless they are a registered Tax Agent. If you are part of a tax group, the Representative Member must file on behalf of the group.

What happens after filing. The FTA has up to 45 business days to respond (the authority may extend this timeframe in complex cases). During this period, the FTA reviews your submission, examines the evidence, and may request additional information through EmaraTax notifications. The FTA can: uphold its original decision (your reconsideration fails), modify the decision (partially in your favor), or reverse the decision entirely (full success). As CLA Emirates' guide documents, the FTA notifies you of the outcome through EmaraTax within five business days of reaching the decision.

The Evidence That Determines the 35-45% Success Rate

Reconsideration is not a negotiation. It is an evidence-based administrative review. The FTA officer reviewing your request is examining whether the original decision was correct based on the facts and the law. Your submission must provide evidence that the original decision was wrong, not just arguments that it was unfair.

Evidence categories that succeed

FTA procedural or factual error. The FTA assessed a penalty based on incorrect facts. Examples: the FTA recorded the wrong registration date and assessed a late penalty based on the wrong deadline, the FTA applied the wrong penalty rate under the new regime when the old rate should have applied (transitional cases), or the FTA assessed a penalty for a return that was actually filed on time but not recorded in the system due to a technical issue. Evidence: EmaraTax submission confirmations, email acknowledgments, system screenshots showing submission timestamps, FTA correspondence showing the correct dates.

Force majeure or circumstances beyond control. A documented event prevented timely compliance. Examples: a system outage on EmaraTax during the filing window (the FTA publishes scheduled maintenance windows; unexpected outages are documented by the FTA), a medical emergency affecting the sole authorized signatory, natural disasters or government-mandated shutdowns that prevented access to records or systems. Evidence: FTA system outage notices, medical certificates, government shutdown orders, travel restrictions documentation.

First offense with immediate rectification. The business violated the obligation for the first time and immediately corrected the situation once aware. The FTA has discretion to reduce or waive penalties for first-time violations where the taxpayer demonstrates good faith. Evidence: compliance history showing no prior violations, proof of immediate corrective action (the return was filed within days of the missed deadline), evidence that the business has since implemented systems to prevent recurrence (staff training, automated reminders, accounting software calendar alerts).

Advisor or system failure. The business relied on professional advice or software that failed. Examples: the tax agent missed the filing deadline, the accounting software generated an incorrect VAT return that the business filed in good faith, or the bank failed to process the payment before the due date despite timely instruction. Evidence: engagement letter with the tax agent, system error logs, bank transfer instruction timestamps vs processing timestamps. Note: reliance on an advisor does not automatically excuse the taxpayer, but it can support a waiver request if the business demonstrates that it acted reasonably in relying on the advice.

Evidence categories that fail

'I did not know about the law.' Ignorance of the tax obligation is not a valid ground for reconsideration. The FTA's position, consistent with global tax administration practice, is that every taxable person is responsible for knowing their obligations. Not knowing that CT registration was mandatory for all juridical persons (as our CT registration guide explains) is not grounds for reversing the AED 10,000 late registration penalty.

'I cannot afford to pay.' Financial hardship without corrective action does not support a reconsideration. The FTA may consider an installment plan for payment, but it will not reverse a correctly assessed penalty simply because the business cannot pay. The installment path is separate from the reconsideration path.

'My business was not trading.' A dormant company that has not been formally dissolved is still required to register and file nil returns. Not trading is not the same as not existing. The penalty applies to the entity, not to its activity level.

The evidence package determines the outcome. Our team prepares reconsideration requests with properly structured evidence, legal references to the specific articles of the Tax Procedures Law, and clear reasoning that addresses the FTA's decision point by point. Message us on WhatsApp.

The Penalty Waiver: A Separate Track for Reasonable Excuse

A penalty waiver is different from a reconsideration. A reconsideration says: the penalty is wrong, reverse it. A waiver says: the penalty may be technically correct, but I have a reasonable excuse, please reduce or eliminate it. As the FTA portal confirms, both can be filed simultaneously.

Grounds for a waiver. The FTA considers waiver requests based on reasonable excuse: the taxpayer made genuine efforts to comply, the non-compliance was caused by circumstances outside the taxpayer's control, the taxpayer rectified the non-compliance promptly once aware, and the taxpayer has a clean compliance history. The waiver is discretionary. The FTA is not obligated to grant it. But a well-documented waiver request with supporting evidence has a reasonable probability of success, particularly for first-time violations.

The CTP006 waiver for late CT registration. Our CT registration guide covers this in detail. Public Clarification CTP006 provides a structured waiver: file your first CT return within seven months (instead of nine) from the end of your first tax period, and the AED 10,000 late registration penalty is waived. This is not a discretionary waiver. It is an automatic program with clear eligibility criteria. If you qualify, use CTP006 rather than the general waiver process.

Partial waivers. The FTA can grant a partial waiver, reducing the penalty rather than eliminating it entirely. For accumulated late filing penalties (AED 500/month for the first 12 months, AED 1,000/month thereafter), a partial waiver might reduce the accumulated amount by 50% if the business demonstrates that it was unaware of the obligation and rectified it once informed. The FTA has discretion on the percentage.

Installment Plans: When You Accept the Penalty But Need Time to Pay

If the reconsideration is rejected and the waiver is denied, the penalty must be paid. For businesses facing accumulated penalties that exceed their current cash reserves, the FTA offers installment plans.

How installment plans work. You apply through EmaraTax for a structured payment schedule. The FTA reviews your financial situation and proposes a payment plan (typically 3 to 12 monthly installments depending on the amount). While the installment plan is active and payments are being made on schedule, the FTA does not take further enforcement action. Late payment interest (14% per annum) continues to accrue on the outstanding balance during the installment period.

Worked example: A business has accumulated AED 36,000 in penalties: AED 10,000 late CT registration + AED 10,000 late VAT registration + AED 6,000 in late filing penalties (12 months x AED 500) + AED 10,000 record-keeping failure. The business applies for a 6-month installment plan. Monthly payment: AED 6,000 plus accruing interest. The total cost is higher than paying in full (because of the 14% interest on the outstanding balance), but the cash flow impact is manageable.

Level 2: The Tax Disputes Resolution Committee (TDRC)

If the FTA rejects your reconsideration request (or fails to respond within 45 business days), the next level is the TDRC. As Kayrouz & Associates' detailed process guide explains, the TDRC is an independent committee established under the Tax Procedures Law to review taxpayer objections to FTA decisions. It is not part of the FTA. It provides an independent review of the dispute.

The 40-business-day objection window. You have 40 business days from the date of the FTA's reconsideration decision (or from the date the 45-day response period expired without a decision) to file an objection with the TDRC. This is a separate 40-day window from the original reconsideration filing window. If the FTA rejected your reconsideration on April 15, you have until approximately June 12 (40 business days later) to file the TDRC objection.

The pay-before-appeal rule. This is the most significant barrier to TDRC access. Before the TDRC will accept your objection, you must have paid all disputed tax and penalties in full. The TDRC will not review your case while amounts remain outstanding. For a business disputing AED 50,000 in penalties, this means paying AED 50,000 to the FTA before the TDRC even begins to consider whether the penalty was correct. If the TDRC rules in your favor, the FTA refunds the amount. But the cash must be paid upfront. This creates a significant cash flow challenge for SMEs with large disputed amounts.

The TDRC process. The TDRC reviews the objection and gives both parties (the taxpayer and the FTA) an opportunity to present their positions. The TDRC issues its decision within 20 business days of receiving the objection, with the option to extend by an additional 20 business days if the case is complex. Both parties are notified within five business days of the decision.

The AED 100,000 finality threshold. If the combined disputed tax and penalty amount is below AED 100,000, the TDRC's decision is final and binding. Neither party can appeal to the courts. For disputes exceeding AED 100,000, either party may appeal the TDRC decision to the competent federal court within 40 business days of notification. This means that for the majority of SME penalty disputes (which typically involve AED 10,000-50,000 in penalties), the TDRC is the last stop. There is no further appeal. As Hallmark International's 2026 penalty guide documented, the TDRC's decision carries significant weight because for smaller disputes, it is truly final.

Level 3: Federal Court Appeal (Disputes Above AED 100,000)

For disputes where the combined tax and penalty amount exceeds AED 100,000, either the taxpayer or the FTA can appeal the TDRC's decision to the federal court. The appeal must be filed within 40 business days of notification of the TDRC's decision.

Court appeals are rare for most UAE businesses. The cost of legal representation, the time involved (court proceedings can take months to years), and the uncertainty of outcome make court appeals practical only for large disputed amounts where the business has strong legal grounds and the financial exposure justifies the litigation cost. For the vast majority of SME tax disputes, the process ends at the TDRC.

Businesses considering a court appeal should engage specialized tax litigation counsel. General corporate lawyers or tax advisors may not have the litigation experience required for federal court proceedings. The court reviews the case on its merits, including the factual record and the application of the tax law, and can uphold, modify, or overturn the TDRC's decision.

From reconsideration to TDRC objection to court appeal, our team represents clients through every level of the dispute process. We prepare the evidence package, file the reconsideration within the 40-day window, coordinate waiver and installment applications, and manage TDRC proceedings if escalation is needed. Talk to us on WhatsApp.

Three Worked Scenarios: When to Fight, When to Pay, When to Negotiate

Scenario 1: Late CT Registration (AED 10,000) - Fight or Use CTP006

A Dubai LLC incorporated in March 2020. Never registered for CT. Registration deadline was June 30, 2024 (March-April licence band under Cabinet Decision 10/2024). The owner discovers the obligation in February 2026 and registers immediately. Our CT registration guide covers the staggered deadline schedule, and our VAT registration guide covers the separate VAT registration obligation that this business also likely missed. The AED 10,000 CT penalty appears on the EmaraTax account.

Option A: CTP006 waiver. First tax period ended December 31, 2024. Seven-month waiver deadline: July 31, 2025. If the company already filed its first CT return by July 31, 2025, the CTP006 waiver applies automatically. If not, this option has expired.

Option B: General reconsideration. File within 40 business days of the penalty notification. Argue that the business was unaware of the obligation and rectified immediately upon discovery. Provide evidence of clean compliance history, immediate registration upon awareness, and systems implemented to prevent recurrence. Success probability: moderate (30-40%) because ignorance of the law is weak grounds, but immediate rectification and first-offense status improve the case.

Option C: Accept and pay. AED 10,000 is a fixed cost. For a business with AED 1M+ revenue, it is 1% of revenue and not worth the time and professional fees of a contested reconsideration. Pay the penalty, register, file the return, and move on. As our real cost of CT article showed, the total compliance cost including this penalty is still a fraction of what the same business would pay in CT in any other major economy.

Scenario 2: Accumulated Late Filing Penalties (AED 8,500) - Negotiate a Partial Waiver

A free zone company registered for CT in 2024 but never filed its first CT return. The return for the period ending December 31, 2024 was due September 30, 2025 per our CT deadlines guide. The company finally files through EmaraTax in March 2026, six months late. Accumulated late filing penalties: AED 500/month for 6 months = AED 3,000. Plus late payment interest on any CT owed during the period. The company also failed to file its quarterly VAT returns for two quarters. Additional VAT late filing penalties: AED 1,000 (first offense) + AED 2,000 (repeat within 24 months) + late payment penalties. Total exposure: approximately AED 8,500.

Recommended approach: File a waiver request for the CT late filing penalties (AED 3,000), arguing first offense and immediate rectification. Simultaneously file a waiver request for the VAT penalties (AED 3,000+), with the same argument. Request an installment plan for any amount that is not waived. Expected outcome: partial waiver reducing the total by 30-50% (AED 2,500-4,250 saved). Filing the waiver costs less than the potential saving. Worth pursuing.

Scenario 3: Incorrect VAT Assessment (AED 85,000) - Fight Through to TDRC

The FTA conducted a VAT audit and assessed AED 85,000 in additional output VAT, arguing that certain supplies classified as zero-rated exports should have been standard-rated domestic supplies. The company disagrees: the supplies were physically exported, with shipping documents and customs declarations proving the goods left the UAE. The FTA's assessment is based on incomplete information (the auditor did not have the full set of export documentation). This type of dispute is increasingly common as the 2026 regulatory changes give the FTA broader audit powers. If the assessment stands, the company also loses the input VAT credit position associated with the incorrectly reclassified supplies.

Step 1: Reconsideration. File within 40 business days with complete export documentation (shipping bills, customs declarations, bills of lading, buyer purchase orders from the foreign jurisdiction). Argue that the supplies meet the conditions for zero-rating under Article 30 of the VAT Executive Regulation. Success probability: high (50-60%) with complete documentation, because the FTA's assessment was based on missing evidence.

Step 2: If reconsideration fails. Pay the AED 85,000 (plus any penalties). File a TDRC objection within 40 business days of the reconsideration decision. Present the full export documentation to the independent committee. Since AED 85,000 is below AED 100,000, the TDRC decision is final. If the TDRC rules in favor, the FTA refunds the AED 85,000.

This scenario justifies fighting because the amount is significant (AED 85,000), the evidence supports the taxpayer's position (physical export documentation), and the FTA's assessment appears to be based on incomplete information. The professional cost of preparing the reconsideration and potential TDRC objection (AED 5,000-15,000 in tax advisory fees) is well below the disputed amount.

The Decision Framework: When to Fight, When to Pay

Fight when: the penalty is based on incorrect facts (you have evidence the FTA's decision was wrong), the disputed amount significantly exceeds the professional cost of the reconsideration (AED 3,000-15,000 depending on complexity), the evidence supports your position clearly and can be documented, the penalty resulted from circumstances genuinely outside your control (system failure, force majeure, advisor error), or the CTP006 waiver applies and you have not yet filed.

Pay when: the penalty is correct and you do not have a reasonable excuse, the amount is small relative to the professional cost of challenging it (challenging an AED 500 late filing penalty is not worth AED 3,000 in advisory fees), the 40-day window has already expired, or the underlying compliance failure is clear and your efforts are better spent on future compliance than on contesting the past. As our penalties guide documents, the compounding effect of ongoing non-compliance is far more expensive than any single penalty. Paying a penalty and bringing compliance current is often the most financially rational decision.

Negotiate when: the accumulated penalties are significant but you accept the underlying violations (partial waiver request), you cannot pay the full amount immediately (installment plan), or the penalty is technically correct but the circumstances were unusual and the FTA might exercise discretion (waiver based on reasonable excuse). Negotiation through waiver and installment is the middle path between fighting and paying, and it is the most common approach for businesses facing accumulated penalties from multiple violations.

Six Mistakes Businesses Make When Challenging Penalties

1. Missing the 40-business-day window. This is the most common and most costly mistake. The window starts from the date the FTA issues its decision, not from the date you notice it on EmaraTax. Check your EmaraTax notifications daily during any period of FTA interaction. One missed notification can mean a permanently lost right to challenge.

2. Filing without evidence. A reconsideration request that says 'I disagree with this penalty' without supporting documentation will be rejected. The FTA reviews evidence, not opinions. Every claim must be documented: screenshots, timestamps, bank records, medical certificates, system logs, correspondence.

3. Using a non-registered tax advisor to file. Only the taxpayer, a registered Tax Agent, or a Legal Representative can submit reconsideration requests. A tax consultant or accountant who is not registered as a Tax Agent with the FTA cannot file on your behalf. Verify your advisor's registration status before the 40-day window expires.

4. Not paying before TDRC escalation. The TDRC will not accept your objection until all disputed amounts are paid. Businesses that file a TDRC objection without paying first waste the 40-day window. Pay the disputed amount, file the objection, and seek a refund if the TDRC rules in your favor.

5. Fighting a small penalty at high cost. Engaging a tax advisor to challenge an AED 500 late filing penalty costs more than the penalty itself. Not every penalty is worth contesting. Calculate the cost-benefit before engaging professional support.

6. Not filing a voluntary disclosure before the penalty is assessed. If you discover an error before the FTA does, a voluntary disclosure reduces the penalty significantly (1% per month on the underpaid tax, vs 15% + 1%/month if the FTA discovers it). Self-correction before assessment is always cheaper than challenging an assessment after the fact. Our 9 mistakes article covers the most common errors that trigger FTA assessments.

Frequently Asked Questions

How long do I have to challenge an FTA penalty?

40 business days from the date the FTA issues its decision. This deadline is absolute. Missing it means the penalty becomes final with no further appeal at Level 1.

Can I file a reconsideration and a penalty waiver at the same time?

Yes. The FTA allows simultaneous submission of reconsideration requests, waiver applications, and installment plan requests through EmaraTax.

What is the success rate for reconsideration requests?

Approximately 35-45% across sectors when properly documented. Success depends entirely on evidence quality and the specific grounds for the challenge. Input VAT recovery disputes have the highest reversal rates at approximately 48%.

Do I have to pay the penalty before appealing to the TDRC?

Yes. All disputed tax and penalties must be paid in full before the TDRC accepts your objection. If the TDRC rules in your favor, the FTA refunds the amount.

Is the TDRC decision final?

For disputes below AED 100,000 in combined tax and penalties, the TDRC decision is final. Neither party can appeal to the courts. For disputes above AED 100,000, either party can appeal to the federal court within 40 business days.

Can my accountant file the reconsideration for me?

Only if they are a registered Tax Agent with the FTA. Tax advisors, consultants, and bookkeepers who are not registered Tax Agents cannot submit reconsideration requests on behalf of clients.

What is the CTP006 penalty waiver?

A structured waiver for the AED 10,000 late CT registration penalty. File your first CT return within seven months (instead of nine) from the end of your first tax period, and the penalty is automatically waived. Covered in detail in our CT registration guide.

How long does the FTA take to respond to a reconsideration?

Up to 45 business days, with the possibility of extension in complex cases. The FTA notifies you of the outcome within five business days of reaching its decision.

Can I get an installment plan for penalty payments?

Yes. Apply through EmaraTax. The FTA reviews your financial situation and proposes a payment schedule, typically 3-12 months. Late payment interest (14% per annum) accrues on the outstanding balance during the installment period.

Should I hire a professional for a reconsideration request?

For penalties above AED 5,000, yes. The professional cost (AED 3,000-15,000 depending on complexity) is justified by the potential saving. For smaller penalties, a DIY approach may be sufficient if you can prepare the evidence package yourself.

40 Days. One Window. Three Paths.

Every FTA penalty comes with a clock. Forty business days to file a reconsideration, a waiver request, or both. That clock starts from the date the decision is issued, not from the date you read the notification, not from the date you discuss it with your accountant, and not from the date you decide to act. The only date that matters is the one on the FTA's decision notice.

The process is fair. The FTA reverses penalties when the evidence justifies it. The TDRC provides an independent review when the FTA does not. The courts provide a final review for larger disputes. But every level requires action within a window, evidence that is documented, and a submission that is properly filed through the correct channel by an authorized person.

If you have received a penalty, check the date. Calculate your 40-day deadline. Gather your evidence. Choose your path: fight, negotiate, or pay. Then act before the window closes.

Penalty reconsideration requests require fast action and proper evidence. We prepare and file reconsideration requests, waiver applications, and TDRC objections for clients facing FTA penalties across VAT, CT, and excise. The 40-day window does not wait. Start on WhatsApp.