A Dubai holding company pays AED 500,000 in management fees to its parent in the UK. In most countries, the paying entity would deduct 10% to 25% at source and remit it to the tax authority. The UK recipient would receive AED 375,000 to AED 450,000, with the rest sitting in the source country's treasury. In the UAE, the recipient receives the full AED 500,000. No deduction. No withholding. No remittance to the FTA. The money leaves the UAE untouched.

The same holding company receives AED 300,000 in dividends from a subsidiary in India. India applies withholding tax at source. Without a tax treaty, India would withhold 20% (AED 60,000). With the UAE-India treaty, the rate drops to 10% (AED 30,000). The UAE company receives AED 270,000. To claim the reduced treaty rate, the UAE company must present a valid Tax Residency Certificate (TRC) to the Indian tax authority. Without the TRC, India applies the full 20% domestic rate and keeps the extra AED 30,000.

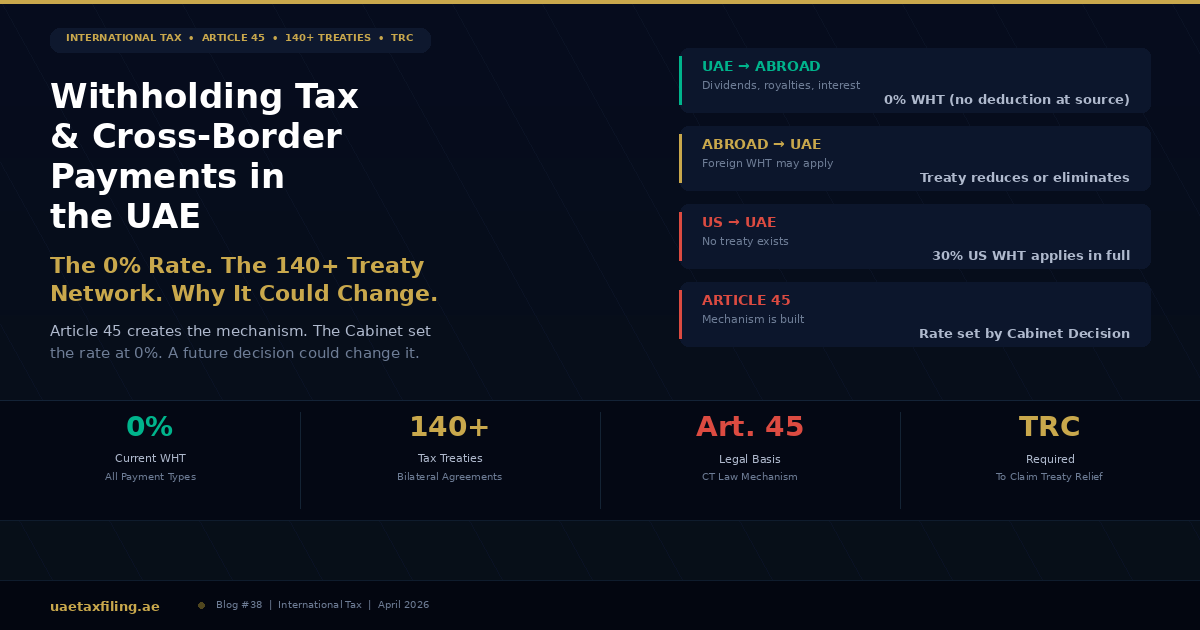

These two scenarios capture the entire structure of UAE withholding tax: outbound payments from the UAE carry 0% WHT (no deduction at source), but inbound payments to the UAE may carry foreign WHT that treaties can reduce. As Kayrouz & Associates' cross-border analysis documented, the 0% rate is one of the core reasons the UAE functions as a holding, treasury, and IP licensing jurisdiction for international groups. But the 0% rate is a policy choice, not a permanent fixture. Article 45 of the Corporate Tax Law builds the withholding tax mechanism. The Cabinet set the rate at zero. A future Cabinet Decision could set it at five, ten, or fifteen percent without amending the law itself. The infrastructure is built. The switch is off. For now.

"Most of our international clients come to us with two questions. First: does the UAE charge withholding tax on my payments abroad? No. Second: how do I stop foreign countries from withholding tax on my payments into the UAE? That requires a Tax Residency Certificate, the right treaty, and proper documentation. The first question takes ten seconds. The second question takes the rest of the meeting."

Jazim, CEO, UAE Tax Filing LLC

The 0% Rate: What It Means and Where It Comes From

Article 45 of Federal Decree-Law No. 47 of 2022 (the UAE Corporate Tax Law) establishes withholding tax on UAE-sourced income paid to non-residents who do not have a permanent establishment or nexus in the UAE. The tax is imposed on the non-resident recipient, but the UAE payer is responsible for deducting and remitting it. As EAS MEA's practical guide explains, the payer acts as the collection agent for the FTA.

The rate is not set by the CT Law itself. The CT Law creates the mechanism and delegates the rate to a Cabinet Decision. The Cabinet has set the rate at 0% for all categories of payment: dividends, interest, royalties, service fees, management charges, and any other UAE-sourced income paid to non-residents. As ClearTax's WHT overview documents, there is no distinction between payment categories. Everything is 0%.

What 0% means in practice. No deduction at source. When a UAE company pays an invoice to a foreign supplier, consultant, licensor, or parent company, the full invoiced amount is remitted. No portion is held back. No WHT return is filed with the FTA. No reporting obligation exists for these payments at the 0% rate. The foreign recipient receives 100% of the payment.

Why 0% is not the same as 'no withholding tax.' This is the distinction that matters for long-term planning. Article 45 creates a withholding tax system. The Cabinet set the rate at zero. A future Cabinet Decision could change the rate to 5%, 10%, or any other figure without amending the CT Law, without parliamentary process, and without public consultation beyond whatever the Cabinet chooses to conduct. The legal infrastructure for positive WHT exists. The rate is currently zero by executive choice. Businesses that structure their international operations around the assumption that 0% is permanent should understand that it is a policy position, not a legislative guarantee. As Chambers & Partners' UAE practice guide notes, the 0% rate means that in practice these payments are not subject to any tax, but the mechanism is in place for a future change.

Outbound Payments: UAE to Foreign Recipients

Every payment a UAE company makes to a non-resident falls under the same 0% treatment. The payment type does not matter. The recipient's country does not matter. The amount does not matter. As long as the current 0% rate is in effect, all outbound payments are made gross.

Dividends. A UAE parent distributing profits to a foreign shareholder sends the full amount. No UAE tax is deducted. For international groups that use the UAE as a holding jurisdiction, this is the structural advantage: profits earned by UAE subsidiaries can be repatriated to the ultimate parent without any UAE-level tax leakage. Combined with the 9% CT rate (or 0% for QFZPs), the total tax cost on profits earned and distributed through the UAE is among the lowest in the world. Our real cost of CT article quantifies the effective rate at 0% to 4% of revenue for most businesses.

Royalties and licensing fees. A UAE subsidiary paying royalties to a foreign parent for the use of IP (trademarks, patents, technology licences) sends the full amount. This is why the UAE is increasingly used as an IP licensing hub: the 0% WHT on outbound royalties means the full royalty payment reaches the IP owner without source-country tax erosion. However, the transfer pricing rules require that the royalty rate be at arm's length. Inflated royalty payments designed to shift profits out of the UAE will be challenged by the FTA under Article 34 of the CT Law.

Service fees and management charges. Inter-company management fees, technical service fees, and consulting payments to foreign affiliates or independent contractors are all paid gross. For multinational groups that centralize management functions in a regional headquarters (often the UAE), this means the management charges flowing from UAE subsidiaries to the regional HQ, or from the HQ to foreign affiliates, carry no UAE WHT. The transfer pricing disclosure on Schedule 5 of the CT return must include these payments if they are between related parties.

Interest payments. A UAE company paying interest on a loan from a foreign lender sends the full interest amount. No UAE deduction. For international debt structuring, this means UAE entities can service external debt without WHT friction. The interest itself may or may not be deductible for CT purposes (the general interest deduction limitation and the specific anti-abuse rules under the CT Law apply), but the WHT on the payment to the foreign lender is zero.

Inbound Payments: Foreign Sources to UAE Companies

The 0% rate is a UAE domestic rate. It governs what the UAE does to outbound payments. It does not govern what foreign countries do to payments they send to the UAE. When a UAE company receives dividends, royalties, interest, or service fees from abroad, the source country applies its own withholding rules. The UAE's 140+ double tax treaty network exists to reduce or eliminate that foreign withholding.

How treaties reduce foreign WHT. A double tax treaty (DTT) between the UAE and a foreign country typically caps the WHT rate that the source country can apply. As PwC's UAE WHT rate table documents, treaty rates vary by country and payment type. The UAE-India treaty reduces dividend WHT from India's domestic 20% to 10%. The UAE-UK treaty reduces royalty WHT from the UK's domestic rate to 0%. The UAE-Germany treaty limits dividend WHT to 5-15% depending on the shareholding percentage. Each treaty is different, and the applicable rate depends on the specific payment type, the shareholding structure, and the treaty provisions.

Worked example: UAE company receiving dividends from India

Without treaty: Indian subsidiary pays AED 1,000,000 in dividends to UAE parent. India applies 20% domestic WHT. AED 200,000 withheld by India. UAE parent receives AED 800,000. With UAE-India treaty: India applies 10% treaty rate. AED 100,000 withheld. UAE parent receives AED 900,000. Treaty saving: AED 100,000. The UAE parent needs a valid TRC to claim the reduced 10% rate. Without the TRC, India applies the full 20% and the UAE company loses AED 100,000.

Worked example: UAE company receiving royalties from Germany

A UAE technology company licences software to a German client. The German client pays AED 500,000 in royalties. Germany applies WHT on outbound royalty payments. The UAE-Germany treaty limits royalty WHT to 0%. With a valid TRC and proper treaty claim, the German payer remits the full AED 500,000 to the UAE company. Without the TRC, Germany applies its domestic rate and withholds approximately AED 75,000 (15% statutory rate). Treaty saving: AED 75,000.

Treaty analysis, TRC applications, and cross-border payment structuring require specialist knowledge of both UAE and foreign tax law. Our corporate tax team handles the full chain: identifying the applicable treaty rate, securing the TRC, preparing the documentation for the foreign tax authority, and ensuring the payment flow is tax-efficient. Message us on WhatsApp.

The US Gap: No Treaty, No Relief

The UAE and the United States do not have a double tax treaty. This is the single largest gap in the UAE's treaty network and it affects every UAE business with US-source income. Without a treaty, the US applies its full domestic WHT rates to payments made to UAE entities: 30% on dividends, 30% on certain interest payments, and 30% on royalties. There is no mechanism to reduce these rates.

What this means for UAE companies with US investments. A UAE holding company that owns shares in a US corporation receives dividends with 30% withheld at source. On AED 1,000,000 in dividends, AED 300,000 stays with the US Internal Revenue Service. The UAE company receives AED 700,000. This is the single highest WHT cost for UAE companies earning income from any major economy, because every other major economy (UK, Germany, France, India, China, Singapore, Japan) has a treaty with the UAE that reduces the rate significantly.

Planning around the gap. Some international groups route US-source income through a treaty jurisdiction (an intermediate holding company in a country that has both a US treaty and a UAE treaty). This type of structuring is legal but must have genuine economic substance in the intermediate jurisdiction. Treaty shopping (using a conduit entity with no real activity) is increasingly challenged by both the US under its Limitation on Benefits provisions and by other jurisdictions under the OECD's Principal Purpose Test. The structure must have commercial rationale beyond tax savings. For multi-entity groups already operating in the UAE, tax group formation can consolidate the compliance burden while maintaining the structural benefits. Our transfer pricing guide covers the substance requirements that apply to inter-group structures, and our guide to choosing a tax firm helps identify advisors with genuine cross-border capability.

The UAE and the US have signed an Intergovernmental Agreement under the Foreign Account Tax Compliance Act (FATCA) for information exchange, but FATCA is not a tax treaty. It does not reduce WHT rates. It only governs financial account reporting. A full income tax treaty between the UAE and the US remains under discussion but has not been concluded as of April 2026.

The Tax Residency Certificate: Your Ticket to Treaty Benefits

A Tax Residency Certificate (TRC) is an official document issued by the UAE Ministry of Finance confirming that the entity or individual is tax-resident in the UAE for the purposes of a specific double tax treaty. Foreign tax authorities require the TRC before they apply the reduced treaty WHT rate. Without a valid TRC, the foreign payer applies the full domestic rate.

Who issues the TRC. The Ministry of Finance, not the FTA. The application is submitted through the Ministry of Finance's online portal. The FTA handles CT and VAT registration and filing; the Ministry of Finance handles tax residency certification and treaty matters.

TRC requirements for companies

A UAE company applying for a TRC must demonstrate genuine tax residency in the UAE. The Ministry evaluates: the company must have been operating for at least 12 months, must hold a valid and active trade licence, must have audited financial statements (or at minimum, management accounts showing real activity), must demonstrate adequate substance in the UAE (employees, office space, operational decision-making conducted from the UAE), and must have an active CT registration (Blog #37 covers the registration process). The application requires the company's TRN, trade licence, financial statements, proof of address, and a statement of the specific treaty country for which the TRC is needed. Processing time is typically 2 to 4 weeks.

TRC requirements for individuals

An individual applying for a TRC must demonstrate UAE tax residency under Cabinet Decision No. 85 of 2022. The primary test is the 183-day rule: physical presence in the UAE for at least 183 days in a consecutive 12-month period. An alternative 90-day test applies if the individual holds a UAE residence permit and has either a permanent place of residence or employment in the UAE. Required documents: valid residence visa, Emirates ID, passport with entry/exit stamps or ICA travel report, tenancy contract or title deed, bank statements showing UAE activity, and proof of employment or business activity.

TRC validity. TRCs are issued for a specific calendar year and must be renewed annually. A 2025 TRC is not valid for claiming treaty benefits on 2026 income. Renewal is not automatic: the application must be re-submitted with updated financial statements and substance documentation each year.

The TRC matters more now than before 2023. Before the UAE introduced corporate tax, the TRC was primarily a convenience for accessing treaty benefits on passive income. Now that the UAE has a 9% CT regime, the TRC carries additional weight. It confirms that the entity is a genuine taxable person in the UAE, which strengthens substance arguments for transfer pricing, supports the entity's position under BEPS anti-abuse provisions, and is increasingly required by international banks and counterparties as proof that the UAE entity is a real, tax-compliant business. As Chambers & Partners documented, while the UAE tax authorities generally accept the use of treaty country entities, they scrutinize arrangements that appear artificial or solely aimed at securing treaty benefits.

Documentation: What to Keep Even at 0%

At the current 0% rate, no WHT return is filed and no deduction is made. But documentation still matters, for three reasons.

Reason 1: The rate could change. If the Cabinet introduces a positive WHT rate, the FTA will expect businesses to demonstrate their historical payment flows. Maintaining records of all cross-border payments (recipient identity, nature of payment, amount, date, applicable WHT rate) creates a clean trail that protects the business if the rules change retroactively or prospectively. As EAS MEA's guide advises, this documentation becomes relevant if the rate changes, if the FTA audits the company's CT position, or if the foreign recipient needs evidence of the UAE tax treatment.

Reason 2: CT deductibility. Cross-border payments to related parties must be at arm's length and properly documented for CT deduction purposes. A management fee paid to a foreign parent is deductible for UAE CT only if it meets the arm's length standard and is supported by proper documentation (inter-company agreement, service delivery evidence, pricing benchmarking). Your accounting service should categorize cross-border payments separately in the chart of accounts so they are identifiable at CT filing time. Our deductions guide covers which expenses are deductible and which are not. The WHT rate is 0%, but the CT deductibility of the underlying payment depends on separate rules.

Reason 3: Foreign treaty claims. When a UAE company receives payments from abroad and claims treaty relief on foreign WHT, the foreign tax authority may request evidence of the UAE treatment of outbound payments. A clean record of outbound payments with their WHT treatment (currently 0%) supports the company's overall international tax position.

Cross-border payment documentation is part of every CT return we prepare. We record outbound and inbound payment flows, maintain the TRC renewal schedule, prepare treaty relief claims for foreign tax authorities, and ensure all related party disclosures are complete. Talk to us on WhatsApp.

Pillar Two and the Global Minimum Tax: The Bigger Picture

The OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting (BEPS) introduced Pillar Two, which establishes a global minimum effective tax rate of 15% for multinational enterprises (MNEs) with consolidated annual revenue of EUR 750 million or more. The UAE introduced a Domestic Minimum Top-Up Tax (DMTT) effective January 1, 2025, to ensure that UAE entities within large MNE groups pay at least 15% effective tax on their UAE income.

Who is affected. Only MNEs with consolidated global revenue of EUR 750 million or more. The vast majority of UAE businesses, including all SMEs, are entirely outside the scope of Pillar Two. A UAE LLC earning AED 10 million or even AED 100 million is not affected unless it is part of a group with EUR 750 million+ in consolidated revenue.

How it interacts with WHT. For in-scope MNEs, the 0% WHT rate does not directly affect the Pillar Two calculation (which is based on effective tax rates on profits, not on withholding rates on payments). However, the existence of a 9% CT rate in the UAE means that UAE entities within in-scope MNE groups already pay some corporate tax, which counts toward the 15% minimum. The DMTT ensures that any shortfall between the effective rate and 15% is collected by the UAE rather than by a foreign jurisdiction applying an Income Inclusion Rule.

For most readers of this article. Pillar Two is not relevant. It applies to a small number of very large multinationals. The 0% WHT rate, the 9% CT rate, and the treaty network are the relevant considerations for UAE businesses conducting cross-border transactions. Our 2026 tax changes guide covers the broader regulatory context, including the DMTT introduction.

How WHT Interacts With the Reverse Charge Mechanism

WHT and the reverse charge mechanism are separate systems that apply to different taxes on the same cross-border transaction. WHT is a CT mechanism (income tax on the non-resident recipient, deducted at source). The reverse charge is a VAT mechanism (VAT on imported services, self-accounted by the UAE buyer). Both can apply to the same payment.

Example: A UAE company pays AED 100,000 to a UK consultant for services performed remotely. WHT at 0% means no income tax is deducted from the payment. The reverse charge mechanism means the UAE company must self-account for 5% VAT (AED 5,000) on its VAT return, reporting both output VAT (AED 5,000) and input VAT (AED 5,000, recoverable if the service is for taxable business purposes). The UK consultant receives the full AED 100,000. The UAE company's net VAT position is zero (output and input cancel). But both the WHT and VAT treatments must be documented correctly on the respective returns.

For businesses that regularly pay foreign suppliers for services, understanding both mechanisms in parallel is essential. The WHT treatment is currently simple (0%, no action). The VAT reverse charge requires active accounting entries on every quarter's VAT return. The CT treatment requires confirming the payment is deductible under the arm's length standard and properly disclosed if the foreign supplier is a related party.

Five Mistakes Businesses Make With Cross-Border Tax

1. Assuming 0% WHT means no compliance obligation. At 0%, there is no WHT filing. But the CT deductibility of the underlying payment, the VAT reverse charge on imported services, the transfer pricing documentation for related party payments, and the TRC for claiming foreign treaty relief all create separate obligations. 0% WHT simplifies one step. It does not eliminate the others.

2. Not securing a TRC before receiving foreign payments. Foreign payers apply their domestic WHT rate unless they see a valid TRC. Once the foreign tax is withheld, recovering it requires a formal refund claim through the foreign tax authority, which can take months or years. Getting the TRC in advance costs a few hours of paperwork and saves potentially hundreds of thousands of dirhams in foreign WHT.

3. Treating the 0% rate as permanent in long-term structuring. IP licensing entities, holding companies, and treasury centers structured around the 0% WHT assumption should have contingency plans for a positive rate. Contract terms, pricing models, and inter-company agreements should include provisions for rate changes. Building a multi-decade structure on a Cabinet Decision that can change with a single announcement is a risk that should be acknowledged and planned for.

4. Ignoring US-source income tax implications. UAE companies earning dividends, royalties, or interest from the US face 30% federal WHT with no treaty relief. Some businesses discover this only after their first US payment arrives 30% short. If you have US-source income, consult a cross-border tax specialist before the first payment is made.

5. Not disclosing cross-border related party payments on the CT return. All payments to related parties must be disclosed on Schedule 5 of the CT return, regardless of the WHT rate. The FTA cross-references related party disclosures with VAT data and transfer pricing records. Missing disclosures are a known audit trigger.

Frequently Asked Questions

Does the UAE charge withholding tax on payments to foreign companies?

The UAE has a withholding tax mechanism under Article 45 of the CT Law, but the rate is currently set at 0% by Cabinet Decision. No deduction is made at source on any payment type (dividends, interest, royalties, service fees).

Could the 0% rate change in the future?

Yes. The rate is set by Cabinet Decision, not by the CT Law itself. The Cabinet can introduce a positive rate without amending the law. There is no public indication of an imminent change, but the legal mechanism for a change exists.

What is a Tax Residency Certificate and why do I need one?

A TRC is issued by the Ministry of Finance confirming UAE tax residency for treaty purposes. Foreign tax authorities require it before applying reduced treaty WHT rates on payments to UAE entities. Without a TRC, the full foreign domestic rate applies.

Does the UAE have a tax treaty with the United States?

No. The UAE and the US do not have a double tax treaty. US-source income paid to UAE entities is subject to the full US domestic WHT rate (generally 30% on dividends and royalties). There is no mechanism to reduce this rate.

How many double tax treaties does the UAE have?

Over 140 treaties as of April 2026, covering major trading partners including the UK, India, Germany, France, China, Singapore, Japan, and most EU member states. The treaty network is one of the most extensive in the world.

Do I need to file a WHT return at the 0% rate?

No. At 0%, no WHT return is required and no reporting obligation exists for the withholding itself. However, the underlying payments may need to be disclosed on the CT return (Schedule 5 for related party payments) and accounted for under the VAT reverse charge.

How does WHT interact with the reverse charge mechanism?

They are separate systems. WHT is a CT mechanism (income tax). The reverse charge is a VAT mechanism (self-accounted VAT on imported services). Both can apply to the same payment. Currently, WHT requires no action (0%), while the reverse charge requires active entries on the VAT return.

Can I claim a credit for foreign tax withheld on payments to my UAE company?

The UAE CT Law provides for foreign tax credits under certain conditions. Foreign WHT paid on income that is also subject to UAE CT may be creditable against the UAE CT liability, subject to limitations. Consult a tax advisor for your specific situation.

Does Pillar Two affect my business?

Only if your business is part of a multinational group with consolidated global revenue of EUR 750 million or more. For all other UAE businesses, Pillar Two is not applicable. The 0% WHT rate and 9% CT rate are the relevant considerations.

Should I structure my business in a free zone for cross-border tax efficiency?

Possibly. A free zone QFZP earning qualifying income from international clients pays 0% CT. Combined with the 0% WHT rate, the total UAE tax cost on qualifying international income is zero. However, QFZP status requires substance, audit, and compliance with strict qualifying income rules. Note that UAE-source rental income is specifically excluded from qualifying income. Our free zone vs mainland comparison covers the full analysis.

The Switch Is Off. The Mechanism Is Built.

The UAE's 0% withholding tax rate on outbound payments is one of the most commercially significant features of the country's tax framework. It makes the UAE one of the most efficient jurisdictions in the world for holding companies, IP licensing, treasury operations, and profit repatriation. The 140+ treaty network extends this efficiency by reducing foreign WHT on inbound payments, provided the UAE entity holds a valid TRC.

But the 0% rate is not a constitutional guarantee. Article 45 of the CT Law creates the mechanism. The Cabinet set the rate. The Cabinet can change it. No business should panic about this possibility, but every business that structures its international operations around the 0% assumption should know that the assumption rests on a single executive decision, not on a permanent legal principle.

For now, the rate is zero. The treaties are in place. The TRC is available. The documentation requirements are minimal. The strategic advantage is real. Use it, plan for it, but do not assume it is forever.

International tax structuring, TRC applications, treaty analysis, and cross-border payment documentation are specialist services. Our team advises UAE businesses on the full international tax chain: outbound WHT (currently 0%), inbound treaty relief (TRC-dependent), CT deductibility of cross-border payments, and VAT reverse charge compliance. Start on WhatsApp.