Every year, more than 40,000 new trade licences are issued in Dubai alone. The first question every one of those entrepreneurs faces is the same: free zone or mainland? Before June 2023, the answer was mostly about market access and visa allocation. Since corporate tax arrived, the answer is about money. Specifically, which structure puts less money into the FTA's account and more into yours.

The surface math seems settled. Mainland: 9% corporate tax on profits above AED 375,000. Free zone: 0% on qualifying income if you are a Qualifying Free Zone Person. Nine percent versus zero. Nobody needs a calculator for that. So thousands of businesses chose free zones for the tax headline, set up in DMCC or IFZA or SHAMS, and assumed the saving was automatic.

It is not automatic. The 0% rate carries a compliance cost that no one explains until the first audit fee invoice arrives. A mandatory annual audit regardless of revenue (AED 15,000 to AED 40,000). Substance requirements that demand real employees and real expenditure in the free zone. Monthly income classification to separate qualifying from non-qualifying revenue. And the permanent overhang of a five-year disqualification if any single condition is breached. As Crossfoot's analysis documented, tax benefits in the UAE are earned through ongoing compliance, not granted through a licence address.

On the mainland side, a business pays 9% on profits above AED 375,000, but the calculation stops there. No income classification. No mandatory audit below AED 50 million revenue. And until December 2026, access to Small Business Relief that can reduce the CT liability to AED 0 for businesses under AED 3 million in revenue, a relief that QFZPs cannot elect.

This article runs the comparison the way it should be run: not as a rate comparison but as a total annual cost comparison. The CT rate, the audit cost, the monitoring overhead, the substance expenditure, the risk of disqualification, and the administrative burden, all calculated in AED, for specific business sizes and profiles. What comes out is a crossover point that nobody else has published: the profit level below which paying 9% on the mainland is genuinely cheaper than maintaining 0% in a free zone.

"I see business owners celebrate getting a free zone licence because they read it means zero tax. Six months later, they realize the mandatory audit costs more than the corporate tax they would have paid on the mainland. The question is never free zone or mainland. The question is: what does each structure actually cost you, every year, with everything included?"

Jazim, CEO, UAE Tax Filing LLC

The Head-to-Head: Ten Dimensions That Decide the Winner

Our QFZP qualification guide covers free zone conditions in full and our deductions guide covers mainland CT calculations. Here is how the two structures compare across the ten dimensions that matter most for corporate tax.

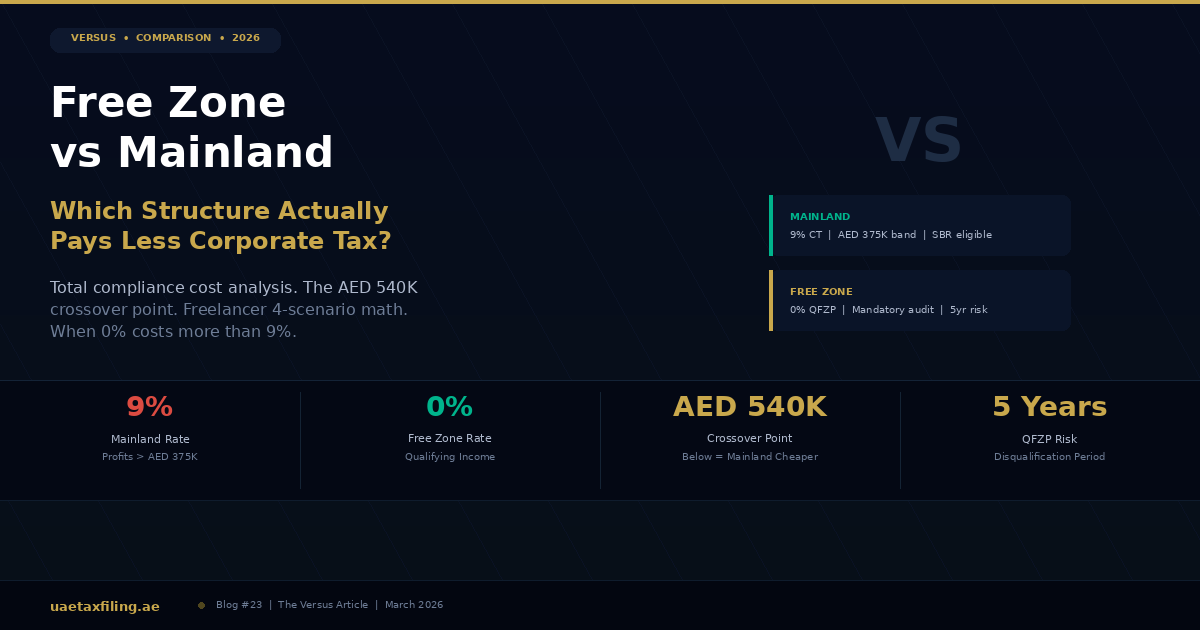

Corporate tax rate. Mainland companies pay 9% on taxable profits exceeding AED 375,000. Free zone QFZPs pay 0% on qualifying income, but 9% on any non-qualifying income with no zero-rate band at all.

The AED 375,000 zero-rate band. This is mainland-only. Every mainland entity gets the first AED 375,000 of taxable income at 0% automatically, no conditions, no application. QFZPs get no equivalent band on non-qualifying income. As Movingo's free zone guide documented, free zone firms do not get the AED 375,000 tax-free bracket for non-qualifying income. A QFZP with AED 100,000 in non-qualifying income pays AED 9,000 in CT on that portion. A mainland company with AED 100,000 in total taxable income pays AED 0 because the full amount falls within the band.

Mandatory audit. Mainland companies need audited financial statements only if revenue exceeds AED 50 million. QFZPs need audited financials every single year regardless of revenue. A SHAMS freelancer with AED 300,000 in revenue pays for the same audit process as a JAFZA trading house with AED 300 million. The cost: AED 15,000 to AED 40,000 per year depending on complexity. As Emifast's analysis highlighted, the cost of a quality audit may actually be higher than the 9% tax you would pay on the mainland for smaller businesses.

Substance requirements. Mainland companies face standard requirements: an office, a visa, trade activity. Free zone QFZPs face strict substance tests: adequate employees performing the core income-generating activities in the free zone, adequate assets, and adequate operating expenditure. The FTA evaluates this on the nature and scale of your business. A trading company with AED 50 million in revenue and one employee in a flexi-desk will not pass.

Market access. Mainland companies can trade freely with anyone in the UAE and internationally. Free zone companies cannot trade directly with mainland consumers without a distributor, a mainland branch, or a dual-licence arrangement. If your customers are individuals or businesses located on the UAE mainland, this restriction makes the free zone operationally impractical.

Income classification. On the mainland, all income is taxed at the same 9% rate. There is nothing to classify. In a free zone, you must separate qualifying income (from other free zone persons, international clients, or qualifying activities) from non-qualifying income (from mainland clients, consumers, certain excluded activities). This classification is monthly, manual, and the source of most QFZP compliance failures.

De minimis risk. Not applicable on the mainland. In a free zone, if non-qualifying income exceeds 5% of total revenue or AED 5 million (whichever is lower), you lose QFZP status for the current year and the next four years. One large mainland client in one quarter can push you past the threshold. Our QFZP guide explains the de minimis rule and its five-year disqualification consequence in detail.

Transfer pricing. Standard arm's length rules apply on the mainland if you have related party transactions. In a free zone, the same transfer pricing rules apply, and TP compliance is specifically required to maintain QFZP status. Failure to maintain arm's length pricing on intercompany transactions can trigger QFZP disqualification independently of the de minimis rule.

Small Business Relief. Available on the mainland for businesses with revenue under AED 3 million per tax period, until December 2026. SBR treats the business as having zero taxable income. Not available to QFZPs. This means a mainland startup pays AED 0 in CT with no audit requirement. A free zone startup with the same revenue pays AED 0 in CT but AED 15,000+ in mandatory audit fees.

VAT treatment. Both structures charge 5% VAT on taxable supplies and file quarterly VAT returns. Designated free zones have limited customs/VAT exceptions for goods within the zone, but for service businesses, the VAT treatment is effectively identical.

Not sure which structure actually costs less for your specific business? Our corporate tax team models both scenarios with your actual revenue, expenses, and client geography. Get your free comparison on WhatsApp.

The Math Nobody Publishes: Total Annual Cost at AED 2 Million Profit

Every competitor article compares the CT rate (9% vs 0%) and stops. That comparison is incomplete to the point of being misleading. Here is the complete annual cost for each structure at AED 2,000,000 in taxable profit.

Mainland company: AED 156,250 to AED 161,250 per year

Corporate tax: AED 146,250 (0% on first AED 375,000, then 9% on AED 1,625,000). Trade licence renewal: AED 10,000 to AED 15,000. Mandatory audit: Not required (revenue below AED 50M). Income classification: Not required. QFZP monitoring: Not applicable. Disqualification risk: None.

Free zone QFZP: AED 35,000 to AED 81,000 per year

Corporate tax: AED 0 (100% qualifying income assumed). Mandatory annual audit: AED 15,000 to AED 40,000. Trade licence renewal: AED 12,000 to AED 25,000. QFZP income monitoring: AED 3,000 to AED 6,000 per year (accountant time). TP documentation: Required to maintain QFZP. Disqualification risk premium: Estimated AED 5,000 to AED 10,000 (insurance-equivalent cost).

At AED 2M profit, the free zone saves AED 75,250 to AED 126,250 per year. That is a real, material saving, and at this profit level the free zone wins clearly. But the saving is not AED 146,250 (the full CT liability). The compliance costs eat 14% to 49% of the gross CT saving. The 0% rate is real. It is also expensive to maintain.

The AED 540,000 Crossover Point

This is the number that changes the entire conversation. At what profit level does the free zone's compliance cost exceed the mainland's CT liability?

The minimum free zone audit costs AED 15,000. On the mainland, the CT on AED 540,000 in taxable profit is: (AED 540,000 minus AED 375,000) x 9% = AED 14,850. At AED 540,000, the mainland CT (AED 14,850) is less than the free zone audit alone (AED 15,000), before adding any other compliance costs.

Below AED 540,000 in taxable profit, the mainland is cheaper. The 9% rate produces a lower total annual cost than the 0% rate. This crossover rises if your audit costs are higher (AED 25,000 or AED 40,000 for complex businesses). No competitor calculates this number. The free zone vs mainland conversation has been stuck on rate comparison for three years. The crossover reframes it as a cost comparison, which is what it always should have been.

The Hidden Costs of 0% That Nobody Mentions

The audit is the most visible cost. Three additional costs accumulate inside every QFZP:

QFZP income monitoring. Every month, someone must classify every transaction as qualifying or non-qualifying. An invoice to a DMCC client: qualifying. An invoice to a Business Bay client: not qualifying. A mixed-scope project serving both: requires allocation. This classification is not automated by any accounting software. It requires manual judgment, documentation of each client's free zone status, and ongoing verification. The accountant time cost is AED 3,000 to AED 6,000 per year for a small company, more for businesses with hundreds of transactions. Miss a classification, and the FTA's audit process will reclassify it at penalty rates.

Substance documentation. The QFZP must demonstrate 'adequate substance' in the free zone: real employees performing the core income-generating activities, real office space (not just a registered address), and real operating expenditure proportionate to the business. A freelancer faces a particular challenge here because the individual IS the business, and proving that work happens inside the free zone office rather than from a home in JBR requires careful documentation: employment contracts specifying the free zone location, tenancy agreements, utility bills, payroll records, and board resolutions confirming that key decisions are made from within the zone.

The five-year disqualification risk premium. If a QFZP fails any qualifying condition in any year, it loses the 0% rate for the current year and the next four years. Five consecutive years at 9%. For a company earning AED 3 million in annual profit, that disqualification costs approximately AED 1,181,250 in additional CT over five years ((AED 3M minus AED 375K) x 9% x 5 years). Even a 2% annual probability of accidental disqualification represents an expected cost of AED 23,625 per year. The de minimis rule is where most disqualifications happen: non-qualifying income exceeding 5% of total revenue or AED 5 million. One large mainland client in one quarter can push a QFZP past the threshold permanently.

When the Free Zone Wins

The free zone structure is unambiguously cheaper when three conditions are all true: profit is well above the AED 540,000 crossover, income is predominantly qualifying by nature (not by restructuring), and substance can be maintained without excessive overhead. Three business profiles illustrate this clearly.

The international consultant (AED 3M+ revenue, all non-UAE clients). A management consulting firm operating from DMCC that serves exclusively European and Asian clients earns 100% qualifying income by default. CT at 0%: AED 0. The AED 30,000 audit cost is a fraction of the AED 236,250 it would pay in mainland CT ((AED 3M minus AED 375K) x 9%). Annual saving: over AED 200,000. The free zone is the obvious choice, and it is not close.

The global trading company (AED 10M revenue, free-zone-to-free-zone and exports). Goods traded outside the UAE or between free zone entities are qualifying income. A JAFZA or DMCC trading house with this profile saves AED 800,000+ per year compared to a mainland structure. The audit cost, substance cost, and monitoring cost combined represent less than 5% of the CT saving. At this scale, the free zone is a tax optimization engine.

Fund management or headquarter services (AED 5M profit). These are qualifying activities under the Ministerial Decisions. High profit margins mean the CT saving dwarfs the compliance cost. Annual saving: AED 400,000+ versus mainland. As PwC's incentives guide confirmed, QFZP status on qualifying activities remains one of the most powerful tax positions in the UAE, provided all conditions are maintained.

The e-commerce sellers on Amazon and Noon are a critical edge case. If a free zone seller ships goods to mainland consumers, that income is non-qualifying. Many sellers discover this only after they have set up inventory in a free zone warehouse. The QFZP classification for marketplace sellers requires line-by-line analysis of shipping destinations and buyer locations.

When the Mainland Wins

The mainland structure is cheaper, and sometimes dramatically cheaper, in three scenarios that collectively apply to the majority of small and medium UAE businesses.

The small consultancy (AED 500,000 profit, UAE clients). This is the scenario that catches the most businesses. A management consultant earning AED 500,000 in profit from UAE clients pays AED 11,250 in CT on the mainland (9% of AED 125,000 above the AED 375,000 band). The same consultant in a free zone pays AED 0 in CT but AED 15,000+ for the mandatory audit, AED 3,000+ for QFZP income monitoring, and faces permanent disqualification risk because all clients are mainland-based (meaning all income is non-qualifying). Total free zone cost: AED 18,000+ with constant compliance anxiety. Total mainland cost: AED 11,250 with zero classification burden. The mainland saves AED 6,750+ per year AND eliminates disqualification risk entirely. The consultant chose the free zone to save on tax and ended up paying more.

Restaurants, retail, and anyone serving local consumers. If your customers are on the UAE mainland, your income from a free zone entity is almost certainly non-qualifying. A free zone restaurant would need a mainland distributor to legally serve food to local customers, adding cost and complexity. As Flying Colour Tax explained, a mainland company earning AED 1 million in profit from local customers pays AED 56,250 in CT with a simple, clean structure. A free zone entity earning the same from the same customers faces the non-qualifying income problem, potentially pays 9% CT anyway because none of the income qualifies, and still pays AED 15,000+ for the mandatory audit on top. The free zone is the worst possible structure for a local consumer business.

Startups with losses or revenue under AED 3 million. Any startup or small business with revenue under AED 3 million should run the mainland-with-SBR calculation before looking at a free zone. Small Business Relief eliminates CT entirely (AED 0) with no audit requirement, no substance proof, and no income classification. The compliance cost is just the basic CT return filing fee. A free zone startup with the same revenue pays AED 0 in CT but AED 15,000+ in mandatory audit fees. Over three years (2024-2026), the mainland startup saves AED 45,000+ in audit costs alone. Our SBR analysis explains why SBR is a bad choice for loss-making businesses that want to carry losses forward, but for profitable small businesses, it is the most tax-efficient position available anywhere in the UAE.

We file CT returns for both mainland and free zone companies and advise on restructuring when the current structure costs more than it should. Our accounting team handles the IFRS financials for QFZP audits and our CT team manages EmaraTax filing for both structures. WhatsApp us for your free structure review.

The Freelancer and Sole Operator Special Case

The free zone vs mainland question is most acute for solo professionals. The UAE has approximately 200,000 active freelancer permits, and the majority were issued through free zones like SHAMS, Meydan, and IFZA for visa convenience, not for tax optimization. Now they face a tax structure designed for multi-employee companies.

Consider a freelance management consultant earning AED 1,200,000 per year with AED 200,000 in business expenses. Taxable profit: AED 1,000,000. Here are the four possible outcomes:

Option 1: Mainland with SBR (revenue under AED 3M). CT = AED 0. No audit required. Total annual tax cost: AED 0 plus basic filing fee. This is the cheapest option by far, available until December 2026.

Option 2: Mainland without SBR. CT = (AED 1M minus AED 375K) x 9% = AED 56,250. No mandatory audit. Total annual cost: approximately AED 58,000 including CT plus accounting fees.

Option 3: Free zone with 100% international clients. CT = AED 0. Mandatory audit AED 18,000 + QFZP monitoring AED 4,000 + substance documentation. Total cost: approximately AED 24,000. Saving versus mainland without SBR: AED 34,000 per year. This works.

Option 4: Free zone with 50% mainland clients. Half the income is non-qualifying. CT on non-qualifying: AED 500,000 x 9% = AED 45,000 (no AED 375K band). Plus audit AED 18,000 + monitoring AED 6,000. Total cost: approximately AED 69,000. This is AED 11,000 MORE than the mainland option. And the freelancer carries five-year disqualification risk on top.

The pattern: for freelancers with 100% international clients, the free zone works. For freelancers with any significant mainland client base, the free zone can cost more than the mainland. And for any freelancer under AED 3 million revenue, SBR on the mainland makes the entire comparison irrelevant until 2027.

Should You Restructure? The Decision Framework

If you already have a structure, changing it has one-time costs: new licence fees, potential asset transfer implications, transfer pricing considerations on intercompany transactions during the transition, and the operational disruption of moving employees, contracts, and bank accounts. Restructuring only makes sense when the annual saving exceeds the one-time switching cost within two to three years.

Mainland LLC with all clients outside the UAE and revenue above AED 3M: Evaluate migration to a free zone. The potential 0% rate on qualifying income can save six figures annually.

Mainland LLC with revenue under AED 3M (any client base): Stay mainland, elect SBR, pay AED 0 in CT until December 2026. Revisit in 2027 when SBR expires.

Mainland LLC with revenue above AED 3M and UAE-based clients: Stay mainland. A free zone adds cost with no CT benefit because the income is non-qualifying.

Free zone QFZP with non-qualifying income approaching 5%: Restructure urgently. Consider splitting into two entities: a free zone entity for qualifying income and a mainland entity for non-qualifying income. This requires transfer pricing compliance between the two.

Free zone QFZP with small profit where audit exceeds potential CT saving: Consider mainland migration. You may be paying more for 0% than you would pay for 9%.

Free zone QFZP with large profit and 100% qualifying income: Stay free zone. This is the structure working as intended. Maximize the 0% rate.

Mixed structure (free zone + mainland entities) with related party transactions: Ensure full TP compliance. Evaluate whether a tax group (95% ownership threshold) could simplify filing, but watch the AED 375,000 band trap we covered in that article.

New business serving UAE consumers directly: Mainland LLC. Free zone restrictions outweigh the tax benefit for B2C businesses.

New business serving international clients only: Free zone. The 0% qualifying income rate, combined with lower setup costs and faster processing, makes it the clear choice. As DubaiSetup's guide noted, dual licensing is also an option for businesses that want free zone tax benefits with selective mainland access.

For property investors, the structure question is different entirely because personal (individual) property holdings are exempt from CT under Cabinet Decision 49. A free zone property company does not get this exemption and faces 9% CT on non-qualifying rental income from mainland tenants. The worst structure for a UAE property investor is often a free zone company, not a mainland one.

What Changes in 2027 and Beyond

SBR expires. Small Business Relief is available only for tax periods ending on or before December 31, 2026. From 2027, mainland companies under AED 3 million revenue will pay 9% CT on profits above AED 375,000. This narrows the mainland advantage for small businesses. A consultant who pays AED 0 today on the mainland may pay AED 56,250 from 2027, changing the free zone comparison entirely. The 2026 tax changes guide covers all the shifts happening this year.

E-invoicing becomes mandatory. The UAE's e-invoicing mandate begins July 2026 (pilot) and becomes mandatory for large businesses from January 2027. Both structures face the same compliance costs. The penalties for non-compliance (AED 5,000/month for failure to implement, AED 100 per non-compliant invoice) apply equally across both jurisdictions.

The QFZP regime itself is not scheduled to change, but the FTA's enforcement intensity is increasing. With 93,000 inspection visits in 2024 and algorithmic cross-referencing of VAT returns and CT returns, audit risk is rising for free zone entities that claim 0% but have borderline qualifying income ratios. The practical cost of QFZP compliance will likely increase as monitoring and documentation requirements tighten through 2027.

Frequently Asked Questions

Is a free zone company exempt from corporate tax in the UAE?

No. Free zone companies are subject to CT. They can qualify for 0% on qualifying income if they meet all QFZP conditions. Non-qualifying income is taxed at 9% with no AED 375,000 zero-rate band.

What is the total annual cost of maintaining the 0% free zone rate?

AED 35,000 to AED 81,000 per year including mandatory audit (AED 15,000 to AED 40,000), QFZP monitoring, substance documentation, and disqualification risk management.

At what profit level is the mainland cheaper than a free zone?

Below approximately AED 540,000 in taxable profit. At that level, the mainland CT equals the minimum free zone audit cost. Below it, paying 9% costs less than maintaining 0%.

Can I use Small Business Relief in a free zone?

No. SBR is not available to QFZPs. Only mainland companies with revenue under AED 3 million can elect SBR for CT = AED 0 until December 2026.

What happens if my free zone income becomes non-qualifying?

If non-qualifying income exceeds 5% of total revenue (or AED 5 million), you lose QFZP status for the current year and the next four years. All income becomes taxable at 9%.

Can I operate both a free zone and mainland entity?

Yes. Many businesses use a dual structure. But transactions between the two must comply with transfer pricing rules and be documented at arm's length.

Should I move my mainland company to a free zone?

Only if your profit significantly exceeds AED 540,000, your income is predominantly qualifying, and the annual CT saving exceeds the total compliance cost plus switching cost within 2 to 3 years.

Do free zone companies still need to file a CT return?

Yes. Every taxable person must file, including QFZPs at 0%. Missing the September 30 deadline risks AED 500/month late filing penalty and potential QFZP status loss.

What is the biggest mistake in the free zone vs mainland decision?

Looking only at the CT rate (0% vs 9%) without calculating total compliance cost. For small businesses, the 0% rate can cost more than the 9% CT it was designed to eliminate.

How do I know if my free zone income is qualifying?

Qualifying income generally comes from other free zone persons or international clients. Mainland customer income is usually non-qualifying. Our QFZP guide covers the full classification.

0% Is Not Free. 9% Is Not Always More Expensive.

The free zone vs mainland debate has been framed as a tax rate comparison for three years. It should have always been framed as a total cost comparison. The 0% rate is genuinely valuable for businesses with high profits, international client bases, and naturally qualifying income. It saves hundreds of thousands of dirhams per year for global traders, international consultants, and fund managers operating from UAE free zones.

But that same 0% rate costs a small consultancy with mainland clients more than the 9% CT it was designed to replace. It costs a startup more in audit fees than it saves in tax. It costs a property investor more than simply holding the property in their own name. The headline rate is not the total cost. The total cost is the rate plus the compliance plus the risk.

The math is specific to every business. It depends on your profit level, your client geography, your income classification, your audit cost quotation, and your honest assessment of whether you can maintain QFZP compliance year after year without a single breach. There is no universal answer. There is only your answer, calculated with your numbers.

Run the total cost comparison before you choose. Run it again every year. The number that matters is not the CT rate. It is the amount that leaves your bank account.

We calculate the total annual cost for both structures using your actual financials. No assumptions. No bias toward either jurisdiction. Just the math that tells you which option is cheaper for your business, this year and next. Get your free structure comparison on WhatsApp.