A JAFZA trading company sells industrial machinery to another JAFZA company. Both businesses are in the same designated zone. The goods never leave the zone. No VAT is charged. The transaction is outside the scope of UAE VAT entirely. The seller does not even report it on the VAT return as a taxable supply.

The same JAFZA company provides consulting services to the same buyer, in the same zone, in the same week. The consulting fee is AED 200,000. VAT at 5% is charged: AED 10,000 in output VAT, reported on the quarterly VAT return, and remitted to the FTA.

Same seller. Same buyer. Same zone. Same week. One transaction has zero VAT. The other has 5%. The difference is not the location, the parties, or the value. The difference is that one transaction involves goods and the other involves services. This is the dual personality of a UAE designated zone: treated as outside the UAE for VAT on qualifying supplies of goods, but firmly inside the UAE for VAT on services. As EAS MEA's designated zone guide documented, a designated zone has two completely different personalities for tax purposes, and understanding this dual nature is fundamental to maintaining compliance.

The confusion costs real money. A business that applies the 'outside the scope' treatment to a service transaction under-reports output VAT. The FTA catches it during the next audit, assesses the unpaid VAT plus 14% annual interest under the new penalty regime, and the correction wipes out months of profit. This article maps every transaction pattern a designated zone business encounters, with the correct VAT treatment for each, the documentation the FTA requires to support it, and the five mistakes that trigger the most audit adjustments.

"The single most common VAT error we see in free zone businesses is applying designated zone treatment to services. Every month, we onboard a client whose JAFZA or DAFZA company has been treating consulting fees, management charges, or logistics services as outside the scope of VAT because they assumed everything in a designated zone is VAT-free. It is not. Only qualifying supplies of goods are outside the scope. Services are always taxable. Always."

Jazim, CEO, UAE Tax Filing LLC

The Dual Personality: Outside the UAE for Goods, Inside for Services

Federal Decree-Law No. 8 of 2017 (the UAE VAT Law) and Cabinet Decision No. 59 establish the framework. A designated zone is a specific fenced geographic area with security controls and customs oversight that meets criteria set by the Cabinet. These zones are treated as being outside the territory of the UAE for VAT purposes, but only for qualifying supplies of goods. As Flying Colour Tax's 2026 guide explains, the logic is simple: as long as goods stay within the fenced, customs-controlled area, VAT is out of scope. The moment goods cross into the mainland, or the moment the transaction involves services instead of goods, standard UAE VAT rules apply.

For goods: A supply of goods within a designated zone, or between two designated zones, is treated as taking place outside the UAE. No VAT is charged, provided strict conditions are met: the goods must remain under customs control, they must not be released for consumption within the zone, and proper customs and movement documentation must exist. This treatment applies only when both parties are established in a designated zone and the goods physically remain within the zone system.

For services: All services supplied within, from, or to a designated zone are treated as taking place inside the UAE. Standard 5% VAT applies. The designated zone status of the supplier is irrelevant for services. As ProAct's 2026 guide confirmed, a JAFZA consulting firm providing project management to a mainland client charges 5% VAT. A DAFZA IT company providing software support to another DAFZA company charges 5% VAT. Warehouse leasing, handling, logistics, legal advice, accounting services, and every other service follows ordinary UAE VAT rules regardless of where the supplier or recipient is located.

For corporate tax: Designated zones are firmly inside the UAE for CT purposes. A JAFZA company pays 9% CT on profits above AED 375,000 (or 0% if it qualifies as a QFZP). The designated zone VAT treatment and the QFZP CT treatment are separate frameworks governed by separate laws. Our free zone vs mainland comparison covers the CT side in full.

Your Free Zone Is Probably Not a Designated Zone

The UAE has over 45 free zones. Only 23 of them are designated zones for VAT purposes under Cabinet Decision No. 59. Every business operating in a non-designated free zone follows standard mainland VAT rules on all transactions, goods and services alike. As ADEPTS' 2026 enforcement guide confirmed, the FTA is actively verifying physical fencing, access controls, and security segregation to confirm continued designated zone status.

The 23 designated zones (verified as of 2026)

Dubai (8): Jebel Ali Free Zone (JAFZA), Dubai Airport Free Zone (DAFZA), Dubai Cars and Automotive Zone (DUCAMZ), Dubai Textile City, Al Quoz (industrial area), Al Qusais (industrial area), Dubai Aviation City, and International Humanitarian City.

Abu Dhabi (5): Free Trade Zone of Khalifa Port, Abu Dhabi Airport Free Zone, Khalifa Industrial Zone (KIZAD/KEZAD), Al Ain International Airport Free Zone, and Al Bateen Airport Free Zone.

Sharjah (2): Hamriyah Free Zone and Sharjah Airport International Free Zone (SAIF Zone).

Ajman (1): Ajman Free Zone.

Umm Al Quwain (2): UAQ Free Trade Zone at Ahmed Bin Rashid Port and UAQ Free Trade Zone on Sheikh Mohammed Bin Zayed Road.

Ras Al Khaimah (3): RAK Free Trade Zone, RAK Airport Free Zone, and RAK Maritime City Free Zone.

Fujairah (2): Fujairah Free Zone and Fujairah Oil Industry Zone (FOIZ).

Popular free zones that are NOT designated: Dubai Multi Commodities Centre (DMCC) with its 650+ crypto companies, Dubai Internet City (DIC), Dubai Media City (DMC), Dubai Design District (d3), Dubai Knowledge Park, Dubai Healthcare City, Dubai Studio City, Dubai Science Park, Dubai International Financial Centre (DIFC), Abu Dhabi Global Market (ADGM), Meydan Free Zone, IFZA, SHAMS (Sharjah Media City), and twofour54. Every transaction in these zones, whether goods or services, follows standard mainland VAT rules at 5%. A DMCC gold trading company that assumes its intra-zone gold transfers are VAT-free is wrong. Standard 5% VAT applies to every supply.

Not sure whether your free zone is designated? Our VAT team verifies your zone status and reviews your VAT treatment for every transaction type. Getting the classification wrong on even one quarter's returns triggers reassessment plus interest. Message us on WhatsApp.

Five Transaction Patterns and Their Correct VAT Treatment

Every transaction involving a designated zone falls into one of five patterns. As TaxReady's comparison guide documented, understanding these patterns is the difference between compliance and reassessment.

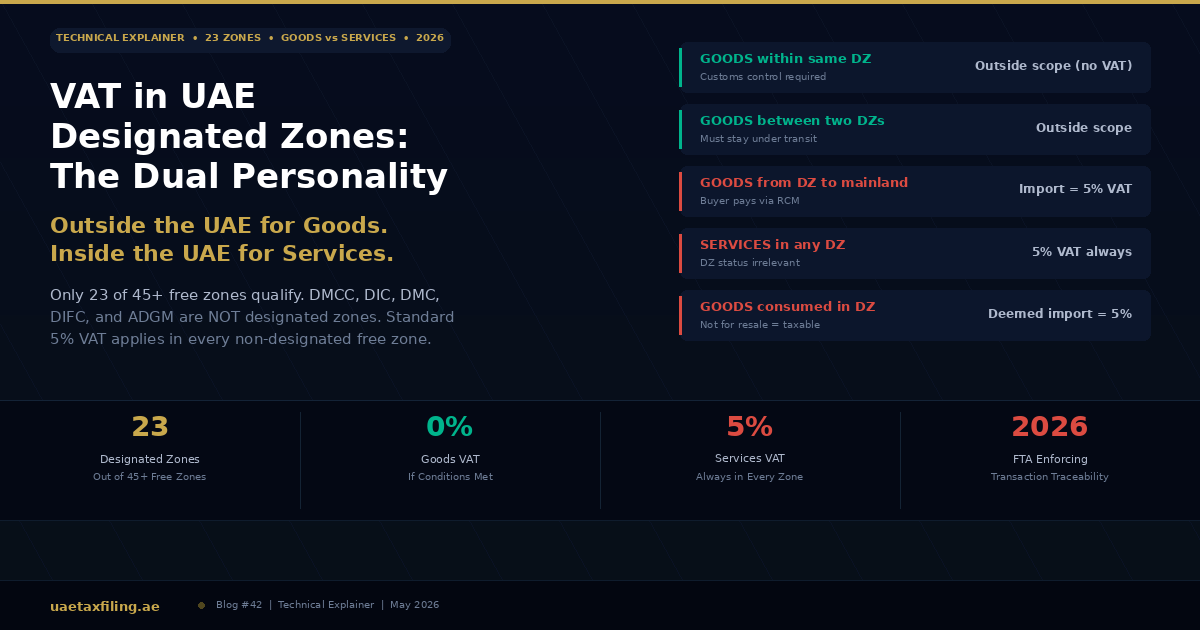

Pattern 1: Goods within the same designated zone

Example: A JAFZA trading company sells industrial machinery to another JAFZA company. The machinery remains in a JAFZA warehouse.

VAT treatment: Outside the scope of UAE VAT. No VAT is charged. The supply is not reported as a taxable supply on the VAT return. Conditions: both parties must be established in the designated zone, the goods must remain within the zone under customs control, and the goods must not be released for consumption (they must be intended for resale, storage, or further production). As ProAct confirmed, the seller should still issue appropriate commercial documentation and retain full customs and transaction evidence.

Pattern 2: Goods between two different designated zones

Example: A DAFZA electronics distributor sells a shipment to a KIZAD warehouse operator. The goods move from Dubai Airport Free Zone to Khalifa Industrial Zone in Abu Dhabi.

VAT treatment: Outside the scope of UAE VAT, provided the goods remain under customs transit control during the entire journey and are never released into mainland UAE at any point. The transport between the two zones must follow customs transit procedures, and both zones must be designated. If the goods pass through a mainland customs point or are temporarily stored in a non-designated location during transit, the out-of-scope treatment is lost and 5% VAT applies. As ADEPTS documented, the FTA requires transaction-level traceability to prove that goods never entered the mainland at any stage of the supply chain.

Pattern 3: Goods from a designated zone to mainland UAE

Example: A JAFZA trading company sells electronics to a retailer in Business Bay. The goods leave JAFZA and are delivered to the retailer's mainland warehouse.

VAT treatment: Treated as an import into the UAE. The mainland buyer is the importer of record and must account for 5% VAT. In most cases, the buyer accounts for the VAT through the reverse charge mechanism: the buyer self-assesses 5% output VAT and claims the corresponding input VAT on the same return (net zero effect if fully recoverable). The designated zone seller treats the transaction as a zero-rated export from the zone. As Flying Colour Tax explained, proper customs export documentation from the designated zone is required to support the zero-rated treatment.

Pattern 4: Services in any designated zone

Example: A JAFZA logistics company provides warehousing and handling services to another JAFZA company. A DAFZA consulting firm provides advisory services to a mainland client.

VAT treatment: Standard 5% VAT applies. Always. The designated zone status of the supplier or recipient is irrelevant for services. Warehousing, handling, consulting, legal, IT support, management, accounting, and every other service follows ordinary UAE VAT rules. The only exception is if the service qualifies as an export of services under the general VAT rules (i.e., supplied to a recipient who is outside the UAE and outside the GCC, and the service is not related to goods or real estate in the UAE). That exception is based on the export rules, not on designated zone status.

Pattern 5: Goods consumed within a designated zone

Example: A company in JAFZA purchases office furniture, food for employees, or cleaning supplies that will be used within the zone rather than resold or re-exported.

VAT treatment: Deemed import. 5% VAT applies. This is the consumption trap. Goods purchased within a designated zone that are intended for consumption rather than resale are deemed to have been imported into the UAE. The buyer must account for 5% VAT on these goods. As EAS MEA's guide confirmed, if goods are released for consumption, moved to the mainland, or no longer remain under customs control, the transaction falls back within the standard UAE VAT framework. Food sold by a grocery store within a designated zone to employees for personal consumption is a taxable supply. Office supplies used by the business within the zone are deemed imports.

Imports From Outside the UAE Into a Designated Zone

When goods are imported from outside the UAE directly into a designated zone, no VAT is charged at the point of entry. The goods remain under customs suspension within the zone. As Flying Colour Tax confirmed, this is functionally similar to a bonded warehouse: duties and VAT are suspended while the goods remain in the zone.

VAT becomes payable only when the goods leave the designated zone and enter mainland UAE (Pattern 3 above) or when they are released for consumption within the zone (Pattern 5). For e-commerce importers who store inventory in JAFZA or KIZAD warehouses before fulfilling orders to mainland customers, each individual shipment from the zone to the mainland triggers the import VAT event. The customs documentation for each movement must be maintained for the FTA Audit File.

Supplies From Mainland UAE to a Designated Zone

A mainland supplier selling goods to a buyer in a designated zone charges standard 5% VAT. As TaxReady's guide confirmed, supplies from mainland UAE into a designated zone are treated as taxable domestic sales, not exports. The mainland seller invoices with 5% VAT, the designated zone buyer pays the VAT, and the buyer claims the input VAT on its quarterly VAT return (recoverable if the purchase relates to taxable or zero-rated supplies).

This catches businesses that assume 'designated zone = no VAT on purchases.' The out-of-scope treatment applies only to supplies within or between designated zones. Purchases from mainland suppliers carry full 5% VAT, just like any other domestic purchase. For businesses that operate in both a designated zone and on the mainland (dual structures), the transfer pricing rules apply to any inter-company transactions between the two entities, and the VAT treatment of each supply must be determined independently based on whether the supply involves goods or services and the direction of the flow.

VAT Registration: Designated Zone Businesses Are Not Exempt

A common misconception is that businesses in designated zones do not need to register for VAT because their goods transactions are outside the scope. This is wrong. As our VAT registration guide explains, VAT registration is based on the value of taxable supplies exceeding AED 375,000 in the previous 12 months, or AED 187,500 for voluntary registration. Even businesses with predominantly out-of-scope goods transactions often have service income, mainland customer revenue, or deemed imports that create taxable supplies above the threshold.

A JAFZA trading company with AED 5 million in out-of-scope goods transactions within JAFZA and AED 400,000 in warehousing services provided to other JAFZA companies must register for VAT because the AED 400,000 in service income alone exceeds the AED 375,000 mandatory threshold. The out-of-scope goods transactions do not count toward the threshold (they are not taxable supplies), but the service income does. Once registered, the company reports both: the out-of-scope goods as non-taxable and the services as standard-rated at 5% on the quarterly return.

For businesses approaching the threshold, the voluntary registration cost-benefit analysis applies: if taxable expenses (on which input VAT is paid) exceed AED 187,500, voluntary registration may allow recovery of input VAT that would otherwise be absorbed as a cost. Our CT registration guide covers the separate CT registration obligation, which applies to all juridical persons regardless of VAT status or zone designation.

Year-End Compliance: The Designated Zone VAT Health Check

Before each year-end filing deadline, designated zone businesses should run a comprehensive VAT health check that covers five areas. First, verify that your zone is still on the Cabinet Decision 59 designated list (the FTA can add or remove zones). Second, review every goods transaction classified as out-of-scope and confirm that customs documentation (gate passes, transfer forms, warehouse records) exists for each one. Third, review every service transaction and confirm it was reported at 5% VAT. Fourth, identify all deemed imports (goods consumed within the zone) and confirm they were self-assessed. Fifth, reconcile your VAT return totals against your CT return revenue figures and document any variance in a written reconciliation.

The FTA's enforcement intensity in designated zones has increased significantly. As ADEPTS documented, audit teams are actively reviewing transaction flows, customs data, and invoicing logic for free zone companies. A voluntary disclosure filed before the FTA initiates an audit carries a penalty of 1% per month of the tax difference. A correction discovered during an audit carries 15% fixed plus 1% per month. The cost difference between self-correction and audit discovery is substantial, and for designated zone businesses with years of potentially misclassified transactions, the exposure compounds quickly. Our penalty challenge guide covers the reconsideration process if you believe an FTA assessment was incorrect.

Designated zone VAT compliance requires transaction-by-transaction classification. Our accounting team configures your accounting software with the correct VAT codes for each transaction pattern and maintains the documentation trail that the FTA requires. Talk to us on WhatsApp.

The Documentation the FTA Requires in 2026

The out-of-scope treatment for goods is not self-certifying. The FTA expects businesses to prove that every out-of-scope transaction meets all the qualifying conditions. As ADEPTS' enforcement guide warned, in 2026 the FTA requires transaction-level traceability to prove that goods never entered the mainland. If a transshipment between two designated zones lacks proper customs documentation or movement records, it can trigger 5% VAT along with a 14% annual interest-based penalty.

For every out-of-scope goods transaction, maintain: customs transfer forms or gate passes showing goods entering and leaving the zone, transport logs confirming the route between zones (for inter-zone transfers), warehouse or inventory records confirming goods remained within the zone throughout the relevant period, proof of the recipient's designated zone status (trade licence, customs client code, or FTA registration confirming they are established in a qualifying zone), VAT invoices or zero-rated invoices prepared in line with FTA requirements, and contracts or purchase orders setting out the supply terms. As ProAct's guide emphasized, the FTA expects these records to match across all systems: your VAT return, your accounting records, and your customs records. Discrepancies between any of these are a common audit trigger.

For deemed imports (consumption within the zone): maintain records showing that VAT was self-assessed on goods consumed within the zone. The FTA audits designated zone businesses specifically for under-reported deemed imports, because the temptation to treat internal consumption as out-of-scope is strong and the error is common.

How Designated Zone VAT Status Interacts With QFZP Corporate Tax Status

The designated zone VAT framework and the QFZP corporate tax framework are separate systems, but they interact in ways that matter for compliance.

You can be in a designated zone for VAT and NOT be a QFZP for CT. A JAFZA trading company that earns most of its revenue from mainland UAE customers gets the designated zone VAT treatment on its goods (those sold within JAFZA are out of scope) but does not qualify as a QFZP because its income from mainland customers is non-qualifying. The company pays 9% CT on its profits. The VAT and CT treatments operate independently.

You can be a QFZP for CT and NOT be in a designated zone for VAT. A DMCC consulting firm that earns 100% of its revenue from international clients qualifies as a QFZP (0% CT on qualifying income from outside the UAE) but gets no designated zone VAT benefit because DMCC is not a designated zone. All services are taxed at 5% VAT regardless. The 0% CT rate and the 5% VAT rate coexist on the same income stream.

The compliance risk: losing QFZP status can affect your VAT position indirectly. If a QFZP loses its status through a de minimis breach (non-qualifying income exceeding 5% of total revenue), the company is reclassified as a standard taxable person at 9% CT. This does not change the VAT treatment of its designated zone goods transactions (those are governed by the VAT law, not the CT law), but it does mean the business is now paying more CT, which compounds the cost of any VAT errors discovered during the same period. Businesses that lose QFZP status often face simultaneous CT and VAT audit exposure because the FTA reviews both registrations when a compliance issue is identified in either one.

Six Mistakes That Trigger Designated Zone VAT Audits

1. Applying out-of-scope treatment to services. This is the number one error. Warehouse leasing, handling fees, consulting, IT support, and management charges within a designated zone are all taxable at 5%. The designated zone status does not exempt services. Every service transaction must be reported with 5% output VAT on the quarterly return.

2. Assuming your free zone is designated when it is not. DMCC, DIC, DMC, DIFC, ADGM, IFZA, SHAMS, Meydan, and many other popular free zones are NOT designated. Standard 5% VAT applies to every transaction, goods and services alike. Check the Cabinet Decision 59 list before claiming out-of-scope treatment.

3. Missing documentation for inter-zone transfers. Goods moving between JAFZA and DAFZA are out of scope only if customs transit documentation proves the goods never touched the mainland. Without gate passes, transport logs, and customs transfer forms, the FTA reclassifies the transaction as a taxable supply and assesses 5% VAT plus interest.

4. Not accounting for deemed imports on consumed goods. Office supplies, food, furniture, and other goods consumed within the zone are not out of scope. They are deemed imports subject to 5% VAT. Businesses that treat internal consumption as out-of-scope under-report VAT and face reassessment.

5. Confusing designated zone VAT rules with QFZP CT rules. The two frameworks are separate. A company can have 0% CT (QFZP) and 5% VAT (on services). A company can have out-of-scope VAT (goods in a designated zone) and 9% CT (non-QFZP). Mixing the two creates errors on both returns.

6. Using outdated zone lists. The FTA has updated the designated zone list over time. Businesses that set up their VAT policies years ago may be applying rules based on an old list. Verify your zone's current status against the latest Cabinet Decision before each financial year. If your zone has been removed from the designated list, every out-of-scope treatment you applied since the removal is wrong and requires a voluntary disclosure.

Frequently Asked Questions

What is a designated zone for VAT purposes?

A specific fenced geographic area listed by Cabinet Decision that is treated as outside the UAE for VAT on qualifying goods supplies. Only 23 of the UAE's 45+ free zones qualify.

Is DMCC a designated zone?

No. DMCC is a free zone but NOT a designated zone. Standard 5% VAT applies to all goods and service transactions in DMCC.

Do services in a designated zone attract VAT?

Yes. Always. All services supplied within, from, or to a designated zone are subject to standard 5% VAT. The out-of-scope treatment applies only to qualifying goods supplies.

What happens when goods move from a designated zone to mainland UAE?

The movement is treated as an import into the UAE. The mainland buyer accounts for 5% VAT, typically through the reverse charge mechanism. The designated zone seller treats it as a zero-rated export.

Are goods consumed within a designated zone VAT-free?

No. Goods consumed within the zone (office supplies, food, furniture for internal use) are deemed imports subject to 5% VAT. Only goods intended for resale, storage, or re-export qualify for out-of-scope treatment.

Can goods move between two designated zones without VAT?

Yes, provided the goods remain under customs transit control during the entire journey and never enter mainland UAE at any point. Customs documentation proving the transit route is mandatory.

Is DIFC a designated zone?

No. DIFC is a financial free zone but not a designated zone for VAT purposes. Standard 5% VAT applies to all transactions in DIFC.

Do I still need to register for VAT if I am in a designated zone?

Yes. VAT registration is based on the value of taxable supplies exceeding AED 375,000, regardless of zone status. Even businesses with predominantly out-of-scope goods transactions may have service income that triggers registration. Our VAT registration guide covers the thresholds.

How does the FTA audit designated zone VAT claims?

The FTA cross-references your VAT return against customs records, gate passes, and transport logs. Discrepancies between your claimed out-of-scope treatment and the customs documentation trigger reassessment plus 14% annual interest.

Does designated zone status affect corporate tax?

No. Designated zone status is a VAT concept only. Corporate tax treatment depends on whether the entity qualifies as a QFZP under the CT Law, which is a separate assessment with different conditions.

Two Personalities. One Business. Zero Room for Error.

A designated zone is outside the UAE for goods and inside the UAE for services. That is the entire rule. Every VAT error in a designated zone traces back to a business that either applied the outside-the-UAE treatment to a service (wrong), assumed its free zone was designated when it was not (wrong), or failed to maintain the customs documentation that proves the goods never left the zone system (wrong).

The 23 designated zones are listed. The five transaction patterns are mapped. The documentation requirements are clear. The penalties for getting it wrong are 5% of the transaction value plus 14% annual interest from the date the VAT should have been paid. For a trading company moving AED 10 million in goods per year, a single misclassified transaction pattern can create a six-figure VAT exposure that compounds every quarter it goes uncorrected.

Check your zone status against the list. Review every transaction type against the five patterns. Confirm that your accounting software applies the correct VAT code to each pattern. Maintain the customs documentation that proves every out-of-scope claim. File the quarterly return with confidence that every figure is defensible. That is the standard. Anything less is an audit waiting to happen.

We configure VAT compliance for designated zone businesses: correct tax codes for each transaction pattern, customs documentation protocols, deemed import tracking, and quarterly return preparation. For businesses that need a full VAT health check before the next filing deadline, we review every historical transaction for correct treatment. Start on WhatsApp.